This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To that end, the the Internet Crime Complaint Center (IC3), a hub to bring complaints to the Federal Bureau of Investigation (FBI), is eyeing payroll fraud. Often steered toward a prepaid card owned by the cybercriminal, said IC3. In Europe, especially, nations must be on the lookout for payment cardfraud. The deposits?

There certainly is room for improvement, according to the whitepaper, as middle market companies, which are defined as those with annual sales below $500 million, spend an estimated $7.8 billion of that amount could be made through corporate cards. trillion on B2B interactions each year, and MasterCard has estimated that $1.8

Between account takeovers, business logic abuse, loyalty and reward points fraud and other cybersecurity attack methods, companies are not only suffering financial damages but brand image damages too. Here are a few of the top things every eTailer should know about fraud in 2017. Card Not Present Fraud Is A Big Threat.

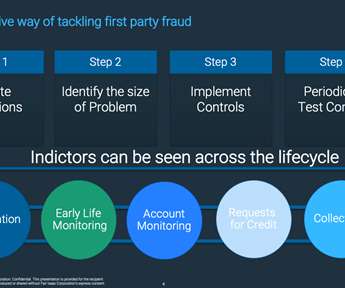

Traditionally, credit application fraud has been perpetrated in two ways: First-party fraud – where the criminal uses their own identity to commit fraud, even if they obscure some details in order to prevent detection. Where fraud data sharing is in place, their scope may well be limited across multiple organizations.

FICO has just released an interactive infographic on European cardfraud trends since 2006, showing that cardfraud in the 19 countries studied has hit a new high of €1.8 In the UK, cardfraud also a hit a new high in 2016, £618 million, though the rise was less than the rise from 2014 to 2015.

In its latest whitepaper, titled “Omni-Channel Payments for Merchants: Myth or Reality?,” To gain a better understanding of how pervasive omnichannel payment offerings are among merchants, ACI Worldwide collaborated with Payments Cards and Mobile (PCM Research) to conduct a survey of the retail industry.

The card processing landscape experienced significant changes in 2017, and this shift in players will impact financial institutions well into the future. What follows is a list of the vendors Cornerstone sees in 85% of our card selection projects. PSCU and Jack Henry Card Processing Solutions (JHA CPS).

Smart Card Technology Can Increase Security, Decrease Payment Vulnerability, Reduce Fraud and Improve Workflow for the Healthcare Industry PRINCETON JUNCTION, N.J. Press Release] – At the same time as the.

But the global adoption of such schemes, alongside the problems suffered by early adopters, has turned the focus to real-time payments fraud. As discussed in my earlier post , real-time payments make multiple types of fraud more attractive and enable the fast movement and laundering of criminal proceeds. Who Is Liable?

This is the fourth in my series on five keys to using AI and machine learning in fraud detection. In fraud detection, a model will benefit from the experience gained by ingesting millions or billions of examples, consisting of both legitimate and fraudulent transactions. It’s the computing equivalent of human experience.

In my previous post I looked at what was driving synthetic identity fraud and discussed the difficulties in classifying both first-party fraud and synthetic identity fraud. An inherent challenge with first-party fraud is sorting out fictional customers from real ones without reducing business. What to Do.

What Is First-Party Fraud? From banks to telcos to debt collection agencies, what looks like unrecoverable bad debt may in fact be first-party fraud. For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. by Matt Cox.

In a world where convergence is coming faster than any whitepaper can articulate, O’Connell said it’s more important than ever for payments players to ensure their payments networks are responsible, safe, secure and fair. When you have that consortium data, fraud becomes much easier to manage and stay ahead of,” O’Connell noted.

Payment fraud is an ideal use case for machine learning and artificial intelligence (AI), and has a long track record of successful use. Recently, however, there has been so much hype around the use of AI and machine learning in fraud detection that it has been difficult for many to distinguish myth from reality.

For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. Perhaps surprisingly, consumers sometimes use their own personal information to commit fraud. Both of these crimes are first-party fraud.

Biometric Security Crucial for Fraud Protection and CX. Because customers value ease of use and good fraud protection most, FIs must balance scam protection with making things easy for good customers – but not TOO easy. How FICO Can Help You Fight Application Fraud. Download the whitepaper on this survey.

This is the second in my series on five keys to using AI and machine learning in fraud detection. Non-monetary may include a change of address, a request for a duplicate card or a recent password reset. A good example of this occurs in our FICO Falcon Fraud Manager, with its Cognitive Fraud Analytics.

As the US payment card infrastructure continues to move to EMV, fraudsters are turning their targets toward unattended self-service terminals, such as US ATMs, most of which have not yet been upgraded to read EMV chips. Globally, the European ATM Security Team reported a 19% increase in ATM-related fraud attacks from 2014 to 2015.

Payment fraud is an ideal use case for machine learning and artificial intelligence (AI), and has a long track record of successful use. Recently, however, there has been so much hype around the use of AI and machine learning in fraud detection that it has been difficult for many to distinguish myth from reality.

The Secure Technology Alliance has released a whitepaper, which shows that cards with dynamic security code features might prevent card-not-present (CNP) fraud.

This is a guest blog from Jonathan Williams , an expert in payments, identity and fraud prevention, working for advisory firm Mk2 Consulting. In July, the European Banking Authority (EBA) published their guidelines for reporting fraud under Payment Services Directive 2 (PSD2).

