This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The nation’s millennials—the biggest and most diverse generation of customers in our nation’s history—account for more than $1 trillion in annual purchasing power. And according to ICBA’s recently released 2014 American Millennials and Banking Study, this generation represents a major opportunity for communitybanks.

Communitybanking can be one of the most rewarding and most challenging areas of financial services in which to work — that’s the view, anyway, of Rebeca Romero Rainey, president and CEO of Independent Community Bankers of America (ICBA) , who recently joined the nation’s leading advocacy organization that exclusively represents communitybanks.

However, there may be an opportunity to get more contactless cards into the hands of consumers — an opportunity that involves communitybanks and is backed by financial incentives. ICBA Bancard’s 1,600 communitybank customers have issued more than 7.3 ICBA Bancard’s 1,600 communitybank customers have issued more than 7.3

As house prices skyrocket, student loan debt grows and wages stagnate, many Gen Zers and millennials are watching their homebuying dreams move out of reach. But there are ways communitybanks can help mortgage-seekers get on the property ladder. So how can communitybanks help? By Beth Mattson-Teig.

Understanding these attitudes and using them to inform marketing messages enables communitybanks, regional banks and credit unions to better serve their customers. How are Gen X, Millennials, and Gen Z defined? The experiences of every generation are characterized by their behaviors involving finances.

It also analyzes why younger investors like millennials have remained reticent to invest and how the health crisis could affect this generation’s spending and saving habits, especially as legacy disbursement methods such as paper checks continue to fall out of favor. Millennials have been hit especially hard, with one study finding that 5.6

Are communitybanks missing the chance to climb aboard the faster payments train? With various banks and FinTechs producing innovative solutions — like mobile banking and P2P tools aimed at improving the speed of payments — the pressure is on for communitybanks to keep up. faster payments system.

Everywhere you look, it seems, there are articles about Millennials: Millennial workers, Millennial customers, Millennial homeowners, Millennial voters. And banks and credit unions looking to grow business loan portfolios , especially, can benefit from insights into Millennial entrepreneurs.

In Europe, a group of seven banks tapped technology firm IBM to build a blockchain platform for the consortium in an effort to make global trade simpler and more streamlined for smaller businesses. Communitybanks meet the millennial generation.

Think of banking and you might think of lending and deposits, where firms make money on the spread between what they pay savers and what they take in from borrowers. But banks cannot live on interest alone. Additional financial products and services must round out traditional banking activities.

The program aims to accelerate the integration and deployment of digital banking technologies and to improve member experiences. Further collaborations could be possible if credit unions and communitybanks can work better together, according to J. Helping CUs Engage and Retain Millennial Talent . The good news?

As an early-career CPA, Carissa Rodeheaver began her communitybanking career as a trust administrator nearly three decades ago. Now, she's at the same bank, as chairman, president and CEO of Oakland, Maryland-based First United Bank and Trust.

The fourth season of the ABA Banking Journal Podcast kicks off with Minnesota communitybank CEO Andy Schornack. The post Podcast: Giving Emerging CommunityBank Talent ‘Opportunities to Shine’ appeared first on ABA Banking Journal.

If communitybanks put in the effort to foster a sense of belonging, the result is a stronger workplace culture, greater employee loyalty and, ultimately, a better experience for customers. So, how can communitybanks build truly inclusive cultures, where everyone feels like they belong? Misti Stanton, Mercantile Bank.

Out of Mom and Dad’s basement, millennials are primed to become your next best customers. Bauhs is on the tail end of the “millennial” generation, which is commonly defined as those born between 1980 and 2000. This is really the moment for communitybanks to show that they’re a fit for millennials. By Ed Avis.

Communitybanks and credit unions are feeling the pressure to boost their digital card services or risk losing customers to megabanks and digital challengers, Ondot Systems ’ Chief Strategy Officer Todd Lesher told PYMNTS in a recent discussion. It’s a story told by the data itself, Lesher said. Square announced $1.3

Nearly every single consumer uses an institution that provides all of those services as their primary bank. Ninety-two percent of consumers count their primary bank as either a national bank, regional/communitybank or credit union. of consumers report that their primary bank is a digital-only bank (4.2

Derek Williams, president and CEO of Century Bank & Trust in Milledgeville, Ga., wanted to be a financier before finding his way to communitybanking. He has served as president and CEO of $365 million-asset Century Bank & Trust in Milledgeville, Ga., now part of Bank of America, before moving to Griffin, Ga.,

For communitybanks and credit unions, their physical proximity to the small businesses they’re servicing is often pointed out as a major advantage these smaller players hold over the big banks, enabling these FIs to develop deeper relationships with their small to medium-size business (SMB) clients, anticipate their needs and establish trust.

Out of Mom and Dad’s basement, millennials are primed to become your next best customers. Bauhs is on the tail end of the “millennial” generation, which is commonly defined as those born between 1980 and 2000. This is really the moment for communitybanks to show that they’re a fit for millennials. By Ed Avis.

The meetings also support the mission of the CBA which is the preservation and development of local, independent communitybanks in Georgia as well as the philosophy of hometown banking. The CBA has approximately two hundred communitybanking members. Hello, I’m a Millennial. percent since 1992.

The meetings also support the mission of the CBA which is the preservation and development of local, independent communitybanks in Georgia as well as the philosophy of hometown banking. The CBA has approximately two hundred communitybanking members. Hello, I’m a Millennial. percent since 1992.

