This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for communitybanks. However, for communitybanks, these challenges can also present some opportunities.

Our analysis shows that an average communitybank can expect $9.7mm NPV of income (about 1% ROA) on a $100mm loan portfolio when the average loan life is seven years, versus only $5mm NPV of income (about 0.50% ROA) on the same portfolio where the average loan life is 2.3 years (both portfolios measured over a ten-year life).

It would make no sense to risk the banks capital without adequate compensation. However, some banks are inadvertently taking risk without any additional revenue. However, with the current shape of the yield curve, banks generate no additional revenue by extending duration. But at SouthState Bank, we use a much simpler solution.

This article is the second in a two-part series on top concerns and growth strategies of communitybanks. Part I focused on bankers’ greatest concerns, while this section will focus on growth strategies. Everyone in the banking industry seems to be asking the same question these days: How can we facilitate growth?

In our previous article ( here ) we analyzed the data on communitybank M&A and performance, and we concluded that there is no relationship between communitybank size and profitability, as measured by return on equity (ROE). The key insight is to understand how growth translates into bank efficiency.

We work with hundreds of communitybanks across the country that utilize forward rate locks to decrease risk, increase fee income, and stave off competition from national and regional banks. Tools for Forward Rate Locks The lending curve is currently flat. Boost non-interest income with loan and hedge fees.

Banks & credit unions recognize the importance of new deposits After years of consistent deposit growth, financial institutions have faced a shift recently, with deposits declining since 2022. Investing in digital solutions not only improves the customer experience but also positions communitybanks as forward-thinking financial partners.

You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective risk management and compliance." WATCH Takeaway 1 Many financial institutions are questioning where rates are headed and how to structure their ALM strategies accordingly.

For more communitybanks, the latter strategy can fast-track digitization initiatives. This week’s look at the latest bank-FinTech tie-ups shows Banking-as-a-Service and other FinTech players embracing smaller regional and communitybanks to elevate small- to medium-sized business (SMBs) and corporate banking offerings.

In a previous article [ here ] we discussed why communitybanks need product managers to ensure that financial products and services are effectively developed, launched, and managed to meet customers’ evolving needs and the bank’s risk and profitability goals. Not all customers are the right fit for the product.

How can community financial institutions thrive in 2021? Communitybanks provide unique and important banking services for their customers, but they also face significant obstacles. Takeaway 1 Communitybanks play an important role in the economy and their communities, but they face significant obstacles.

Innovation has always been important for communitybanks, but the driving force of digitization over the last decade has greatly sped up the pace, said Kevin Tweddle, chief innovation officer for the Independent Community Bankers of America ( ICBA ). Communitybanking is no exception. Leveling the Playing Field.

Therefore, the quarterly profile and Chairman Martin Gurenberg’s commentary on the industry are skewed by the performance of larger banks. In this article, we analyze the underlying data for communitybanks and focus on the Chairman’s view of the future of bank performance.

In our dealing with hundreds of banks and thousands of borrowers, we observe strategies and structures that have worked for our customers. We would like to share ten strategies that we and other communitybanks have effectively deployed to win bus

A profitability strategy has a lot to factor in given today’s uncertain market. Here’s what community bankers need to know when planning their budgets for the next year. of digital banking customers said they switched to digital banking because of the pandemic. Source: 2021 Provident Bank survey. Quick stat.

The current policy directions from the new administration are largely inflationary, and communitybanks should be paying attention and consider a loan-level hedge strategy. Many banks that survived the rapid interest rate hikes still struggled with net interest margin (NIM) compression caused by fixed-rate loans and securities.

Alloy’s Julieann Thurlow, CEO of Reading Cooperative Bank, said, “Communitybanks play a special role in the lives of our customers, but we don’t have the same IT and innovation budgets as the big banks to capitalize on that relationship.” This time around, Sweetbridge is using blockchain in a lending context.

Community bankers need to understand their competitive landscape. Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help communitybanks differentiate their services and enhance their competitive advantage.

Preparing for 2023 While communitybanks have until 2023 until they must comply with CECL, there is likely less time than expected. . While communitybanks have until 2023 until they must comply with CECL, there is likely less time than expected. 2023 CECL Deadline? Steps to Take This Year WATCH Webinar.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. download NOW Takeaway 1 The most popular blog posts on the Abrigo site reflect many of the priorities communitybanks and credit unions had in 2023.

These actions can result in costly civil penalties and reputational damage, so banks and credit unions should take proactive steps to ensure their BSA compliance programs are robust and effective. In a recent high-profile case , a major bank faced significant civil and criminal consequences for violating the BSA.

Some of the most pressing challenges facing communitybanks and credit unions in the current banking environment include narrow interest rate margins, increasing pressure from regulators, and competition with “too-big-to-fail” mega-banks.

We concluded that the market does not adequately compensate banks for credit and interest rate risks. Top-performing communitybanks deploy relationship banking. We define relationship banking as a model focused on a consultative banking approach. uses at our bank.

Small business (SMB) lending is big business for communitybanks , which are a popular destination for small business borrowers, thanks to strong approval rates on loan applications. But new analysis from the Federal Reserve has identified a reversal in communitybanks’ position in the small business lending market.