Examples given of operational areas that could be impacted by employees working remotely and create compliance and reputational risks included call centers and customer service, collections, dispute investigation, loss mitigation, fraud investigation/ID monitoring, and compliance monitoring.

FICO global survey finds customers want better fraud protection and more security from their digital banking channels. FICO’s 2022 consumer banking fraud survey shows that customers are split in their thinking on when they sufficiently trust a digital channel to apply for a new account, loan, or credit card. . FICO Admin.

So it’s not surprising to find machine learning being advocated as the answer for payment service providers looking to manage fraud in the world of PSD2. Why does PSD2 make machine learning more important than ever in the fight against fraud? Actually, the use of machine learning to fight fraud has a long and successful pedigree.

In some cases, these will be technically defined, in some cases related to social engineering and in others these contexts will be patterns of activity that indicate a higher fraud risk, for example, changing an address and requesting a new credit card. is low and so are the authentication requirements.

The key success factor will be to be able to capture the application data in a digitally innovative way and to decision the applications almost instantly with low friction but with an adequate KYC, AML and application fraud control. For more information, see our whitepaper on “Can Alternative Data Expand Credit Access?”.

FICO leverages machine learning (ML) in solutions ranging from fraud detection to marketing. To learn more about FICO’s research in the use of artificial intelligence and machine learning for credit scoring models in the financial services industry, please refer to the following whitepaper: [link]. . by Can Arkali.

Banks are well positioned as is explained in a recent whitepaper of the European Banking Association (EBA). Some suggest that digital identity verification by banks could ultimately end the need to type in a credit-card number on an ecommerce website. From Banks want to keep your digital ID in their vaults – FT.com ].

This is typically carried out by checking data, for example, the electoral roll or looking at trusted documents, such as government-issued passports, identity cards, or driving licences, and checking that they are genuine, valid and have not been tampered with or altered. The customer’s device presents with a different SIM card.

The FICO Blog posts last year reflected that – we wrote about everything from the impact on collections, proactive lender communications with consumers, issues with fraud, and of course, how FICO® Scores were impacted. consumers had on average $6,004 in credit card debt, down from an average of $6,934 back in January 2020.

These include falling consumer retention figures, as app transaction abandonment rates increase; the cost of developing and maintaining mobile apps; ensuring adequate security for accurate billing and fraud prevention; and meeting regulations such as PSD2.

One use case is to use a bot, via text messaging, to help customers when they have potential credit cardfraud. Card-linked offers generated a lot of excitement a few years ago. They have a platform to source the merchant offers, and match them with card issuers. Link your card to website or app, select the offer.

With CRMnext, replacing a lost card or request a new pin is a one button process. Demo: voice conversation with Alexa, able to ask bank account balance, block cards, pay bills, send money to friends. They are introducing CrossCore – First smart plug in play fraud and identity platform. 20% of customer interactions are assisted.

Credit cards offer rewards but over 60% of payments are made on debit cards. Chip card reader for when customers are shopping online to improve security. Verifies the card and pushes that information onto the merchant. The software/platform pieces is the ability to use virtual card numbers. Plus the 1% rewards.

asked Aashish Sharma , referring to a game-changing card in poker “Is this the event that will turn the way we interact, learn, play, communicate, run our businesses, and our lives in general?”. Odds assessment of the last card to be played. Finding Business Opportunities From Covid-19. “Is Is COVID-19 ’the Turn’?”

Download our latest whitepaper that discusses what it really takes to develop a successful Fintech startup. Going to speak about technology can be better used in the card world. Card-linking – link to Facebook, BofA, other so you can get a targeted real-time discount offer. 12:23 pm Silver6 – [link].

I like the idea but I am a bit concerned about the potential for fraud from both companies and investors. You can look at life events such as marriage, credit card, new job, etc. Addresses compliance, fraud experience and customer experience analytics. users fall victim to fraud.” I need to learn more. Very fast and cool.

That ignition is thanks to the fact that all Transport of London trains accept contactless cards now – where the report says that 9 in 10 rides are paid for via a contactless card. Merchants and Chip Cards. IBM ), allegations of consumer harm over not being able to require the use of PINs with Chip Cards ( Walmart v.

Today, the hype machine, which is the fuel of the investments in blockchain and crypto, rooted in a world run by algo-driven, permissionless networks, appears to be little more than a bunch of academic whitepapers and blog posts that sound great in the echo chambers. All you need for proof is to just follow the smart money.

Note for you damn haters: yes, it’s down from a frothy high of $66,0000, but look at the normalized return over the past 15 years since Satoshi Nakamoto’s whitepaper.) In addition, it has has opened more than 400,000 debit cards and is opening as many as 75,000 per month, creating a whole other disruption risk we need to discuss.

Companies are turning to accelerators, funds, and labs to try to find the next big thing that will reduce fraud, speed up transaction times, and catch on with consumers. ” It publishes quarterly forecasts and whitepapers that focus on the changing influences of CIOs. GFT Technologies — Digital Innovation Lab.

Now, to avoid any cue card and teleprompter issues, we’ll just go with the written list again this year. According to CardFlight, only 42% of MasterCard and 52% of Visa cards are chip-enabled due to backlogged card producers and payment processors. And the winners are …. THE BANKING AWARDS. GonzoBanker of the Year.

On Wednesday the American Office of the Comptroller of the Currency (OCC)* followed up on its promise last December to introduce a national bank charter for Fintech bank startups by issuing a whitepaper on how to apply for a licence, the evaluation process and … The Boy who cried Wolf!

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content