This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

“Liberation Day” brought a 10% baseline tax on all imports plus a 15% to 49% tariff rate on a defined set of nations (below). The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for communitybanks.

We work with hundreds of communitybanks across the country that utilize forward rate locks to decrease risk, increase fee income, and stave off competition from national and regional banks. National lenders have been using forward rate locks for decades, and these instruments can take many forms.

Over the last 15 years, an ever greater percentage of communitybanks have embraced some form of interest rate hedging. Approximately 1,000 banks in the country use some form of hedging products to manage risk, generate fee income, or provide product offerings demanded by their customers. Loan-level Vs. Balance Sheet Hedging.

Over the last 15 years, an ever greater percentage of communitybanks have embraced some form of interest rate hedging. Approximately 1,000 banks in the country use some form of hedging products to manage risk, generate fee income, or provide product offerings demanded by their customers. Loan-level Vs. Balance Sheet Hedging.

Communitybanks’ use of swaps (banks’ primary tool to hedge interest rate risk on loans) has increased substantially over the last ten years. Meanwhile, communitybanks face net interest margin (NIM) and fee income pressure. Only 304 banks (or 6.7% of the total) used swaps directly.

communitybank management team. The CLO was lamenting how he was losing quality loans and deposits to three aggressive nationalbanks in the territory. While this communitybank is not aggressively pricing new loans, losing this commercial credit with a substantial deposit relationship was painful.

Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help communitybanks differentiate their services and enhance their competitive advantage. Analyzing the competition can also help a bank be realistic about which products it can sell and at what price.

The current policy directions from the new administration are largely inflationary, and communitybanks should be paying attention and consider a loan-level hedge strategy. Many banks that survived the rapid interest rate hikes still struggled with net interest margin (NIM) compression caused by fixed-rate loans and securities.

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

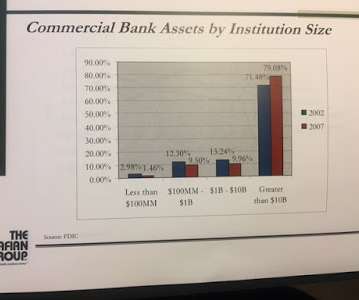

In recent months, the momentum around reducing the regulatory burden on the nation’scommunitybanks has continued to gain steam. There are more than 6,000 banks and thrifts under $10 billion in assets and they are often less equipped to deal with complexities brought by additional regulations.

Clockwise from top left: Grand Ridge NationalBank, Wheaton, Ill.; Community Financial Services Bank, Benton, Ky.; Bank of Montana, Missoula, Mont.; CNB Bank, Berkeley Springs, W.Va.; Midwest Bank, Norfolk, Neb. Can Bank of Montana’s success be replicated? Grand Ridge NationalBank.

In June of 2008 I gave a speech titled "The Death of the CommunityBank" and in that speech I made predictions. Prediction: The General Bank will become extinct. Much like competitors nip at communitybanks' customers. Eighteen percent of that group opened an account at a digital bank. Result: Mixed.

For decades communitybanks have structured fixed-rate loans with adjustable features – the most popular structure is a ten-year fixed-rate loan with a five-year reprice. With short-term interest rates expected to rise through 2022, many communitybanks are reconsidering their ALCO strategies.

In Q2/24 the average return of asset (ROA) for communitybanks (under $10B in assets) was 1.08%. But within the communitybanking sector, performance varied among banks significantly and a large swath of banks need to improve ROA. of communitybanks reported negative ROA. Another 16.2%

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

Deposit costs and liquidity remain a challenge for some communitybanks as competition for core funding remains intense. The graph below compares the liquidity ratio for communitybanks (under $10B in assets) and banks over $100B in assets. Communitybanks do have a few strategies for mitigating COF pressures.

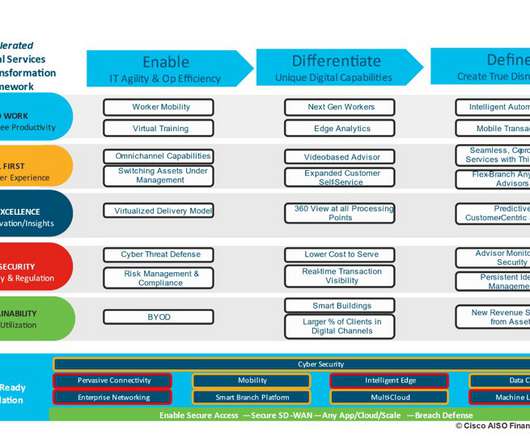

As a change agent serving the financial services industry for over 20 years, it is a great privilege to collaborate with Bank, Insurance, and Wealth Management institutions to devise and execute digital transformation strategy, solve complex business problems, and leverage technology to strengthen business results.

This development is very important to communitybanks, as their efficiency ratio also increased, but to 61.63%. The nationalbanks have already indicated how they plan to reverse the efficiency ratio increase – through headcount reduction. What is Driving the Efficiency Ratio at CommunityBanks?

With megabanks spending billions on digital investments each year, regional and communitybank executives understand they cannot compete on resources. Instead, these players are focusing on specific niches, brand strategies and community connections to differentiate themselves. Appoint Digital Ambassadors.

Source: FRED With deposits trickling back into the banking system and the promise of a potential rate cut this year, banking executives are experiencing a glimmer of hope. Instead, it’s time to build deliberate strategies to ensure a sustainable approach to deposit growth. Optimize pricing strategies.

