This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence.

For more communitybanks, the latter strategy can fast-track digitization initiatives. This week’s look at the latest bank-FinTech tie-ups shows Banking-as-a-Service and other FinTech players embracing smaller regional and communitybanks to elevate small- to medium-sized business (SMBs) and corporate banking offerings.

Here’s how four communitybanks are thriving in this environment. This region has the kind of energy that draws people to a place and helps them and their businesses thrive. We spoke with four communitybanks in the southern half of Texas to learn how they are serving this buzzing region. By Mindy Charski.

Below, PYMNTS rounds up the latest solutions that FinTechs and lenders are developing to ease the PPP lending process for SMBs and FIs alike, with many initiatives focused on enabling regional and communitybanks to maintain a competitive edge against the biggest banks. Fresno First Bank. LendingTree.

Speaker: Brian Muse-McKenney, Chief Revenue Officer & Matt Simester, Cards and Payments Expert

In this new webinar, Brian Muse-McKenney of Episode Six and Matt Simester of Payments Consultancy Limited will explore the challenges regional and communitybanks have faced in implementing tailored credit card programs with flexible payment options as a tool to attract and retain the next generation of customers.

Teaching staff these KYC tips to make clients feel more comfortable In 2023, KYC procedures must both support CDD compliance and make sure your institution is a welcoming place for all customers. Members of Amish or sovereign citizen communities often have fewer government-issued IDs. Miss” and thus alienating nonbinary customers.

”Indeed, AI can be a tool that takes this mission to the next level.Let’s explore four key areas to help you harness the […] The post AI for Banks: A Starter Guide for Community and Regional Institutions appeared first on ABA Banking Journal.

Biggest regionalbanks should be held to same standard as the largest national institutions, says ICBA CommunityBanking Feature3 Feature Retail BankingComplianceCompliance/Regulatory

Rapid consolidation in the banking industry is creating a growing band of regionalbanks that find themselves stuck in a solution provider market that isn’t fully capable of serving them. As banks have consolidated, so have the technology partners serving them.

Bank of America ranks highest in banking mobile app satisfaction, reports JD Power Retail Banking Feature Lines of Business Technology Mobile Online Tech Management Feature3 CommunityBanking Consumer Compliance Customers.

Meanwhile, leaders at small banks recognize that their institutions play a vital role in helping community businesses and individuals not only weather uncertainty but also thrive. How can community financial institution leaders manage their challenges and seize their opportunities at the same time?

If communitybanks put in the effort to foster a sense of belonging, the result is a stronger workplace culture, greater employee loyalty and, ultimately, a better experience for customers. So, how can communitybanks build truly inclusive cultures, where everyone feels like they belong? Misti Stanton, Mercantile Bank.

For several years, while state-level legalization has expanded, access to traditional banks remains an issue thanks to their status as federally regulated entities. Today, however, the banking challenge has largely been solved. According to Muller, data is often at the heart of this issue.

214 | The number of banks surveyed in the PYMNTS Bank Innovation Readiness Index, in collaboration with payments solutions provider i2c. It also included banks outside this profile and represents a broad range of FIs reflective of the market.

This week’s look at the latest in bank-FinTech collaborations and open banking initiatives finds a focus on small business lending: In the U.K., Funding Options struck a data-sharing agreement with 20 alternative lenders to make SMB loan applications more efficient, while in the U.S.,

With a permissioned blockchain network , services can be shared between credit unions, which could improve identification authentication and compliance surrounding regulations, know your customer, lending and payments. Under the plan, credit union members would be able to access the CULedger via a digital credential dubbed MyCUID.

Survey also finds fewer than half of bank employees know what conduct and ethics controls are in place Compliance Management Compliance/Regulatory CommunityBanking Feature3 Financial Research Human Resources Feature Management Compliance.

The transition from compliance to consulting makes sense: tax season is just that, a “season,” and nearly 60 percent of respondents to a Sageworks survey indicated they saw an increase in total revenue by adding financial services to their accounting practice.

Proposed capital rules aimed at bigger institutions will force regional and larger communitybanks to consider ways to grow or seek an exit strategy, bankers and analysts predict.

In addition to these technology-oriented improvements, there are also a variety of process improvements that many banks can make that are cost-free. Moving all customers to digital statements, restructuring compliance reviews and employee onboarding are just some of the more popular efforts that banks are undertaking in 2023.

In its biannual report on supervision and regulation, the Federal Reserve Board noted an uptick in governance issues with large banks. Regional and communitybanks, meanwhile, were plagued by IT problems and risk management struggles.

A bill that would give regionalbanks a break on regulation was before the U.S. That change would become effective 18 months after the bill is enacted — though the SIFI designation immediately lift for banks with assets under $100 billion, according to a Height Research report by Ed Groshans, senior vice president at the firm.

