This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for communitybanks. However, for communitybanks, these challenges can also present some opportunities.

It would make no sense to risk the banks capital without adequate compensation. However, some banks are inadvertently taking risk without any additional revenue. Historically, loan hedging required substantial resources for documentation, accounting, legal, marketing and operations.

In this article, we highlight some Gen AI strategy insights for communitybanks and provide tools to help bankers advance their programs. For example, in the next year, does the bank want to focus on making its employees more productive or enhancing customer experience. appeared first on SouthState Correspondent Division.

In our previous article ( here ) we analyzed the data on communitybank M&A and performance, and we concluded that there is no relationship between communitybank size and profitability, as measured by return on equity (ROE). While size isn’t correlated to profitability, operating leverage is.

This eBook explains the features of a Business Lending Platform that communitybanks should make their top priorities when evaluating any business lending software. What should you look for in a Business Lending Platform?

For more communitybanks, the latter strategy can fast-track digitization initiatives. This week’s look at the latest bank-FinTech tie-ups shows Banking-as-a-Service and other FinTech players embracing smaller regional and communitybanks to elevate small- to medium-sized business (SMBs) and corporate banking offerings.

Communitybanks can also play the fintech game. BankMobile — the digital bank, formerly a division of Customers Bancorp Inc. — was acquired by Flagship, a Florida-based communitybank, for $175 million. “We We are no longer a partner or a division of […].

While we are supporters of communitybanks using loan-level hedging, we continue to see communitybanks struggle to properly implement and successfully utilize a back-to-back swap (B2B) program. We understand why, and what communitybanks need to address to make such a program a success.

In Q2/24 the average return on assets (ROA) for communitybanks (under $10B in assets) was 1.08%, with an average ROE of 10.44%. But within the communitybanking sector, performance varied among banks significantly. The ROA for the communitybank sector is shown in the graph below. Another 16.2%

Speaker: Brian Muse-McKenney, Chief Revenue Officer & Matt Simester, Cards and Payments Expert

In this new webinar, Brian Muse-McKenney of Episode Six and Matt Simester of Payments Consultancy Limited will explore the challenges regional and communitybanks have faced in implementing tailored credit card programs with flexible payment options as a tool to attract and retain the next generation of customers.

As big banks try to win over customers with digital upgrades that resemble slick user interfaces from fintech startups, communitybanks are looking at new ways to keep pace with customer expectations. Radius Bank, a one-branch Boston-based communitybank with $1.2 billion in assets, is using […].

Our recognition as the #3 communitybank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. Yet, the banking industry is at a turning point. My goal is to convince you to approve a pilot program that will cement our position as a leader in communitybanking.

People want to be a part of something bigger than themselves, and communitybanks provide that opportunity. Communitybanking is about serving the greater good. As community continuators, we are part of something bigger than ourselves. Photo by Chris Williams.

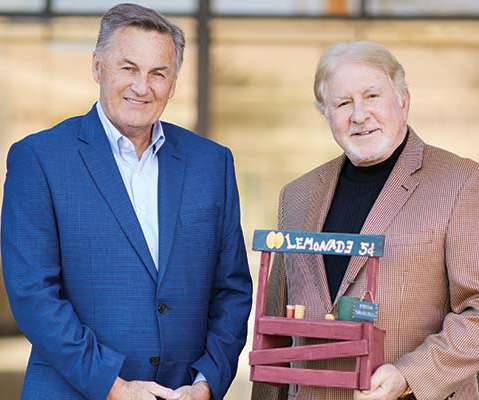

Inspired by the entrepreneurship of lemonade stands, Scottsdale CommunityBank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale CommunityBank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

That’s even more true for communitybanks, which lack the resources larger FIs have to support modernization initiatives and technology investment efforts. At the same time, the logistical challenges and competitive pressures associated with digitization remain just as pertinent for communitybanks.

Finastra, which was formed from the union of Misys and D+H, and calls itself the world’s third largest fintech company in the world, has acquired American software company Malauzai in an attempt to strengthen its foothold in the American banking market.

of digital banking customers said they switched to digital banking because of the pandemic. Source: 2021 Provident Bank survey. These days, there’s a lot to contend with as a communitybank, from changing consumer behaviors due to the pandemic to uncertainty surrounding the economy and inflation. Quick stat.

Ken Finley, president of Johnson City Bank, in downtown Johnson City with Shannon Sultemeier, executive vice president (left); and Brenda Haynes, vice president/cashier (right). Here’s how four communitybanks are thriving in this environment. These include family-owned businesses, community businesses and operating companies.

