This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now that the cannabis industry is maturing and better understood, is it time for financial institutions to take on the risk of cannabis lending? Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans.

Businesses' working capital cycles are longer. Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. Thousands of banks, credit unions, and accounting firms use our risk management and lending solutions, contributing to this cooperative data model for banking intelligence.

Automating the key steps that often occur in the back office leads to faster decisions, stronger customer or member relationships, and more profitable lending to small businesses. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for community banks. Trade policies that lead to retaliatory tariffs from trading partners can lead to more severe economic repercussions in inflation, GDP growth, and employment.

Recent data and trends of the small business lending market SMB Lending Insights is a snapshot of current financial trends and metrics that impact small and medium-sized business (SMB) lending and financial institutions. You might also like this guide for smarter, faster small business lending.

Boost your small business lending efforts from the bottom up Small businesses play a crucial role in our economy, and one of the critical factors in their success is access to funding. You might also like this guide for smarter, faster small business lending.

Confident Risk Management Begins with Sound Loan Policy A risk-based approach to loan policy can effectively improve your institution's profitability. You might also like this webinar on loan policy best practices. Loan policies make up the foundation for managing that credit risk. . When and how to update your policy.

Develop an MBL program while mitigating risk Credit unions looking for alternate paths to growth in today's rising rate environment may be primed to leverage member business lending. Takeaway 3 The specific policy areas outlined below should be carefully considered by credit unions engaged in member business lending.

When and how to cite credit exceptions A policy on credit exceptions can address many factors that can lead financial institutions to diverge from loan policy and miss signs of potential trouble. Takeaway 3 A credit exception policy should spell out what one is, when it can be used, and how to clear it.

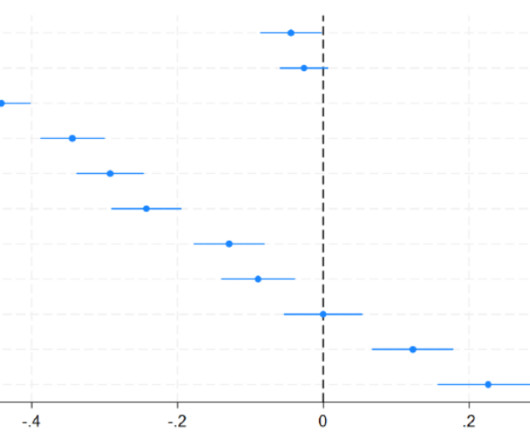

Interventions in corporate credit markets have featured prominently in the policy response to crisis episodes over the last two decades. Framework for policy evaluation We analyse the policy in four steps. We plot the estimated effects of the policy on average loan interest rates in Chart 1.

Large amounts of capital flow across borders. So can recipient countries employ prudential policies to offset monetary policy changes in centre countries? Many people (most notably Hélène Rey’s 2013 Jackson Hole paper ) have advocated taking macroprudential policies to offset this destabilising effect.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. Takeaway 2 The top lending and credit blog posts focused on the benefits of banking technology, interest rate management, and developing risk ratings.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

Over the past decade, several central banks have cut policy rates below zero. In a recent paper we explore the effect on bank lending by combining data on exposure to negative rates with banks’ balance sheets, the Spanish credit register and firms’ balance sheets. Why might negative rates work differently?

Julia Giese, Michael McLeay, David Aikman and Sujit Kapadia Central banks have been using a range of monetary policy and macroprudential tools to maintain monetary and financial stability. Policymakers can do better by also deploying the countercyclical capital buffer , a tool that varies the amount of additional capital banks must set aside.

Commercial bankers are trusted advisors and have a unique opportunity to understand their client’s specific financial and personal situations, explain the basic concepts of capital markets, and offer prudent and objective advice to help customers reach their goals. The graph below shows the lending curve from one month to 20 years.

One proposition is a 9 percent core capital requirement on the top tier, akin to banks. Middle-layer non-bank lenders would follow a board-approved policy on capital adequacy, and upper-layer shadow financiers would follow exposure rules like those big banks follow. It will only let them take on a limited amount of leverage.

Examining supply chain vulnerabilities exposed by current trade policies, including dependence on imported raw materials or overseas manufacturing. Such value-added services underscore the bank’s commitment to their clients well-being and solidify their role as trusted advisors rather than mere providers of capital.

Understanding gross capital flows is crucial for both macroeconomic and financial stability policy. However, theory is lagging behind empirical work , as much of the literature continues to rely on net capital flow models developed many decades ago. This has major implications for several policy debates.

‘Zombie lending’ occurs when a lender supports an otherwise insolvent borrower through forbearance measures such as repayment holidays and temporary interest-only loans. In a recent paper , I examine whether these lending practices contributed to the subsequent low output experienced by the euro area. Belinda Tracey.

Though traditional financial institutions have faced a surge in market pressure to digitize as new FinTech competitors emerge, there are still plenty of areas in which banks hold the upper hand, commercial lending included. But an overwhelming surge in demand painfully exposed traditional banks' biggest shortcomings in business lending.

Government Accountability Office (GAO) said that financial regulators should look more closely at the role of non-bank tech companies in the small business (SMB) lending and consumer lending markets. Such alternative data, said the GAO, could pose risk to such lending decisions.

