This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for communitybanks. However, for communitybanks, these challenges can also present some opportunities.

It would make no sense to risk the banks capital without adequate compensation. However, some banks are inadvertently taking risk without any additional revenue. However, with the current shape of the yield curve, banks generate no additional revenue by extending duration. But at SouthState Bank, we use a much simpler solution.

In our previous article ( here ) we analyzed the data on communitybank M&A and performance, and we concluded that there is no relationship between communitybank size and profitability, as measured by return on equity (ROE). While size isn’t correlated to profitability, operating leverage is.

Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Nearly all U.S.

What should you look for in a Business Lending Platform? This eBook explains the features of a Business Lending Platform that communitybanks should make their top priorities when evaluating any business lending software.

For more communitybanks, the latter strategy can fast-track digitization initiatives. This week’s look at the latest bank-FinTech tie-ups shows Banking-as-a-Service and other FinTech players embracing smaller regional and communitybanks to elevate small- to medium-sized business (SMBs) and corporate banking offerings.

This article is the second in a two-part series on top concerns and growth strategies of communitybanks. Everyone in the banking industry seems to be asking the same question these days: How can we facilitate growth? banks are moving back into commercial real estate (CRE) lending as the economy continues to improve.

Our recognition as the #3 communitybank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. Yet, the banking industry is at a turning point. My goal is to convince you to approve a pilot program that will cement our position as a leader in communitybanking.

In a previous article [ here ] we discussed why communitybanks need product managers to ensure that financial products and services are effectively developed, launched, and managed to meet customers’ evolving needs and the bank’s risk and profitability goals. Not all customers are the right fit for the product.

That’s even more true for communitybanks, which lack the resources larger FIs have to support modernization initiatives and technology investment efforts. At the same time, the logistical challenges and competitive pressures associated with digitization remain just as pertinent for communitybanks.

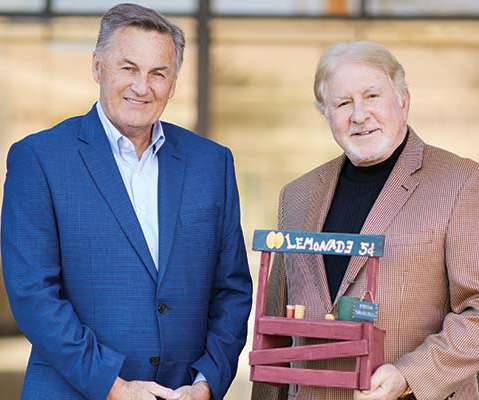

Inspired by the entrepreneurship of lemonade stands, Scottsdale CommunityBank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale CommunityBank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

Key Takeaways Financial institutions who want to maintain a healthy share of business lending this year and through potentially tougher economic times ahead want to be in the best position possible before trouble hits. Abrigo's Business Lending Readiness Survey found many processes stymie those efforts. learn more.

Community bankers need to understand their competitive landscape. Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help communitybanks differentiate their services and enhance their competitive advantage.

of digital banking customers said they switched to digital banking because of the pandemic. Source: 2021 Provident Bank survey. These days, there’s a lot to contend with as a communitybank, from changing consumer behaviors due to the pandemic to uncertainty surrounding the economy and inflation. Quick stat.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. download NOW Takeaway 1 The most popular blog posts on the Abrigo site reflect many of the priorities communitybanks and credit unions had in 2023.

Ken Finley, president of Johnson City Bank, in downtown Johnson City with Shannon Sultemeier, executive vice president (left); and Brenda Haynes, vice president/cashier (right). Here’s how four communitybanks are thriving in this environment. These include family-owned businesses, community businesses and operating companies.

For most consumers who have a checking account, savings account and maybe a mortgage, the regulations placed on their communitybank isn’t given a second thought. Two recent surveys addressing the communitybanking landscape have pointed to increasing regulations as the primary cause of stress for these institutions.

Historically, communitybanks have relied on net interest margin (NIM) instead of fee income to drive return on equity (ROE). In contrast, larger banks have emphasized non-interest income rather than NIM to boost ROE and revenue. Larger banks have historically operated on thinner NIM but higher fee income.

Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. WATCH Investment accounting compliance risks U.S.

Although the above example is a large bank, similar enforcement actions are being handed down to communitybanks. Key strategies to prevent BSA enforcement actions To prevent BSA enforcement actions, banks must prioritize proactive compliance measures. Provide timely updates in response to changes in regulations.

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

With consumer expectations seeming to evolve faster every year, communitybanks could consider partnering with a fintech to keep up with technological innovation. Those conversations, he says, centered around whether communitybanks could compete against this brash group of newcomers. Photo by Pogonici/iStock. Quick Stat.

We asked both leaders and staffers to tell us what makes their communitybanks stand out as employers. Key CommunityBank: Leading by example. Key CommunityBank. At the heart of Key CommunityBank’s work culture is connection. Greg Dennis, Key CommunityBank. “We

Small business credit analysis company PayNet is linking up with a communitybank to streamline SMB lending for the institution. In another statement, BNB Bank EVP and Chief Lending Officer Kevin L. ” Analysis has also found that communitybanks are playing a larger role in small business lending. .”