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

Automating SMB and commercial lending elevates your customer's experience From making it easier to apply to speeding up loan closings, automation can helps make business lending customers and staff happier. You might also like this on-demand webinar, "Strategies to grow your commercial loan portfolio." Digital lending.

The Concepts Lending Curve: A yield curve shows interest rates associated with different contract lengths for a particular interest rate instrument. While economists may use the shape of the yield curve to gauge future economic strength, bankers should pay particular attention to the lending curve.

For communitybanks and credit unions, their physical proximity to the small businesses they’re servicing is often pointed out as a major advantage these smaller players hold over the big banks, enabling these FIs to develop deeper relationships with their small to medium-size business (SMB) clients, anticipate their needs and establish trust.

.; Bank of Montana, Missoula, Mont.; CNB Bank, Berkeley Springs, W.Va.; Midwest Bank, Norfolk, Neb. In our annual workplace survey, employees of ICBA’s best communitybanks to work for told us they benefit from engaging cultures, opportunities for advancement and innovative benefits. What great resignation?

A new approach to loan protocols is just one way for communitybanks to grow in new and different directions. Amid changing economic conditions and rising rates, it’s a good time for communitybanks to re-evaluate their loan strategy with an eye on adaptability. David, CommunityBank Consulting Services, Inc.

Investments in financial technology have been increasing for years, but the events of the last 18 months have created a new sense of urgency for communitybanks and credit unions to fine-tune their digital strategies across the spectrum of various fintech investments.

Loan providers share an infectious enthusiasm and growing optimism for one vertical’s prospects in 2022: commercial lending. Here’s how community bankers can take advantage of various sectors—including SBA lending—over the next 12 months. First Business Bank in Madison, Wis., billion asset communitybank.

Communitybanks are pushing for a stronger role with their small business (SMB) customers. However, through an embrace of FinTech collaboration and industry consolidation, communitybanks appear poised to further dispel assumptions of a lack of digitization. A Consolidating Industry. Strengthening SMB Ties.

Large financial institutions (FIs) are increasingly turning to FinTech firms and alternative lenders to augment their small business (SMB) offerings, but communitybanks are beginning to get on board with the partnership strategy , too. They’re very disciplined on credit and interest rate risk,” he said.

Small Business Loans | 5 minute read Key Takeaways Credit unions' small business loans hit a record low, while small business lending continues to remain strong at big banks and communitybanks. Going digital can help reduce the cost of small business lending and capture more member business loans.

As we kick off this year’s lending issue, I want to pause for a moment to reflect on just how much lending has changed. But communitybanks have adapted to address that shift. By implementing these new strategies, we have focused on what matters most: our customers. Rebeca Romero Rainey. President and CEO, ICBA.

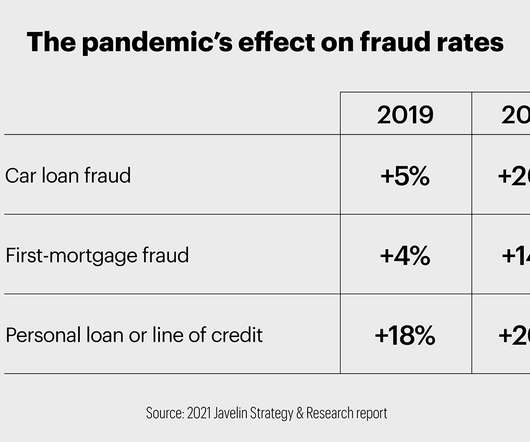

Experts say communitybanks can use education, biometrics and solid cybersecurity practices to fight this growing area of crime. Say a scammer calls a communitybank customer and gains their trust by using information obtained from a major data breach. By Elizabeth Judd. Examples of remote authentication fraud.

Communitybanks are often the familiar faces of the financial services world, and when small businesses seek capital, their neighborhood financial institution can be a promising place to start. While they continue to play an important role in small business financing, the communitybanking market is drastically shrinking in the U.S.

Think of banking and you might think of lending and deposits, where firms make money on the spread between what they pay savers and what they take in from borrowers. But banks cannot live on interest alone. Additional financial products and services must round out traditional banking activities.

It’s no surprise, then, that communitybanks, credit unions, and other financial institutions with recent exams have described how regulators “came down hard on liquidity,” she said. Both static and dynamic scenario analyses can show how different strategies hold up under stress. What if overnight, you had no outlet for them?

For decades communitybanks have structured fixed-rate loans with adjustable features – the most popular structure is a ten-year fixed-rate loan with a five-year reprice. With short-term interest rates expected to rise through 2022, many communitybanks are reconsidering their ALCO strategies.

Just days after the Federal Reserve released a report highlighting the changing role of small business loans at communitybanks, the latest Biz2Credit Small Business Lending Index published, suggesting small and medium-sized business (SMB) lending at small banks remains strong. The Index, released Wednesday (Oct.

Automation is the theme that best describes Chesapeake Bank’s innovation roadmap for 2019, Kevin Wood, managing director of the state-chartered communitybank’s business lending division, Cash Flow, told Bank Innovation. “One

What it means for communitybanks is clear. Throughout the near future, similar market volatility and uncertainty is likely to plague mortgage lenders, calling on communitybank leaders to develop new strategies to aging challenges. Developing leaders in mortgage lending.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content