This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

“Liberation Day” brought a 10% baseline tax on all imports plus a 15% to 49% tariff rate on a defined set of nations (below). The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for communitybanks.

Say "thank you" this National FinCrime Fighter Day BSA professionals and financial crime fighters are tasked with the challenge of protecting our financial system daily. October 26 is National Financial Crime Fighter Day , and it’s the perfect time to pause and applaud everything these professionals do. It’s about relationships.

This year’s winners: Left: Central Valley CommunityBank, People’s Choice Award; Middle: Kennebec Savings Bank, Exceptional CommunityBank Service Award; Right: Cross River Bank, Emerging Service Program Award. Exceptional CommunityBank Service Award. Kennebec Savings Bank.

Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help communitybanks differentiate their services and enhance their competitive advantage. Analyzing the competition can also help a bank be realistic about which products it can sell and at what price.

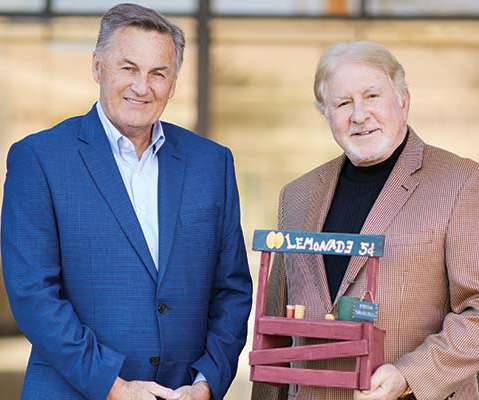

Inspired by the entrepreneurship of lemonade stands, Scottsdale CommunityBank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale CommunityBank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

Most nationalbanks scored relatively well. Communitybanks, not so much and the majority of banks can still not open an account digitally. The Problem with Todays Bank Websites Current bank websites are designed for human navigation. Declarative Action Intents : Publish available actions (e.g.,

Communitybanks are voicing their frustration with what they say is a lack of competition in the market for corporate bank technology providers, reports in The Wall Street Journal said Thursday (April 11). ” Fiserv, FIS and Jack Henry have secured 90 percent of U.S.

Connect with an expert Common fraud schemes Check fraud Check fraud is one of the most concerning fraud trends for communitybanks in 2025. As mentioned above, a strong fraud prevention plan includes proactive customer outreach, security alerts, and educational resources on phishing scams, identity theft, and safe banking practices.

The right technology tools can help institutions manage both regulatory compliance and risk exposure across various investment types, including fixed-income securities, structured notes, derivatives , and funding instruments. You might also like this on-demand webinar, "Winning the deposit game."

is set to see its first new communitybank in decades, as the Federal Deposit Insurance Corporation (FDIC) lent its approval for MOXY Bank to launch in Washington, D.C. With clearance to move forward with its plans, the communitybanking landscape will see its first new industry player in years.

Small Business Administration What creates two out of three net new American jobs; produces close to half of our nation’s goods and services (nonfarm private GDP); and can be found, coast to coast, in every small town, big city and rural enclave? Tune in all week for live-streaming , beginning at 7:30 p.m. Every business starts small.

Executive committee members tell us what advocacy issues they’ll be focused on during their terms, while board members share their words of wisdom for up-and-coming community bankers: themselves. To sum it up, these leaders are all in and all heart for communitybanking. We are not Wall Street banks—we are communitybanks.

Why don''t we play a critical role in solving the nation''s retirement problem? It called for the establishment of USA Retirement Funds to re-establish pension funds as part of the three-legged stool of social security, pension, and personal savings. The US Government already shares with Social Security. that reads.

My bank’s tagline is ‘Where dreams meet solutions,’ and it serves as my guiding inspiration at the bank and, now, at the national level. As community bankers, our customers depend on us to keep their dreams alive. Thankfully, that glass-half-full attitude comes naturally for community bankers. Innovation.

Communitybanks tout themselves as better than national and regional banks because of how close they are to their communities. But this opinion ignores the generations of history many banks across our great land have built. When the bank opened in 1905, Hallstead was already a thriving community.

However, that publication, directly and indirectly, identified three discrete risks affecting communitybanks. We will outline what we think community bankers should glean from this publication. Risks to the CommunityBanking Sector Moody’s identified three risks to the banking sector, including risks to communitybanks.

The Peoples Bank helped the Jones family of Legacy Dairy in Hiseville, Ky., From left, Ally Jones; bank chairman, president and CEO Terry L. Last year, communitybank loan producers were faced with both record-low interest rates and a glut of deposits. The bank provides crop insurance to farmers in 11 states.

Nonetheless, with the recent collapse of sizeable regional banks, regulators, investors, analysts, accountants, and bankers are now scrutinizing the fair value of banks’ securities and loan portfolios. This development should strongly motivate communitybanks to consider the benefits of loan-level hedging.

However, we would like to identify one important macroeconomic variable that will affect the banking industry regardless of the makeup of the legislative and executive branches of the US government. Regardless of who wins, our national debt will continue to increase, and communitybanks should be prepared for its consequences.

To regain some of that ground, Connie Davis, senior vice president at FIS , told PYMNTS in a recent interview, FIs — particularly credit unions (CUs) and communitybanks — must transform the way they think about digital offerings and connected experiences. That means they can compete more effectively against digital-only competitors.

However, communitybanks, in particular, face challenges in quantifying risk and applying compliance measures using a risk-based methodology, Brewer said. A formal requirement for institutions to develop and update risk assessments is among the expected changes.

