This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Payment fraud: What is it and why the payment system used matters Payments are evolving, and so are fraud tactics. Financial institutions must stay ahead by implementing proactive fraud detection strategies to protect their customers and mitigate losses. Key topics covered in this post: What is payment fraud?

Can your AML/CFT and fraud staff recognize these fraud typologies? The technology used to perpetrate financial crimes may be changing, but these common fraud typologies aren't going anywhere. This is a nearly 10% increase in complaints received and a 22% increase in losses and thats just fraud that was offically reported.

DOWNLOAD WHITEPAPER Growing popularity What is driving the rise in crypto fraud? Takeaway 1 Crypto fraud is the newest and most favored field in potential financial gains for bad actors. As it becomes more integrated into our financial system and scams increase, crypto fraud prevention must be a priority. billion in 2020.

While unfortunate, the rising tide of fraud is not necessarily surprising. As technology has evolved, so have their tactics. The dial-up world of the 1990s was a golden age for credit card telephone fraud schemes. Financial criminals have been targeting digital transactions for over three decades.

Merchants saw a drop in card-present fraud due to the increased adoption of Europay, Mastercard and Visa (EMV) chip cards, Visa said. Merchants who have upgraded to chip technology saw a decrease of 80 percent in counterfeit fraud dollars in September of 2018 when compared to September of 2015. More than 3.1

Consumers have more heavily leaned on debit during the pandemic, with the economic downturn making shoppers more cautious than ever about the prospect of taking on credit card debt. A recent study even estimates that shoppers could ultimately shift $100 billion worth of annual spending from credit cards to debit cards.

Payment system types, trends, and fraud risks Understanding how payment systems function, the different types in use, and the associated risks is critical for financial institutions to be able to balance innovation with security. Need short-term fraud or AML staffing relief? Payment card networks in the U.S. trillion in 2021.

And even before then, as evidenced by an earlier conversation between Karen Webster and Drew Edwards , CEO of Ingo Money , mobile deposit fraud was increasingly becoming a favorite vector for criminals. Back then, Edwards noted that mobile check fraud was escalating so much that some banks were shutting off the feature entirely.

But the bad news is that fraudsters see a once-in-a-lifetime opportunity to jump into the increased flow of transactions, Gary Sevounts , executive at fraud detection firm Kount , told PYMNTS in a recent conversation. He added that fraudsters have been showing up across the board in terms of fraud types attempted.

Bank wire fraud is growing and becoming more complex. Takeaway 1 Bank w ire transfer fraud is increasing due to technological advances today. Takeaway 2 Transnational criminal organizations commit b ank wire transfer fraud and use a variety of techniques to make Americans their victims. billion in losses reported.

The rising trend of digitization in commerce and the increased occurrence of card-not-present fraud were not created by the COVID-19 pandemic. Those dynamics have made the dangers of fraud far less abstract to consumers. Fraud, he said, is occurring at an unprecedented rate and scale and it was far from a small issue before.

Visa announced that since their inception, chip cards have reduced counterfeit fraud by 87 percent. . Chip cards are increasingly becoming the norm as usage and acceptance has continued to grow since the EMV standard was first introduced in 2011,” the company said. Counterfeit fraud dollars for all U.S.

In an interview with PYMNTS, Mitch Pangretic, senior vice president of strategic partnerships at Elan , said that in-person cardfraud may have decreased thanks to EMV chips and multi-factor authentication, but card-not-present (CNP) scams are increasingly gaining traction. Interacting With The Cardmember.

Mobile ordering apps are largely responsible for keeping the industry above water, but fraud still plagues the sector. And while promising news regarding COVID-19 vaccines may have put the end of the pandemic in sight, the restaurant industry’s growing fraud concerns will not cease as abruptly. About The Tracker®.

The financial industry is particularly vulnerable to digital fraud. Application fraud, which sees cybercriminals submitting financial product applications to banks with no intention of paying them back, is among the most popular techniques. Defining Application Fraud.

