This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now that the cannabis industry is maturing and better understood, is it time for financial institutions to take on the risk of cannabis lending? Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans.

While significantly more efficient than mailing forms to the SBA, there are some shortfalls to E-Tran, and a vendor can help Loan submission platform Leveraging E-Tran for increased SBA lending The U.S. Understanding the role of E-Tran in SBA lending is the first step for banks and credit unions to ensure smooth loan processing.

Businesses' working capital cycles are longer. Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. Thousands of banks, credit unions, and accounting firms use our risk management and lending solutions, contributing to this cooperative data model for banking intelligence.

An update to Square’s credit risk model for its Square Capital commercial lending product — first disclosed yesterday — was “a key driver of Capital’s outperformance in the fourth quarter,” the company said. The advancement of Capital is key for Square as it continues to grow the fast-growing — and lucrative — lending product.

In the wake of the 2008 global financial crisis, and banks' subsequent pullback from the small- to medium-sized business ( SMB ) lending arena, a slew of alternative lenders emerged onto the scene to fill the credit gap. In Canada, one of those alternative players is Thinking Capital.

Businesses of a certain size — and in industries as varied as construction and restaurants — know the pain of wondering if they will have enough capital to fund operations, inventory, expansion and other mission-critical business activities. When it comes to SMB lending, PayPal has gone global. and global economy. Growth Phase.

Recent data and trends of the small business lending market SMB Lending Insights is a snapshot of current financial trends and metrics that impact small and medium-sized business (SMB) lending and financial institutions. You might also like this guide for smarter, faster small business lending.

Automating the key steps that often occur in the back office leads to faster decisions, stronger customer or member relationships, and more profitable lending to small businesses. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

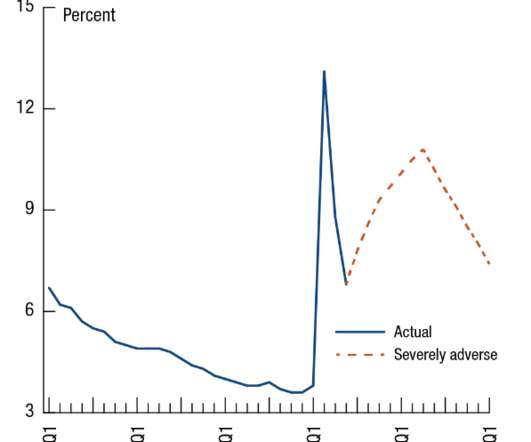

Key Takeaways Stress tests and capital planning are vital to financial institutions in volatile times like these, when the coronavirus and pressures on the energy sector result in a financial crisis. Current environment = Challenging stressed capital planning. This has resulted in theoretical assumptions for capital planning.

Boost your small business lending efforts from the bottom up Small businesses play a crucial role in our economy, and one of the critical factors in their success is access to funding. You might also like this guide for smarter, faster small business lending.

Credit, interest rate, liquidity, optionality, legal and operational risk all interplay with each other to expose the bank, and the borrower, to a set of risk that can be visualized as a three-dimensional area. Some lending markets, such as hospitality, retail and construction have completely dislocated.

PayPal Working Capital will launch in Germany as PayPal Businesskredit, offering small and medium-sized businesses access to working capital financing that is deposited directly into their PayPal accounts. ” German SMBs can apply for the working capital from PayPal online via their existing PayPal accounts. and Australia.

Key Takeaways Financial institutions who want to maintain a healthy share of business lending this year and through potentially tougher economic times ahead want to be in the best position possible before trouble hits. Abrigo's Business Lending Readiness Survey found many processes stymie those efforts. learn more.

In 2015, news outlets ran articles about the “ gold mine ” of venture capital investments in the alternative finance sector. But there is evidence that investors’ appetite for alternative lending startups is on the wane, even as overall FinTech funding continues to climb — and as the success of the alternative lending market grows, too.

Rising production costs led some companies to downsize or relocate operations outside the U.S. Community banks can offer short-term and bridge loans to help clients cover increased costs until supply chains stabilize and working capital loans to support clients in managing operational expenses amid fluctuating costs.

Develop an MBL program while mitigating risk Credit unions looking for alternate paths to growth in today's rising rate environment may be primed to leverage member business lending. Takeaway 3 The specific policy areas outlined below should be carefully considered by credit unions engaged in member business lending.

Federal and state authorities are targeting companies that allegedly lend money to small businesses at extreme rates and seek to collect payments with heavy-handed tactics, NBC News reported Tuesday (Aug. One business owners said he felt as if he were dealing with an entity almost like “a gangster operation.”.

Porter Capital , which works with accounts receivable (AR) financing and asset-based lending solutions, will provide more funding for businesses in need of extra money from their current Paycheck Protection Program (PPP) funds, according to a press release.

Fintech Generations is produced by Queen City Fintech (QCFintech), a premier global fintech accelerator program, and is part of the RevTech Labs operating companies. RevTech Labs alumni have raised over $2 billion in venture capital and have had more than $230 million in company exits. Hans Zandhuis, Head of Ally Lending, Ally.

Velo Labs, Visa and Lightnet Group will work together on payment offerings targeted at serving the micro, small and medium enterprise (MSME) lending market in Asia, the announcement stated. Velo Labs has unveiled a joint effort with Visa and Lightnet Group to build out payment offerings together in Asia, according to an announcement.