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

We asked both leaders and staffers to tell us what makes their communitybanks stand out as employers. Key CommunityBank: Leading by example. Key CommunityBank. At the heart of Key CommunityBank’s work culture is connection. Greg Dennis, Key CommunityBank. “We

.; Bank of Montana, Missoula, Mont.; CNB Bank, Berkeley Springs, W.Va.; Midwest Bank, Norfolk, Neb. In our annual workplace survey, employees of ICBA’s best communitybanks to work for told us they benefit from engaging cultures, opportunities for advancement and innovative benefits. What great resignation?

With consumer expectations seeming to evolve faster every year, communitybanks could consider partnering with a fintech to keep up with technological innovation. Those conversations, he says, centered around whether communitybanks could compete against this brash group of newcomers. Photo by Pogonici/iStock. Quick Stat.

Silicon Valley is coming to banking? That happened long ago — just ask Silicon Valley Bank, a financial institution built to serve the world’s center of innovation. SVB claims it banks a staggering two-thirds Read More. Few bankers can claim better knowledge of what the tech giants are up to. Startups, you say?

Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. WATCH Investment accounting compliance risks U.S.

Anderson bought F&M Bank in the early 1970s. Anderson celebrates 75 years in communitybanking this year. The chairman emeritus of F&M Bank offers us a glimpse of his life, his career and the lessons he’s learned along the way. Name: F&M Bank. Gibson, who owned F&M Bank in Crescent, Okla.,

Community bankers are largely positive about the future, based on the first results of a new index gauging business sentiment among the financial professionals who serve a critical role in local economies. How do you expect the regulatory burden on your bank to change over the next 12 months? Grow your loan portfolio. Learn More.

Independent Banker ’s annual CommunityBank CEO Outlook survey reveals how communitybank leaders plan to leverage today’s deposit-laden banking environment to grow this year. Janet Silveria, CommunityBank of Santa Maria. So, what’s at the top of communitybank leaders’ to-do lists?

As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Companies are borrowing more to cover operational costs but continue to pay suppliers on time, with payables remaining under 30 days.

Although the above example is a large bank, similar enforcement actions are being handed down to communitybanks. Key strategies to prevent BSA enforcement actions To prevent BSA enforcement actions, banks must prioritize proactive compliance measures. Provide timely updates in response to changes in regulations.

Communitybanks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for communitybanks. But there’s plenty communitybanks can do to meet this challenge. Here are some ideas for strengthening fraud defenses.

Most national banks scored relatively well. Communitybanks, not so much and the majority of banks can still not open an account digitally. The Problem with Todays Bank Websites Current bank websites are designed for human navigation.

As communitybanks navigate this process, there are plenty of resources available to answer questions and provide guidance. Three sources of information on FedNow As communitybanks look to take advantage of this new opportunity, they seek resources to help them navigate the journey.

To support debit card operations, a bank gets charged a myriad of transaction charges and maintenance fees from the card rails (Visa, Mastercard, Discover, etc.), and the bank’s processor (usually their core). the network (Interlink, Pulse, Shazam, etc.)

In Q2/24 the average return of asset (ROA) for communitybanks (under $10B in assets) was 1.08%. But within the communitybanking sector, performance varied among banks significantly and a large swath of banks need to improve ROA. of communitybanks reported negative ROA. Another 16.2%

We were still driving checks around, there was no online banking, and networked ATMs was the latest in bank technology. At the time, the rule of thumb for bankers was that each bank employee produced about $20,000 of operating profit per year.

Deposit costs and liquidity remain a challenge for some communitybanks as competition for core funding remains intense. The graph below compares the liquidity ratio for communitybanks (under $10B in assets) and banks over $100B in assets. Communitybanks do have a few strategies for mitigating COF pressures.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

The Clearing House’s RTP finds expansion within the communitybank arena, while abroad, the Bank of Thailand is planning its own infrastructure development to accelerate B2B payments. RTP Gains CommunityBank Traction. Bank Of Thailand Readies New Infrastructure. In the U.S.,

Executive committee members tell us what advocacy issues they’ll be focused on during their terms, while board members share their words of wisdom for up-and-coming community bankers: themselves. To sum it up, these leaders are all in and all heart for communitybanking. We are not Wall Street banks—we are communitybanks.

Last week we wrote about loan-level vs. balance sheet hedging for communitybanks and provided our loan proposal generator ( HERE ). We compared and contrasted the two strategies and sized the market for communitybanks. A communitybank may transact one or only a few balance sheet hedges over many years.

In a previous article [ here ] we discussed why communitybanks need product managers to ensure that financial products and services are effectively developed, launched, and managed to meet customers’ evolving needs and the bank’s risk and profitability goals. Not all customers are the right fit for the product.

Historically, communitybanks have relied on net interest margin (NIM) instead of fee income to drive return on equity (ROE). In contrast, larger banks have emphasized non-interest income rather than NIM to boost ROE and revenue. Larger banks have historically operated on thinner NIM but higher fee income.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content