Debit card issuers face an ever-growing array of fraud schemes perpetrated against them and their account holders. Effective card offerings require financial institutions (FIs) to quickly and accurately detect myriad forms of fraud, forcing them into a delicate balancing act. The Face of Fraud.

A cyberattack from Maze ransomware against global business and tech firm Cognizant mostly hit the company’s corporate cards that had been issued to employees, the company told authorities, according to The Times of India. Also, the FBI has been called to assist with finding out the perpetrator.

As for the areas where scammers managed the biggest hits, business email compromise (BEC), confidence/romance fraud and spoofing were the top three types of crime in terms of monetary losses. BEC fraud does not respect seniority, and it pays exceedingly well.”. billion (or slightly over half) of all losses tracked in 2019.

PAAY has rolled out a partner platform to let merchants and payment providers implement and track EMV 3DS, a standard that aims to help prevent unauthorized card-not-present (CNP) transactions, throughout different merchant accounts. It is essential right now that businesses take measures to protect themselves against fraud.

The financial services sector is experiencing transformative changes driven by technological advancements and innovative trends. AI-powered chatbots can handle routine inquiries, freeing human agents for complex issues, while AI-driven algorithms enhance fraud detection and risk management.

And consumers want to pay with their preferred methods, across cards or digital wallets. Artificial intelligence (AI) can improve the eCommerce experience – not just in terms of warding off fraud, but also in making sure payments can be processed efficiently and that the most effective payment gateways are accessed.

Long before the pandemic, consumers were trending toward digital in their financial services relationships — experimenting with mobile wallets, digital cards, self-service mobile banking and digital gifting. Firms must position themselves to take that valuable top-of-wallet card location with consumers.

6 Steps t o mitigate fraud risk tied to new products Your AML and fraud teams' input is key when it comes to offering new bank products. You might also like this infographic, "Beyond immediate fraud losses: How the costs and impacts of fraud snowball." download NOW Takeaway 1 Fraud losses totaled $485.6

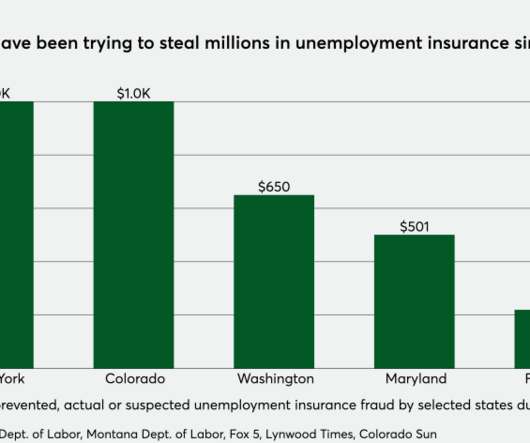

Since July, Visa has noticed an uptick in unemployment insurance fraud with prepaid cards being used as a key disbursement vehicle. And the best solution may be rooted in technology, not law enforcement.

The growth in digital transactions is also spurring a boost in friendly fraud, which occurs when legitimate customers either knowingly or unwittingly claim that they did not make legitimate purchases and seek reimbursement for them. It also analyzes how focusing on the customer experience can help prevent such fraud in the first place.

A recent study from PwC found that 47 percent of companies had experienced fraud at least once in the past two years, with a grand total of $42 billion in funds stolen over this period of time. There were 223,163 cases of identity theft that year across all generations, with 42 percent of them consisting of bank and credit cardfraud.

How financial institutions can prevent losses from 1st-party fraud Learn strong approaches to identifying, preventing, and detecting 1st-party fraud that will keep your AML program on top of fraud trends. Takeaway 3 Prevention and detection best practices can curb hard dollar 1st-party fraud losses while protecting clients.

18) that cardholder signatures will now be optional for the back of credit cards and receipts. In a press release , Mastercard said it is making the changes due to advancements in technology and security. The survey also found that more than half of respondents believe they are secure without signing the cards.