Cross River Bank. Though not venture capital, the private equity raised for New Jersey-chartered communitybank Cross River Bank is noteworthy not only for its impressive price tag of $100 million, but for its reflection of investors’ support for financial institutions that collaborate with the tech startup scene.

For regional and communitybanks there has never been a more frustrating time to be a buyer versus a builder of financial technology. Communitybanks, regional players, and credit unions are all in the fight of their lifetime with the need to transform their business. Mandate #3: Build a next-gen I.T.

Changing customer banking habits means it’s more important than ever for communitybanks to use every tool at their disposal. Communitybanks may have longstanding relationships with their core vendors, but that doesn’t always mean they keep up to date on all the latest features and functionalities. “But

The ICBA and communitybank campaign to improve those rules has included a comprehensive study on their impact that was released before the CFPB announcement of its proposed changes, which are expected to be formally adopted. Of course, this communitybank victory is not the result of just one survey.

The ICBA and communitybank campaign to improve those rules has included a comprehensive study on their impact that was released before the CFPB announcement of its proposed changes, which are expected to be formally adopted. Of course, this communitybank victory is not the result of just one survey.

The CHOICE Act rolls back regulations that Sullivan said can pin down a communitybank and prevent it from serving its function. Communitybanks are spending more money and resources on hiring compliance people than they are on lending to their community,” he said. Banking Around Legalized Marijuana.

Communitybanks and credit unions would be forced to stop making short-term, small dollar loans if the Consumer Financial Protection Bureau's payday lending proposal is adopted, two trade groups said Monday.

It is important to note that 214 banks, excluding the top 25, participated in the Bank Innovation Readiness Index survey. These comprised regionalbanks, smaller commercial banks, communitybanks and credit unions, the majority having assets between $500 million and $5 billion. Methodology.

These services are provided through a variety of delivery systems including automated teller machines, private banking, telephone banking and Internet banking. We believe we can effectively compete as a communitybank in our market area and the niche markets we serve. We focus our marketing efforts in three areas.

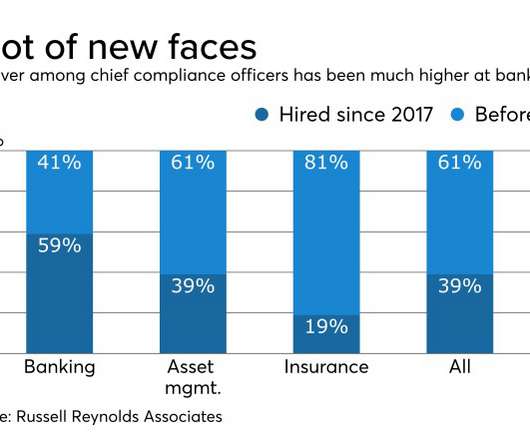

Banks had the highest turnover of chief compliance officers among the 100 largest financial services firms in the world, according to a recent study. Recruiters say that’s a function of changing job demands, high pressure and poaching by fintechs — plus old-fashioned demographics.

This suite of systems can take banks from chaotic and fragmented operations to a smart, scaled future. A striking dynamic has occurred among regional and communitybanks over the past 10 years: their assets have grown much faster than their maturity. 4: The GRC System Ugh!

Bankers and a key government supervisor say the downfalls of multiple regional lenders reminded regulators that traditional M&A is better for the industry than failed-bank-deals.

With all of our hubris about how great communitybanking is compared to national banks, we are not winning market share from them. All comments are my own, as his firm is a broker-dealer which would require a monumental amount of compliance review and disclosures. Edited for your clarity and context. AddingValue ? ?

A new Labor Department regulation designed to make more American workers eligible for overtime pay stands to add costs and slow hiring at communitybanks.

By Christopher DelporteA fintech startup has created what it claims is the first online bank-to-bank marketplace designed to help financial institutions mitigate asset risk.

Large enough to meet the needs of most customers yet small enough to escape some of the Dodd-Frank Act's most onerous compliance expenses, banks with assets of $2 billion to $10 billion are more profitable, as a group, than their smaller and larger counterparts, according to an analysis by Capital Performance Group.

A dozen banks from Arkansas to Virginia are nearing $10 billion in assets, where they will face higher compliance costs and caps on interchange fees. Mergers among those institutions could create a new class of regionalbank.

for $234 million for 162% of tangible book when regional targets were selling for 146% of tangible book. To qualify for listing, companies must meet high financial standards, follow best practice corporate governance, demonstrate compliance with U.S. And to do stock deals, your stock has to be considered valuable by the target.

The combination of higher regulatory expenses andreduced income from interchange fees is taking a toll on the profitability of banks with $10 billion to $50 billion of assets.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content