Small business lending emerged as a common theme in this week’s B2B venture capital roundup, and it’s no surprise, considering the role small and medium-sized businesses (SMBs) play in supporting their local economies. million round for India-based small business lending platform Aye Finance, the company recently revealed.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. Takeaway 2 The top lending and credit blog posts focused on the benefits of banking technology, interest rate management, and developing risk ratings.

Germain Depository Institutions Act of 1982 enabled thrifts to offer money market accounts and expand lending powers, fostering competition with banks. Banks were now allowed to operate across state lines, increasing competition. of C&I lending. In 1980, all foreign-controlled banks composed about 13% of commercial lending.

These conditions not only impact business operations but also raise critical questions about liquidity, creditworthiness, supply chain stability, and growth strategies. Network: Introducing strategic partnerships or recommending external specialists in international trade, tariff mitigation strategies, or operational optimization.

Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. WATCH Investment accounting compliance risks U.S.

Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help community banks differentiate their services and enhance their competitive advantage. Community bankers need to understand their competitive landscape. The banking industry is nationwide and is becoming less branch-focused.

Despite a surge in sales, small businesses selling online can struggle to manage working capital, particularly as many rely on third-party marketplaces like Amazon that don't facilitate instant access to revenues. Digital commerce is a capital-intensive business model, he said, and keeping pace with buyer demand puts a strain on finances.

Startup valuations are dropping; once abundant venture capital is growing scarcer; marketplace lending has gotten bruised — even the self-proclaimed capital of fintech, London, faces an uncertain future with Brexit. Some of the shine seems to have come off fintech innovation in 2016. Read More.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Takeaway 1 SBA lending can expand your product offerings to help win deals with prospects and existing business customers or members. Why SBA Lending? Would you like others articles like this in your inbox? 1 and Sept.

In 2020, the Federal Reserve found that large banks were generally well-capitalized under a range of hypothetical events. The Fed’s Comprehensive Capital Analysis and Review (“CCAR”) stress tests are designed to ensure that large banks are able to lend to households and businesses even in a severe recession.

But new businesses are often multi-jurisdictional from day one, multi-platform and technically sophisticated in everything from equity capital to treasury to accounting and payroll software. The second expectation is that these platforms will sell data to companies through premium APIs to help generate improved operational efficiency.

We are witnessing the integration of AI, the rise of hyper-personalization, and the adoption of advanced digital platforms, all of which are revolutionizing operations and client interactions. Recommended Approach: To capitalize on the rise of embedded finance , financial institutions should focus on several key strategies.

With the inefficient, circa-2004 borrowing processes resident in many banks’ loan departments today, too few lenders are equipped to deal with the rising tide of home equity volumes that will descend like a tsunami on their operations the moment Fed chairman Jerome (What-Are-We-Waiting-For) Powell announces a rate cut. It’s coming, lenders.

Loan providers share an infectious enthusiasm and growing optimism for one vertical’s prospects in 2022: commercial lending. Here’s how community bankers can take advantage of various sectors—including SBA lending—over the next 12 months. anticipates a low double-digit increase in its commercial lending in 2022. Quick Stat.

In this article, we highlight the state of the bank commercial real estate office lending sector and make an argument about why banking might be better off than most analysts think. The State of Office Lending Risk – Traffic 2024 will mark the fifth consecutive year where office demand has declined.

After industry consolidation and a leveling-out of venture capital interest, alternative SMB lending remains a strong market, though just like traditional banks, it has also faced new lessons as a result of the current market. “It comes in waves, there’s no doubt about it,” he said about the alt-lending boom.

The company offers businesses working capital so they can borrow funds at a percentage of their income and pay them back in increments, as they make sales through the platform, minus a set fee that is determined by the company’s sales history. Both companies have said they also see the potential in the market.

But the latest initiatives reveal a growing interest in transforming internal processes, particularly among smaller banks looking to upgrade their core infrastructure and elevate small business lendingoperations. Bectran Augments Cash Application With API. Jack Henry Links FIs to AR Finance Offering.

Though traditional financial institutions have faced a surge in market pressure to digitize as new FinTech competitors emerge, there are still plenty of areas in which banks hold the upper hand, commercial lending included. But an overwhelming surge in demand painfully exposed traditional banks' biggest shortcomings in business lending.

which operates $12 billion-asset OceanFirst Bank N.A. Although the SBA already operates a microlending program, the underwriting standards are similar regardless of whether it is a $5,000 or $50,000 loan. Banks could pool their resources or leverage the expertise or resources of a bank in a particular location to put capital to work.

It would make no sense to risk the banks capital without adequate compensation. First – The Lending Curve of Community Banks Most banks cost of funding is highly correlated to shorter-term rates, and banks generally prefer shorter loan duration floating, adjustable, or fixed rates of up to one to two years.

Now, many of the nearly 5,500 SBA-approved lenders that are participating in the PPP are weighing the option of leveraging that technology to continue to provide SBA lending after PPP. Leveraging tech for SBA lending after PPP. Or, they might wonder whether it’s too late to start 7(a) lending if they’ve never done it before the PPP.

Now, many of the nearly 5,500 SBA-approved lenders that are participating in the PPP are weighing the option of leveraging that technology to continue to provide SBA lending after PPP. Leveraging tech for SBA lending after PPP. Or, they might wonder whether it’s too late to start 7(a) lending if they’ve never done it before the PPP.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content