Understand and meet the desires of millennial borrowers, who will constitute 75 percent of the workforce by 2025. Battle increased pressure from alternative lenders and fintech, which means the process at banks needs to be fast and competitively priced. Communitybanks worry they are in a lose-lose situation.

How millennials will accelerate innovation and technology change. You recognize one of today’s most prominent technology dilemmas for communitybanks: It’s the great mobile divide. Millennials, who will make up half the U.S. Millennials, who will make up half the U.S. By Paul Schaus. that processed $1.3

But how far are they willing to go to do their banking on small mobile devices? A consensus says that the future banking customer relationships—particularly for millennial consumers—will orbit to one degree or another around mobile technology. s entry into the payments business with Apple Pay. Ed Bachelder, payments consultant.

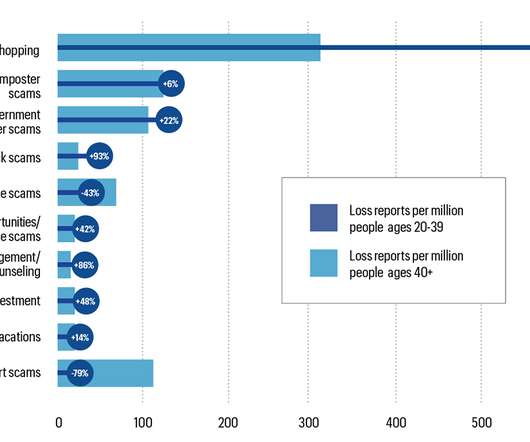

By identifying the preferred banking and spending habits of different generations, scammers can tailor how they reach their targets. We look at communitybanks’ options for fighting this type of crime. Reports about fraud losses: Millennials vs. people 40+. Millennials. By Katie Kuehner-Hebert. Baby boomers.

Texting millennials enters their private zone. Ask permission before texting or emailing them, and don’t abuse the privilege of your direct access with over-communication. Millennials want to be acknowledged. But do communitybanks know the unwritten rules of successfully engaging with millennials?

Texting millennials enters their private zone. Ask permission before texting or emailing them, and don’t abuse the privilege of your direct access with over-communication. Millennials want to be acknowledged. But do communitybanks know the unwritten rules of successfully engaging with millennials?

Both in daily life and in school, millennial parents want to rear children who understand wants vs. needs. The post A role for banks: Helping millennials teach their kids about money appeared first on ABA Banking Journal.

Sometimes the very challenges millennials introduce — whether it is seeking more benefits, demanding flexible schedules or asking for frequent feedback on performance — can turn banks into better places to work for employees of all ages.

The PPP might have been the first time many community financial institutions saw such clear returns on digitization investments, but the same automation and efficiency gains can be found in other end-to-end lending solutions. A relationship-based, community focus in a digital world.

Are your primary customers millennials, demanding mobile banking services? Try technology Sageworks Lending Solution helping communitybanks and credit unions grow Are alt-lenders catching up to banks on borrower experience? Do customers want a faster or more user-friendly approval cycle?

. -14% of SMEs using a large global bank have switched providers in the last year, while even more told FIS they are considering doing so in the next year. and Europe are looking at switching banks to access more high-tech services, like faster payment capabilities. -48%

“Why switch from Wells [Fargo] to Bank of America when you’re getting essentially the same experience?” As the demographics of entrepreneurs and freelancers continue to shift toward millennials and younger professionals, Merritt told PYMNTS that dissatisfaction with traditional FIs is likely to persist. he recently said.

Millennials, who alreadymake up a third of banked consumers in America, are used to transacting life in clicks and swipes. Institutions must embrace their needs now or risk extinction.

And that, Passione said, is an opportunity for lenders who, in the years since the Great Depression, have found themselves struggling to build relationships with millennial consumers and who have taken a sort of “chilly” outlook toward traditional financial institutions (FIs). There are currently 13,000 communitybanks in the U.S.,

Millennials this…”, “Small businesses that…”, Communitybanks are…”. Two current examples illustrate: The Use of AI in Banking is About to Explode. While referring to a small number of communitybanks interviewed for the article, it projects those results on the entire communitybank population.

There’s nothing more suitable for technology disruption than traditional small business banking. And there’s no better way to target Millennial entrepreneurs than with the technology they crave to help them in their business pursuits. Financial institutions are taking notice.

The inconsistency between what millennials say on surveys and their actual behavior should make bank marketers skeptical about building programs around such research.

Millennials came of age in the wake of the Great Recession and have developed a hardened skepticism about banks. For banks to attract them as employees, it's going take more than a promise of work-life balance.

Most financial professionals would agree that in recent years, we’ve been inundated with articles and reports containing tips and tricks for capturing the loyalty of the Millennial generation.

Most communitybanks and credit unions have only one app, their banking transaction app. Hawaii National Bank’s Hawaii Score enables existing bank customers and non-customers the capability to access a TransUnion credit report and score without the need for a credit card or an existing account with Hawaii National Bank.

It’s not a “Millennial thing.” Focus on digital marketing and social media , supplemented with physical outreach to drive digital , such as enhanced contact centers, bank-at-work programs, trade shows, art exhibits and other outreach. About one-third of communitybanks are planning to add or replace this technology.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content