Top down and bottom up analysis can inform capital assessments. Effective stress testing can benefit many different facets of lending, from risk management and strategic decision-making to capital adequacy and liquidity management. Stress testing and capital adequacy. Stress testing and risk management.

There is ample evidence that a monetary policy tightening triggers a decline in consumer price inflation and a simultaneous contraction in investment and consumption (eg Erceg and Levin (2006) and Monacelli (2009) ). Chart 1 shows the impulse responses to an unexpected rise in the policy rate.

” There is a real opportunity here for community banks to position themselves within this movement and capitalize on what the consumer sees as their strengths— relationship-based lending , tailored product offerings, and knowledge of the local community. Develop a relationship-based lending framework.

Michael Kumhof and Mauricio Salgado-Moreno While ‘unconventional’ balance-sheet policies like quantitative easing (QE) and quantitative tightening (QT) appear to have been successful, it is difficult to separate their macroeconomic and financial stability implications from those of other polices.

Support credit risk management Understanding loan covenants, when financial institutions should use them, and how to monitor them supports strong lending portfolios and credit risk management best practices. Takeaway 2 Capital, performance, and administrative covenants are common with business loans.

has small businesses “scrambling to access financial resources to meet their working capital and long-term expansion needs,” Coface said in its report. National economic policy has China cracking down on its shadow banking market, which has also exacerbated small businesses’ struggle to access financing, analysts said.

Sangyup Choi, Tim Willems and Seung Yong Yoo How does monetary policy really affect the real economy? What kinds of firms or industries are more sensitive to changes in the stance of monetary policy, and through which exact channels? ’), which is why we are interested in creating a broad database of such shocks.

Commercial real estate lending continues to receive regulatory scrutiny and reminders for financial institutions to practice solid risk management. They also call for more robust loan review and ALLL policies and practices and “possibly, higher capital levels.” Image credit: Benjamin Child via Unsplash.

Leveraging the efficiencies gained from lending software Banks and credit unions that leverage an integrated lending and credit platform reap the benefits of a consistent, efficient and defensible lending program. Lending and Credit Software. Ag Lending. Lending & Credit Risk. Lending & Credit Risk.

In Kenya, the Capital Markets Authority (CMA) has issued its “FinTech Sandbox Guidance Note,” which is now finalized as policy. Under the terms of that license, said CNBC , the company will be able to offer full current accounts and business lending. Poland, Germany and France. license in the face of Brexit.

The 2008 global financial crisis showed the need for effective macroprudential policy. But what tools should macroprudential policy makers use and how effective are they? We found that capital requirements reduce the effects of financial shocks. Model 2 added capital requirements. What we do.

The Financial Stability Board says Basel III rules have not led to a squeeze of the small business bank lending market, according to reports on Friday (June 7). The FSB announced Friday the findings of its analysis of Basel III regulations on the small business lending space.

Dennis Reinhardt and Carlos van Hombeeck Have post-crisis reforms of banking regulation made banks and lending more resilient to the shock from Covid-19 and if so by how much?

The issues, sources said at the time, could be attributed to problems in how CAN Capital reported delinquencies among its SME borrowers, leading the platform to breach agreements with major lenders, like Wells Fargo. It all stems back to 2010 or so, when CAN Capital launched ambitious growth plans to enter into new markets.

This post investigates whether large and small banks in the UK and US differ in the cyclical patterns of capital positions and credit provision. The reforms aimed to ensure that banks have sufficient capital resources to absorb losses and reduce the cyclical effects of bank capital (and regulation) on the supply of bank credit in stress.

Takeaway 3 Timely risk ratings and a written review policy are critical components of effective loan review and credit review. Larger or more complex institutions might have credit risk review functions entirely separate from their lending functions. Reviewing lending staff’s risk ratings. Identifying Credit Weaknesses.

We’re also a pure-play technology company, designed to support banks [that] want to offer lending products, but … either can’t or won’t dedicate hundreds of millions to building the capacity,” he said. The loans are guided by their credit policy, carried on their balance sheets. This is the bank’s product backed up by our brand.

Due to the troubles, the banking sector in the country seems poised to see shrinking lending margins, and a potential for a large amount of bad debt. People’s Bank Of China said it reached out to each bank and let them know about the rating, asking some to make changes to capital or to get rid of bad loans.

The vast majority of small businesses will enjoy the benefits of the full 20 percent deduction,” said NFIB Senior Vice President of Public Policy and Advocacy Brad Close in an interview with The New York Times in January. Overall, the top banks saw lending grow by 2.3 percent in 2018, compared to a 3.6 percent growth rate in 2017.

London has been leading the charge to be the FinTech capital of the world, but many other cities are nipping at their toes. Many FinTechs are providing financial services directly to customers in areas such as payments and P2P (peer-to-peer) lending. It shows how important FinTech is when major financial centres vie for focus.

Takeaway 3 Credit analysts need training to understand the working capital cycle, look for hidden risks, and be aware of accounting changes. It's about ensuring that every aspect of your lending operation is optimized for efficiency and effectiveness. Assess and control key risk areas with an effective credit policy.

The European Union is in the midst of several upgrades and overhauls within its financial sector, including ongoing efforts to improve access to working capital for the region’s small and medium-sized businesses. The latest figures show levels of bank lending to large corporates has recovered back to pre-crisis levels.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content