This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Understanding broad market trends and the specific forces affecting bank and credit union portfolios can guide institutions decisions while helping them prepare for examiner scrutiny of CRE risk , according to a recent Abrigo webinar, Being strategic with your CRE. And in some cases, that's not going to play out, unfortunately.

Now that the cannabis industry is maturing and better understood, is it time for financial institutions to take on the risk of cannabis lending? Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans.

Capital One‘s commercial lending business is facing price pressure from a saturated market of lenders, including non-banks, that are pushing interest rates down. Increasing competition from non-banks continues to drive less favorable terms in the commercial lending marketplace,” CEO Richard Fairbank told investors on Thursday.

Businesses' working capital cycles are longer. Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. Thousands of banks, credit unions, and accounting firms use our risk management and lending solutions, contributing to this cooperative data model for banking intelligence.

FinTech STAX, a capital-raising platform that accepts both dollars and cryptocurrency, helped WCA raise the funds. “We Using cryptocurrency in capital raises opens the Australian market up to overseas investors, STAX CEO Kenny Lee said, according to CoinDesk, a “hard” market for them to get into. “It

China’s peer-to-peer (P2P) lending sector, once 6,000 businesses strong, has been reduced to fewer than three dozen as the government tightened regulations, leaving billions in loans unpaid. While P2P platforms were touted as an innovative way to match savers with small borrowers, the marketplace has had troubles globally.

Large banks, e-commerce moguls like Amazon and eBay and tech firms are likely to enter the alternative lending space, and soon, according to Eden Amirav, co-founder, and CEO of startup LendingExpress. In markets like Australia, this is already happening. Over the […].

Recent data and trends of the small business lendingmarket SMB Lending Insights is a snapshot of current financial trends and metrics that impact small and medium-sized business (SMB) lending and financial institutions. You might also like this guide for smarter, faster small business lending.

Businesses of a certain size — and in industries as varied as construction and restaurants — know the pain of wondering if they will have enough capital to fund operations, inventory, expansion and other mission-critical business activities. When it comes to SMB lending, PayPal has gone global. and global economy. and global economy.

Germain Depository Institutions Act of 1982 enabled thrifts to offer money market accounts and expand lending powers, fostering competition with banks. Unfortunately, many banks were not equipped to manage deposit volatility as they got in a rate war for money market accounts and Super Now accounts. of C&I lending.

Recent dynamics of the small business lendingmarket A deep understanding of the small business lending landscape and potential efficiencies can help banks and credit unions grow their portfolios. You might also like this guide for smarter, faster small business lending.

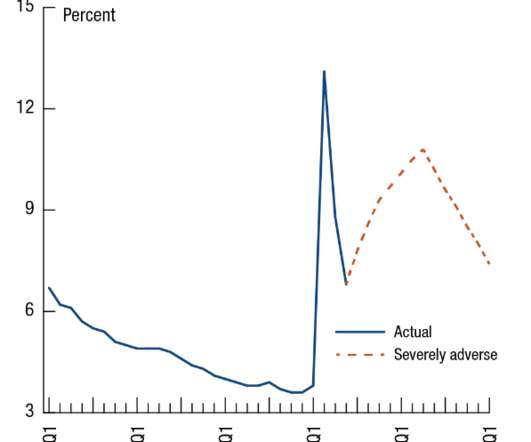

Key Takeaways Stress tests and capital planning are vital to financial institutions in volatile times like these, when the coronavirus and pressures on the energy sector result in a financial crisis. Current environment = Challenging stressed capital planning. This has resulted in theoretical assumptions for capital planning.

Initialized Capital Management has notched $230 million for Initialized V , the California venture firm’s fifth fund, which is geared toward backing early-stage companies, Bloomberg reported. Initialized Capital Management Co-Founder Garry Tan told Bloomberg, “We love finding tomorrow’s unicorns.”.

More than 30 organizations demanded the deal not be subject to expedited federal review and that public hearings be held in the largest lendingmarkets for both Capital One and Discover.

In this article, we highlight the state of the bank commercial real estate office lending sector and make an argument about why banking might be better off than most analysts think. The State of Office Lending Risk – Traffic 2024 will mark the fifth consecutive year where office demand has declined.

Boost your small business lending efforts from the bottom up Small businesses play a crucial role in our economy, and one of the critical factors in their success is access to funding. You might also like this guide for smarter, faster small business lending.

There are quite a few lending solutions these days for small businesses -- Funding Circle, OnDeck, Kabbage, and Square Capital, to name a just a few -- but innovation and digitization are lagging in other areas, such as digital account opening. Enter Gro Solutions, a sales and marketing platform for financial institutions.

Develop an MBL program while mitigating risk Credit unions looking for alternate paths to growth in today's rising rate environment may be primed to leverage member business lending. Takeaway 3 The specific policy areas outlined below should be carefully considered by credit unions engaged in member business lending.

They're also tasked with choosing the best route to obtaining working capital as the number of options grows. From traditional bank loans to alternative financing to other sources of capital like PPP loans , there are many options today, said Puskar. Puskar described the early days of the PPP effort as "hectic." Reading The Tea Leaves.

Recent stats and dynamics of the small business lendingmarket Understanding the small business lending landscape and potential efficiencies can help banks and credit unions grow their portfolios. You might also like this guide for smarter, faster small business lending.