Prevent fraud when adopting FedNow Credit unions can prevent fraud as they connect to FedNow. Use this guide to understand available tools and the steps AML and fraud teams should take. You might also like this FedNow implementation guide with details on appropriate AML/CFT and fraud considerations.

As consumers shop amid ongoing public health restrictions, they almost invariably reach for their credit cards — whether the physical varieties in their wallets or the digital versions stored on their browsers and mobile devices. More than ever, credit cards are becoming the coin of the realm in the global connected economy.

Those less tech-savvy individuals represent juicy targets for fraudsters, who have been fine-tuning card-not-present (CNP) schemes to work across all manner of channels during the pandemic as we wield smartphones to make transactions or bank over the phone. CNP fraud, Nolte said, has become a numbers game.

Mastercard has announced a series of consumer protections aimed at protecting customers and merchants from fraud at fuel stations. The enhanced consumer protection program was designed to provide merchants and banks with tools to help them navigate the heightened risk of fraud, Mastercard said.

He and Nitendra Rajput , Mastercard’s vice president of product development and head of the company’s “AI Garage,” said that in many cases, AI is the only way to scale up sufficiently to meet the challenges the company faces with fraud and other business issues. “It Fighting Fraud in a Post-Pandemic World.

Spend management was the focus of innovation in the commercial card space this week thanks to partnerships and investments in firms aiming to help companies keep track of expenses. Monitoring fuel purchases through both cost and location is a valuable tool for fleet managers to prevent fraud and protect margins.”.

The economic risks of AI to the financial systems include everything from the potential for consumer and institutional fraud to algorithmic discrimination and AI-enabled cybersecurity risks. Hsu discussed the systemic risk implications of AI in banking and finance using a “tool or weapon” approach.

Financial institutions (FIs) are therefore expected to offer more contactless cards this year and some are also unveiling services intended to help consumers easily add cards to their digital wallets. consumers to shift as much as $100 billion in annual spending from credit to debit cards. Around the Next-Gen Debit World.

The phenomenon of payments fraud is not a modern one — far from it. But as RL Prasad, SVP of payment system risk at Visa , told Karen Webster in a recent conversation, what is new today is the who and the how of fraud, particularly in a digital world.

Accrualify , which works in cloud-based solutions for mid- and enterprise-level companies, is launching a new corporate card in partnership with Visa , according to a press release. The intent of the card is to boost options for spend control for corporate finance teams.

The most popular financial crime blogs in 2023 Check fraud, the SAFER Banking Act, and BSA exam topics were among Abrigo's top blogs on AML/CFT and fraud this year. You might also like this infographic on the true costs of fraud at financial institutions. Here are Abrigo’s 10 top AML and fraud blogs in 2023.

These growing revenue streams carry their own risks, however, not the least of which is their propensity to be targeted by fraud. The Fraud Threats Of 2020. Most customers bypass restaurants entirely when trying to perpetrate chargeback fraud , with 76 percent of cardholders going directly to their payment card issuers.

While there is no shortage of new things in the world to get used to these days, cybercrime and fraud are, unfortunately, not among them. The good news, both Srinivasan and Awad told PYMNTS, is that while fraud attempts are up among U.S. consumers, fraud losses are not, yet. million pounds out of the unwitting. “We

The number of real-time payments has risen dramatically in recent years, and APP fraud has grown alongside it. Bad actors typically perpetrate APP fraud in several ways. APP Fraud Ramps Up. Instances of APP fraud around the globe have continued to rise as real-time payment rails extend their reach.

It’s the battle against fraud that can be lost right at the beginning. Bad actors, are, increasingly, targeting online card applications, using stolen personally identifiable information to apply for credit, leveraging those ill-gotten credit lines to make fraudulent purchases. alone topped $10.2 billion last year. alone topped $10.2

It’s happened to almost all consumers: They’re idly perusing their credit card statements when they come across completely confusing, seemingly random charges from businesses they don’t recognize in locations they’ve never visited. Depending on the industry, friendly fraud can account for anywhere from 25-80 percent of all fraud losses.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content