According to a recent survey from four Federal Reserve Banks, small regional and communitybanks have the highest approval rate for small business loans. The 2014 Small Business Credit Survey was a joint operation conducted by the Federal Reserve Banks of New York, Atlanta, Cleveland and Philadelphia.

Many communitybanks and credit unions are turning to small business loans as a source of loan growth. In their Spring 2016 Semiannual Risk Perspective , regulators have publicly acknowledged increasing risk in commercial real estate lending, so small business lending seems like it may be an alternative path.

.; Bank of Montana, Missoula, Mont.; CNB Bank, Berkeley Springs, W.Va.; Midwest Bank, Norfolk, Neb. In our annual workplace survey, employees of ICBA’s best communitybanks to work for told us they benefit from engaging cultures, opportunities for advancement and innovative benefits. What great resignation?

Personalized Touch with Efficient Service Can Boost LendingBanks and credit unions can boost business lending by combining a relationship focus with transaction-oriented processing. . Takeaway 1 Many banks and credit unions want to win more business loans but will face higher rates and more competitors.

Community bankers are largely positive about the future, based on the first results of a new index gauging business sentiment among the financial professionals who serve a critical role in local economies. How do you expect the regulatory burden on your bank to change over the next 12 months? Grow your loan portfolio. Learn More.

Silicon Valley is coming to banking? That happened long ago — just ask Silicon Valley Bank, a financial institution built to serve the world’s center of innovation. SVB claims it banks a staggering two-thirds Read More. Few bankers can claim better knowledge of what the tech giants are up to. Startups, you say?

Independent Banker ’s annual CommunityBank CEO Outlook survey reveals how communitybank leaders plan to leverage today’s deposit-laden banking environment to grow this year. Janet Silveria, CommunityBank of Santa Maria. So, what’s at the top of communitybank leaders’ to-do lists?

Loan providers share an infectious enthusiasm and growing optimism for one vertical’s prospects in 2022: commercial lending. Here’s how community bankers can take advantage of various sectors—including SBA lending—over the next 12 months. First Business Bank in Madison, Wis., billion asset communitybank.

JPMorgan Chase is planning the consolidation its corporate payment operations by combining small business (SMB) and large enterprise solutions, the Financial Times ( FT ) reported on Thursday (Jan. and internationally,” said Co-President and Chief Operating Officer Daniel Pinto in the memo.

For communitybanks and credit unions, their physical proximity to the small businesses they’re servicing is often pointed out as a major advantage these smaller players hold over the big banks, enabling these FIs to develop deeper relationships with their small to medium-size business (SMB) clients, anticipate their needs and establish trust.

Communitybanks are pushing for a stronger role with their small business (SMB) customers. However, through an embrace of FinTech collaboration and industry consolidation, communitybanks appear poised to further dispel assumptions of a lack of digitization. A Consolidating Industry. Strengthening SMB Ties.

But the latest initiatives reveal a growing interest in transforming internal processes, particularly among smaller banks looking to upgrade their core infrastructure and elevate small business lendingoperations. Yes Bank Woes See API Disruption. Bectran Augments Cash Application With API. Yet maturation is low.

These communitybanks are working to fix that through microlending programs. Now, some communitybanks are launching microlending programs to redress the balance. which operates $12 billion-asset OceanFirst Bank N.A. Jenny Bennett, market president at $850 million-asset Summit Bank in Eugene, Ore.,

Small communitybanks may not have the ample resources that Wells Fargo or Bank of America have to develop high-tech, experimental solutions internally. At least, Seacoast Bank VP and Digital Project Manager Jeff Lee and CEO Denny Hudson believe so. ” Florida-based Seacoast Bank has $3.5

Large financial institutions (FIs) are increasingly turning to FinTech firms and alternative lenders to augment their small business (SMB) offerings, but communitybanks are beginning to get on board with the partnership strategy , too. They’re very disciplined on credit and interest rate risk,” he said.

Think of banking and you might think of lending and deposits, where firms make money on the spread between what they pay savers and what they take in from borrowers. But banks cannot live on interest alone. Additional financial products and services must round out traditional banking activities.

Communitybanks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for communitybanks. But there’s plenty communitybanks can do to meet this challenge. Here are some ideas for strengthening fraud defenses.

Communitybanks are often the familiar faces of the financial services world, and when small businesses seek capital, their neighborhood financial institution can be a promising place to start. While they continue to play an important role in small business financing, the communitybanking market is drastically shrinking in the U.S.

Financial institutions that want to play in the small business lending sandbox need to bring their digital toys. article , former Small Business Administration administrator Karen Mills said communitybanks with strong small business customer bases that don’t find new ways to serve them digitally are going to face a “reckoning.”

One area of impact is small business finance and lending, with small businesses and lenders seeing a slowdown in demand. Small business lending platform Funding Circle commented on this effect in its latest earnings data, noting that there has been “some deterioration” in its higher-risk small business loan bands in the U.K.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content