Velo Labs, Visa and Lightnet Group will work together on payment offerings targeted at serving the micro, small and medium enterprise (MSME) lendingmarket in Asia, the announcement stated. We are providing customers from the MSME market with another pathway to build credit and improve financial wellness.”.

Commercial bankers are trusted advisors and have a unique opportunity to understand their client’s specific financial and personal situations, explain the basic concepts of capitalmarkets, and offer prudent and objective advice to help customers reach their goals. It shows the average commercial loan rates for different terms.

On a risk-adjusted return on equity basis, banks moved their target from 16% that held for most of last year, to now looking at a 20% risk-adjusted return on capital (RAROC). Countering this trend is more competitive lending than we have seen in 2024 that manifests in more price concessions and less than expected margin relief.

Leverage customer insights for targeted marketing Understanding the needs of different customer segments allows banks to tailor deposit products and marketing strategies effectively. Banks can attract new deposits by: Providing competitive interest rates on savings, money market accounts, and certificates of deposit (CDs).

A lull in venture capital funding has only a few B2B FinTechs this week securing new investment rounds. Just this week, RTP Global announced a a fund, with the venture capital firm planning to deploy that cash for early-stage technology companies in areas like FinTech and Software-as-a-Service (SaaS).

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. Takeaway 2 The top lending and credit blog posts focused on the benefits of banking technology, interest rate management, and developing risk ratings.

It would make no sense to risk the banks capital without adequate compensation. There are three main considerations that bankers need to analyze to determine if the risk/reward profile of fixed rate loans is adequate in todays market. Therefore, in todays market banks maximize yield and minimize risk by keeping loan duration short.

Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help community banks differentiate their services and enhance their competitive advantage. The largest 100 banks dominate the industry with almost 75% of the market share.

Like many venture capital companies in the payments space, Serent Capital has had a busy year. 15 with the announcement of the launch of its fourth fund, Serent Capital IV — at $750 million. 15 with the announcement of the launch of its fourth fund, Serent Capital IV — at $750 million. That was followed on Dec.

The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks can lend to households and businesses even in a severe recession. The 23 large banks tested remained well above their risk-based minimum capital requirements. Test Results.

Will capital, for instance, become more expensive or cheaper? For example, the problem of improving earnings becomes: Rank the most effective way for the bank to increase profit by 20% within the next 2 years while increasing risk by only 10% and holding capital constant. At this point, attempting to test a solution is most helpful.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Takeaway 1 SBA lending can expand your product offerings to help win deals with prospects and existing business customers or members. Why SBA Lending? Would you like others articles like this in your inbox? 1 and Sept.

Key Takeaways Commercial real estate lending will be a top focus for many financial institutions in 2020. Real Estate Market Outlook. MBA Vice President for CRE Research Jamie Woodwell said in a news release that low interest rates gave CRE markets a boost last year. “In CRE Lending. Lending & Credit Risk.

Small business lending emerged as a common theme in this week’s B2B venture capital roundup, and it’s no surprise, considering the role small and medium-sized businesses (SMBs) play in supporting their local economies. million round for India-based small business lending platform Aye Finance, the company recently revealed.

In 2020, the Federal Reserve found that large banks were generally well-capitalized under a range of hypothetical events. The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks are able to lend to households and businesses even in a severe recession.

Loan providers share an infectious enthusiasm and growing optimism for one vertical’s prospects in 2022: commercial lending. Here’s how community bankers can take advantage of various sectors—including SBA lending—over the next 12 months. anticipates a low double-digit increase in its commercial lending in 2022. Quick Stat.

But we feel that CTLs offer community banks profitable lending opportunities. The credit default market requires only 94.5bps per annum fee for default protection. The graph below demonstrates Starbucks Corporations historical share price, credit default premium, and 1-year probability of default in the market for the last five years.

billion since its 2017 founding, is optimistic about venture capital funding for tech companies, despite current market volatility. Brex, a corporate card and financial product startup that has raised $315 million in equity and reached a reported valuation of $2.6

I recently sat down with the marketing team at Anthemis to talk about the changes happening in SME banking and the opportunity for innovation. But new businesses are often multi-jurisdictional from day one, multi-platform and technically sophisticated in everything from equity capital to treasury to accounting and payroll software.

Euro area banks have scaled back lending in order to shield against risk, a new European Central Bank (ECB) survey says. The banks' continued reticence on lending reflects the uncertainty still present in the economy due to COVID-19, including various government lockdowns and spikes in case counts.

The futures market now expects close to average odds of a 75bps increase in Fed Funds rate for the next FOMC meeting on December 14 th ( HERE ) and about 60% odds of a 75bps hike by January. This week the FOMC increased the Fed Funds rate by 75 bps, as expected to the 3.75% to 4.00% target range. The Yield Curve Inversion. Conclusion.

The company offers businesses working capital so they can borrow funds at a percentage of their income and pay them back in increments, as they make sales through the platform, minus a set fee that is determined by the company’s sales history. Both companies have said they also see the potential in the market.

Last week, the American Banking Association (ABA) held its annual Bank Marketing Conference in Denver, receiving rave reviews. The theme was – developing your marketing superpowers. Amid the brewery networking, superhero costumes, and fun, some fantastic bank marketing lessons were had, and not just for bank marketers.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content