This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

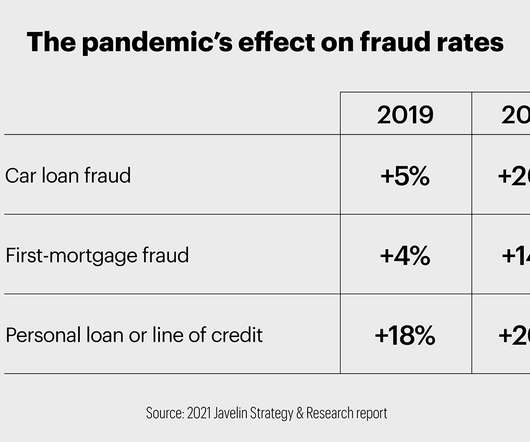

Experts say communitybanks can use education, biometrics and solid cybersecurity practices to fight this growing area of crime. Say a scammer calls a communitybank customer and gains their trust by using information obtained from a major data breach. By Elizabeth Judd. Examples of remote authentication fraud.

Here’s how communitybanks can enhance their payments offerings. of banks’ revenues come from payments. Payments account for up to 30% of bank revenue, and that income stream is under attack. As 2023 kicks off, communitybanks can respond to today’s payments landscape by addressing five key trends.

A career banker with multiple financial institutions, including the long-admired Mercantile from Maryland, Mike elevated up the credit and lending vertical to his current position. Mark Semanie, Maryland Market President, Wesbanco. Mark did not come into banking until his mid 30's.

The bank faced credit setbacks in the nation's capital and margin pressure this year. But it made a series of new hires to reduce risk and diversify its loan portfolio, preparing for a new era of demand as the industry awaits interest rate cuts.

The bank took a big hit on an office property in Washington, D.C., during the first quarter. This month, it filed a shelf registration statement for an offering of up to $150 million that could be used to bolster capital or refinance debt.

With the SBA’s Paycheck Protection Program set to re-opening for applications tomorrow, a Marylandbank CEO this weekend recounted his bank’s experience getting up and running during the early days of the program. The post MarylandBank CEO Reflects on First Round of PPP Applications appeared first on ABA Banking Journal.

Here’s what communitybanks need to know about these products and how they can take advantage of this model. Emerging as the latest form of point-of-sale (POS) lending, BNPL introduces new ways for consumers to make purchases and spread out their payments. BNPL: The communitybank play. By Colleen Morrison.

An event at EMS in June brought together (L–R) Clear Mountain Bank president/CEO Dave Thomas, ICBA president Rebeca Romero Rainey, FHLBank Pittsburgh president/CEO Winthrop Watson, and Tim Critchfield, EMS owner/president. Name: Clear Mountain Bank. Consider, for example, its commercial lending approach. By Mindy Charski.

Robust online mortgage websites embrace today’s lending challenges as well as consumer needs. When CommunityBank of Bergen County unveiled its online mortgage hub this summer, the bank put “ease of use” at the top of its goals for the site, says President and CEO Peter Michelotti. “I By Elizabeth Judd.

The bank cut its dividend, raised capital, hired multiple top executives and vowed to reduce its commercial real estate concentration after a bruising first half of 2024.

With vigor and a strong commitment to service, Ron Paul leads a rapidly growing communitybank in Maryland. Bank assets: $5 billion. Ronald Paul first encountered communitybanking as a real estate developer in the early 1980s. He became an enthusiastic advocate of relationship-based banking.

The Internet of Things, also known as the Industrial Internet, is where networked smart devices communicate to powerfully automate a multitude of complex tasks for both consumers and businesses, potentially including communitybanks. Both scenarios would communicate possible financial needs of the bank and its customers. “If

Me to a community banker: Why don't you offer more options than real estate secured lending to help fund early stage businesses? Banker: Because that's not communitybanking. I've been in this business over 20 years and still don't know the definition of communitybanking. I've got news for you.

Schwanhausser suggests that motivating online activities or games that help customers meet savings, investing and other money management goals—or perhaps understand more about banking, entrepreneurship or protecting personal information identity theft—can help build a financial safety net and lend themselves to game technology quite nicely.

The Bethesda, Maryland-based company called its success in luring a team from Capital One as its most "newsworthy" move to date executing a strategy aimed at diversifying its lending operation.

The Bethesda, Maryland, company projects increases in loans and deposits as its C&I lending strategy gears up. Criticized and past-due loans appear to be declining even with a jump in nonperforming assets.

That dynamic provides a unique opportunity for individual community bankers to tell their stories to their federal lawmakers, which has always been a vital part of getting ICBA’s pro-communitybanking legislative agenda enacted. As an example, “If X goes into effect, it would decrease my mortgage lending by X percent.”.

The old borrow short, lend long strategy. I want to read to you the FDIC’s conclusion from their An Examination of the Banking Crisis of the 1980’s and Early 1990’s. Who would’ve thought lending $1 million to a San Francisco cab driver to buy a house at 100% loan to value would go bad? Remember K Bank in Maryland?

through its subsidiary BNC National Bank, offers communitybanking and wealth management services in Arizona, Minnesota, and North Dakota from 16 locations. It also conducts mortgage banking from 12 offices in Illinois, Kansas, Nebraska, Missouri, Minnesota, Arizona, and North Dakota. What a ride! #3. BNCCORP, Inc.

Digital banking solutions for communitybanks and credit unions. A turnkey solution incorporating CRM, invoicing and payments into a simple solution for the business delivered through the bank’s digital banking solution. An industry leader in lending and benchmarking solutions for financial institutions.

Fallout from recent global events presents an obstacle to generating revenue for communitybanks. It’s certainly an interesting time to be a communitybank, but there are still plenty of ways to make efficiencies with an eye on profitability. ? But one of the biggest problems in communitybanking today is a fear of risk.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content