This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

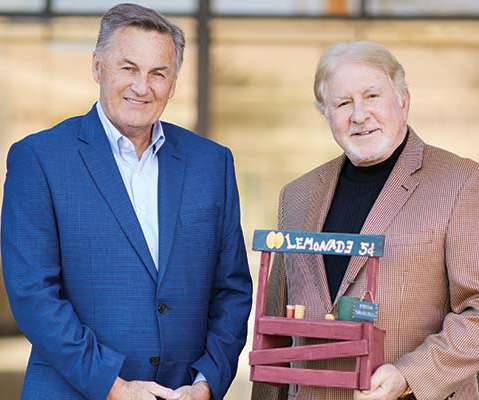

Inspired by the entrepreneurship of lemonade stands, Scottsdale CommunityBank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale CommunityBank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

This year’s winners: Left: Central Valley CommunityBank, People’s Choice Award; Middle: Kennebec Savings Bank, Exceptional CommunityBank Service Award; Right: Cross River Bank, Emerging Service Program Award. Exceptional CommunityBank Service Award. Kennebec Savings Bank.

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

We asked both leaders and staffers to tell us what makes their communitybanks stand out as employers. Key CommunityBank: Leading by example. Key CommunityBank. At the heart of Key CommunityBank’s work culture is connection. Greg Dennis, Key CommunityBank. “We

.; Bank of Montana, Missoula, Mont.; CNB Bank, Berkeley Springs, W.Va.; Midwest Bank, Norfolk, Neb. In our annual workplace survey, employees of ICBA’s best communitybanks to work for told us they benefit from engaging cultures, opportunities for advancement and innovative benefits. What great resignation?

Communitybanks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for communitybanks. But there’s plenty communitybanks can do to meet this challenge. William Atkinson is a writer in Illinois.

Following their stints as interns, Malvern Bank retained the talents of (L to R) Cody Sorenson, Keegan Wederquist and Adam Konfrst, hiring them as full-time, mid-level team members. These communitybanks share how they have (or haven’t) altered their hiring strategies. Eclipse Bank: Reputation matters. Total employment.

The total roster now claims more than 1,600 banks and credit unions domestically, said the site, even as 35 percent of retailers in the U.S. support Apple Pay.

ITMs and VTMs are popular retail banking innovations among communitybanks. What’s on the horizon for retail banking? We spoke with two communitybanks that have ramped up their services to meet—and exceed—the changing expectations of customers. So how are retail banks meeting this challenge?

The Peoples Bank helped the Jones family of Legacy Dairy in Hiseville, Ky., From left, Ally Jones; bank chairman, president and CEO Terry L. Last year, communitybank loan producers were faced with both record-low interest rates and a glut of deposits. The bank provides crop insurance to farmers in 11 states.

Whether achieved by internal or external resources, communitybanks provide valuable support for small businesses. By providing “bonus” services to small businesses, such as startup loan programs and referral services, communitybanks prove themselves to be reliable financial partners, with mutually beneficial results.

And the great news, according to “American Millennials and Banking,” a major new study commissioned by ICBA, is that Bauhs and the 80 million other people in his generational cohort are prime potential customers for communitybanks. This is really the moment for communitybanks to show that they’re a fit for millennials.

Communitybanks are vital providers of small-business credit because of their extensive local market knowledge and deep customer relationships. In Illinois, a loan participation plan by a communitybank “insourced” jobs to the local area from overseas. By Jessica Milano. million of their $5.1

We spoke with industry specialists about the priorities for communitybanks as they build a digital loan process for small businesses. It’s critical for communitybanks to have online loan applications, process automation staff skilled in digitization and more. Doing so can help communitybanks: Optimize the loan cycle.

billion-asset CNB Bank headquartered in Clearfield, Penn., We are providing banking options in areas that have been known as ‘bank deserts,’ which is very important to us as a communitybank.” This was an extensive process undertaken to bring the final product to the community,” says Noah.

A young entrepreneur prefers relationship communitybanking. which he still operates. In general, Meadows believes communitybanks can play an important role in helping young businesspeople. He talks monthly with a loan officer at First National Bank of Odon, his local communitybank. “He

Big-brand megabanks, the Visa and MasterCard networks, and big-box merchants had signed up to become partners with Apple’s universal retail smartphone app that uses Near Field Communication and tokenization technologies. So where do ballyhooed mobile banking and payments developments among the biggest players leave communitybanks?