This strategy is used for various reasons discussed further in this article. Recently, larger lenders, including Bank of America, JPMorgan, Goldman Sachs, and Wells Fargo, have announced that they are seeing an elevated appetite for forward rate locks on loans for future anticipated commercial borrowings.

Last week we wrote about loan-level vs. balance sheet hedging for communitybanks and provided our loan proposal generator ( HERE ). We compared and contrasted the two strategies and sized the market for communitybanks. We also shared a table that summarized the two strategies.

Since its founding in Evansville in 1834, Old NationalBank has focused on communitybanking by building long-term, highly valued partnerships and keeping our clients at the center of all we do.

smaller communitybanks and credit unions (CUs) stepped up to the plate and, according to the Small Business Association (SBA), ended up facilitating more than half of PPP loan volume to SMBs. That's good news for communitybanks and credit unions, which could see a wave of new SMB customers and members in the coming months.

However, that publication, directly and indirectly, identified three discrete risks affecting communitybanks. We will outline what we think community bankers should glean from this publication. Risks to the CommunityBanking Sector Moody’s identified three risks to the banking sector, including risks to communitybanks.

In two recent articles, we reviewed the banking industry’s deposit behavior with regard to cost of funding earning assets (COF) ( HERE ), and we compared how communitybanks’ COF behaves relative to nationalbanks in a rising interest rate cycle ( HERE ). A graph for SouthState Bank appears below.

ABA announced six banks are the recipients of the 2024 Brand Slam Awards, which honor exceptional bank marketing strategies. The post ABA recognizes six banks with nationalbank marketing awards appeared first on ABA Banking Journal.

A new approach to loan protocols is just one way for communitybanks to grow in new and different directions. Amid changing economic conditions and rising rates, it’s a good time for communitybanks to re-evaluate their loan strategy with an eye on adaptability. David, CommunityBank Consulting Services, Inc.

OCC Handbook (Section 203): Investment Securities The National Credit Union Administration (NCUA) also emphasizes that a credit unions board must take full responsibility for investment oversight , ensuring proper reporting structures are in place.

We recently worked with a communitybank in the Southeast that wanted to win a piece of credit business for a manufacturing company. The manufacturing company had a long-time relationship with a nationalbank and the communitybank lender was struggling to make inroads with the company’s CEO and owner.

Takeaway 3 Communitybanks have seen less volatility in noninterest income, and many are still eyeing growth across the category. To remain competitive, some of the nations’ largest banks have introduced new products. Communitybanks target growth. Types of Noninterest Income. An important source of revenue.

Two sections of the 10k I scroll to is the "Business" section and the "Business Strategy" section. This, one would think, would give me a feel of the bank''s differentiation strategy, it''s perceived competitive advantage, if you will. Well don''t get too excited. I picked Texas because of their perceived independent streak.

Secular changes occur over many business cycles, tend to be slow-moving, and are more difficult to manage with business strategy. Furthermore, high federal government debt does not just lead to higher interest rates but also poses economic, national security, and social challenges. With time, these changes will only amplify.

People’s United Bank, which operates across Connecticut, southeastern New York state, Massachusetts, Vermont, Maine and New Hampshire, recently demonstrated the growing interest of communitybanks to collaborate with FinTechs to expand their product offering — just as larger national and multinational financial institutions (FIs) do.

Community bankers need to practice realistic loan pricing discipline. However, we need to understand the meaning of pricing discipline and its effect on communitybank performance. This is strong evidence that communitybanks are pricing to an arbitrary minimum credit spread in this set of loans.

. “We look forward to serving you and your communitybank in the year ahead.”. Happy New Year, community bankers! And if you haven’t done so already, I encourage you to also come up with a communitybanking resolution—one that helps you flourish as a professional. I wish I had this when I was running my bank!

We recently reviewed a loan term sheet from a nationalbank for a $13mm commercial real estate (CRE) loan. The bank offered a 25-year amortizing loan with a ten-year term and required the borrower to hedge its interest rate risk. The borrower was provided options on the type of hedge and when to execute.

Banks consistently produce under their cost of capital. For example, at present, return on equity performance is about 12% for the average communitybank. However, for the average bank, their cost of capital is between 9% and 14% depending on the bank’s equity liquidity with an average of 12.5%. Why is that?

As banks across the country mark American Housing Month in June, the ABA Banking Journal Podcast sat down with Michael Petrie, who leads the $4 billion Merchants Bancorp in Carmel, Ind. -- one of the nation's largest affordable housing lenders.

Bank Slate Convos 6. Main Street Banking: A Podcast for Community Bankers 8. Banking on Digital Growth 9. The CommunityBank Podcast 10. Ahead of the Curve: A Banker’s Podcast Ahead of the Curve: A Banker’s Podcast features insights from banking leaders and advisors across the industry.

Customers and competitors are challenging communitybanks to extend loan duration – borrowers are eager to lock fixed rates before they rise further, and many competitors are happy to oblige. But what are the optimal fixed terms for communitybanks given today’s interest rate, credit, and liquidity environment?

I was at a strategic planning retreat a few weeks back where a colleague lauded the concept of bankers getting back to plain vanilla communitybanking. Is the premise that doing "plain vanilla" banking acceptable? Valley National had an ROA in the fourth quarter of 1.08%. I hear and read this often. I doubt it.

With a competitive offering, it will be easier to attract the small business and mid-sized companies that a bank needs to fuel its core growth. The opportunity for the product is that for an average communitybank, 83% of their commercial, non-profit, and municipal customers are NOT using treasury management services.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content