The current policy directions from the new administration are largely inflationary, and communitybanks should be paying attention and consider a loan-level hedge strategy. Many banks that survived the rapid interest rate hikes still struggled with net interest margin (NIM) compression caused by fixed-rate loans and securities.

Furthermore, high federal government debt does not just lead to higher interest rates but also poses economic, nationalsecurity, and social challenges. Federal Debt – Impact Banking The path of the federal debt is already changing economic and public dynamics. With time, these changes will only amplify.

One possible solution to this dichotomy is for banks to offer interest rate swaps to hedge individual loans. This article will review domestic banks’ adoption of interest rate swaps. Next week’s article will consider the challenges and possible solutions for communitybanks to adopt loan hedging programs.

Credit Option: Lenders realize the unfavorable circumstances of a loan workout, and this leads to the largest credit option in banking – the ultimate credit option is the debtor’s ability to “hand the creditor the key to the building” and convert a secured loan into an equity stake. First is a declining balance provision.

Many communitybanks today are willing to underwrite real estate secured loans on just two metrics: debt-service-coverage ratio (DSCR) and loan-to-appraised value (LTV). Banks typically approve credits above 1.20x DSCR and below 75% LTV – with many loan-specific factors that may skew these acceptable levels.

financial institutions as they scrambled to apply for Paycheck Protection Program (PPP) loans under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. Lendio already secured its approval to facilitate PPP loans, the alternative lender said, noting that small businesses can now apply for a PPP loan on the Lendio platform.

CommunityBank of the Bay. Community First Credit Union (OH). Evans Bank. Federated Bank. First Bank of Boaz. First NationalBank of Milaca. Grand Savings Bank. Greater Cleveland Community Credit Union. Greenleaf Wayside Bank. Hometown CommunityBanks.

People’s United Bank, which operates across Connecticut, southeastern New York state, Massachusetts, Vermont, Maine and New Hampshire, recently demonstrated the growing interest of communitybanks to collaborate with FinTechs to expand their product offering — just as larger national and multinational financial institutions (FIs) do.

To that end, earlier this month FinTech firm SoFi made the leap beyond San Francisco to Hong Kong, having bought online brokerage firm 8 Securities. The 8 Securities deal comes a few weeks after SoFi said it would spend $1.2 percent of consumers are either “very” or “extremely” likely to use or already use nationalbanks, and 60.1

Community bankers need to practice realistic loan pricing discipline. However, we need to understand the meaning of pricing discipline and its effect on communitybank performance. This is strong evidence that communitybanks are pricing to an arbitrary minimum credit spread in this set of loans.

I was at a strategic planning retreat a few weeks back where a colleague lauded the concept of bankers getting back to plain vanilla communitybanking. Is the premise that doing "plain vanilla" banking acceptable? Valley National had an ROA in the fourth quarter of 1.08%. I hear and read this often. I doubt it.

#2 Northeast Bank (NasdaqGM: NBN) Northeast Bank is a full-service bank headquartered in Portland, Maine that had $3.9 It has a nationwide digital bank, ableBanking, that offers online savings products to consumers nationwide to assist in funding its nationwide lending program. million in net income for an ROA of 0.73%.

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act) includes the following key provisions that affect financial institutions and regulation of financial institutions: Section 4003 – Emergency Relief and Taxpayer Provisions.

The need for a known, reliable brand creates an excellent opportunity for communitybanks to help small business customers while building deposit balances. Communitybanks can now white label this same product to onboard and process employee retention tax credits for the bank’s small business customers AND prospects.

In a reported phishing campaign that began last month, Bank Secrecy Act (BSA) officials at credit unions in the U.S. The emails were reportedly only sent to certain anti-money laundering (AML) contacts, leading some to question if the National Credit Union Administration (NCUA)’s non-public data had been accessed, Krebs On Security reported.

The total roster now claims more than 1,600 banks and credit unions domestically, said the site, even as 35 percent of retailers in the U.S. As has been reported, Apple Pay is also available internationally in, among other nations, Australia, China, Hong Kong, Japan, Spain, the U.K. support Apple Pay. and Switzerland.

But given the rise of neobanks — FinTechs that are using banking services as the foundation for new ecosystems and Big Tech, which is exploring ways to extend their reach into banking and financial services — we thought we’d go back to first principles and ask consumers that simple question in relation to their primary banking relationship.

As usual, it was full of insight that every community banker should consider. Our focus is on information that pertains to the communitybanking industry. The bank aims to be a responsible citizen at the local level in every community where it lends and takes deposits. 1) The Fed May Hike More Than Expected.

Increasing Deposit Balances and Profit Consider this case study – customer acquisition costs for a company that provides security guards and patrol services are about $8,000. The average security company has about $80,000 in deposit balances, while the average trade association has about $501,000 in balances.

In a previous article ( here ), we discussed why commercial loan prepayment protection would be a critical return on asset (ROA) driver for communitybanks in 2023. We outlined the four main reasons why prepayment provisions increase profitability for banks. The greater fool theory breaks down in a recession.

Communitybanks and credit unions partnered with their communities to help families and businesses through these unprecedented times , causing spikes in consumer fraud that must be faced head on. To zero in on suspicious activity, typologies can be used to more accurately assess behaviors.

He said that while small banks, credit unions (CUs) and regional players deeply fear being swept aside by the great digitalization wave that the pandemic has set off, their concerns aren’t actually unique to the financial industry’s smaller end. Inherently, they trust their banks more.”. The Three Things Smart FIs Must Offer.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content