Academy Bank COO Tom Kientz notes that the communitybank was eager to expand its deposit and loan services. Looking for an avenue to increase its deposit base, Academy Bank tapped into a market it hadn’t explored before: homeowners associations. William Atkinson is a writer in Illinois. Photo by Jason Tracy.

While most of Alpine Bank’s in-lobby “shops” are carried out here at its Glenwood Springs branch, the program also has an online element. It’s no secret why Alpine Bank’s mystery shopper program has helped the communitybank meet and exceed customer expectations over the past two decades. Name: Alpine Bank.

Increasingly, more digitally connected consumers are saying yes to that question with their communitybank. Some even assume their bank will interact with them however and whenever they want. For many communitybanks, telephone calls still generate the highest volumes of customer service interactions.

When Urban Partnership Bank in Chicago was born four years ago from the remains of a failed community development institution, its mission was revised and then revived again. That special charter allows the bank, one of 40 in the nation that is both a minority depository institution and a CDFI, to receive funding from the U.S.

Illinoisbank launches insurance premium financing sideline. In an era of exceptional competition with tight interest margins, many communitybanks are attempting to tap new lines of business. Triumph CommunityBank in Moline, Ill., billion-asset communitybankoperates.

And the great news, according to “American Millennials and Banking,” a major new study commissioned by ICBA, is that Bauhs and the 80 million other people in his generational cohort are prime potential customers for communitybanks. This is really the moment for communitybanks to show that they’re a fit for millennials.

Job seekers are in the driver’s seat across most industries, including communitybanking,” says Lindsay LaNore, group executive vice president and chief learning and experience officer for ICBA. However, communitybanks have a big opportunity to stand out from the crowd of potential employers.”. Put people first.

In fact, our directors don’t just show up for the monthly board meetings and committee meetings; they are very much engaged in the oversight of our bank. They are visionaries and stay involved; at the same time, they don’t meddle in the day-to-day operations of the bank. ROAA in 2015: 2.27 Assets: $105 million. Employees: 26.

We still have a high demand for cash,” says Tylynn Theis, vice president of Harvest Bank, a $130 million-asset communitybank in Kimball, Minn. Maybe the baby boomers and older [customers] have a little higher demand for cash, but really we see all ages still coming into the bank for cash.”. The cashier’s role.

Over the next three years, Anderson enrolled in all three of Community Banker University’s in-depth compliance certification training programs. I also benefit from the respect I get from our board and CEO, and definitely from the bank examiners. Bank security. Bank Secrecy Act/anti-money laundering. Compliance.

Ted Whitehurst, Providence Bank president and CEO, led the charge to open a new brick-and-mortar location of the Raleigh, N.C., communitybank during the pandemic. Providence Bank chose to open a new brick-and-mortar site during the pandemic, when many other businesses were ceasing operations or shutting down altogether.

A summary of the banks, their strategies, and links to their website are below. #1. Open Bank (OTCQB: OPBK) Open Bank commenced operations in 2005 as First Standard Bank in the Koreatown section of Los Angeles. They are built as a relationship bank serving the Korean community in LA and surrounding areas.

With the prevalence and importance of Internet-enabled devices increasing nearly everywhere, communitybanks should remember to expand the scope of their security policies and network monitoring to cover their hardware, according to computer security experts. which specializes in serving communitybanks. Upping IT audits.

When John Zimmer took over as president of HNB National Bank in Hannibal, Mo., The $396 million-asset communitybank had merged with another bank four years earlier, doubling the size of its branches, staff and operations, and Zimmer was convinced some unnecessary or overlapping expenses still existed.

billion of assets and operates eleven branches in the metropolitan Milwaukee market, a loan production office (LPO) in Minneapolis, Minnesota, and 45 mortgage banking offices in 21 states. The mortgage bank has more than 3x the employees of the bank. million, than it has in operating expense, at $95.0 So they grew.

Nasdaq: OSBC) Old Second is a single-bank holding company headquartered in Aurora, Illinois. billion of assets and operates twenty five branches in the western suburbs of Chicago. The Bank, Old Second National Bank, lost a whopping $156 million in 2009 and 2010. Summit also operates an insurance subsidiary.

In this feature, we’ll look at a number of ways you can continue to build trust—an especially crucial task as the pandemic continues, telecommuting persists and consumer banking practices evolve. But for most communitybanks, building a trustworthy brand isn’t a conscious effort. billion-asset communitybank.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content