This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For more communitybanks, the latter strategy can fast-track digitization initiatives. This week’s look at the latest bank-FinTech tie-ups shows Banking-as-a-Service and other FinTech players embracing smaller regional and communitybanks to elevate small- to medium-sized business (SMBs) and corporate banking offerings.

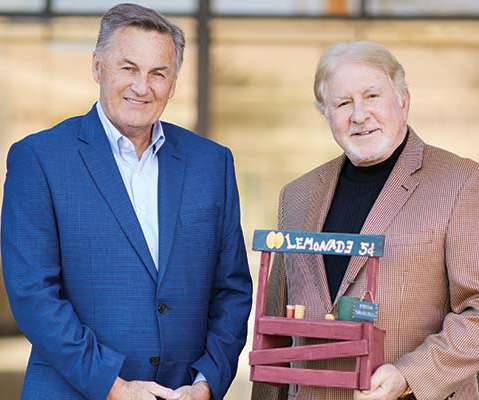

Inspired by the entrepreneurship of lemonade stands, Scottsdale CommunityBank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale CommunityBank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

Among the migrations recently completed or underway, banks are already seeing material results. Finastra announced that 27 communitybank customers are working with Finastra to upgrade their legacy core banking solutions to Fusion Phoenix. This is in addition to 15 banks which went live last year.

With mortgage rates down in the US , many homebuyers are looking locally to their communitybanks to finance their new, potentially life-changing purchase. In the spirit of the go local movement, new data from Sageworks Bank Information peeked in on 10 cities to see which communitybanks were making an impact on local mortgage lending.

retail and business banking sectors by further enabling digital transformation for communitybanks and credit unions around the U.S. Simon Paris, CEO at Finastra said in the press release, “Credit unions and communitybanks are the fabric of American financial services.

This year’s National Small Business Week , themed “SBA: Dream Big, Start Small,” will include special events in Atlanta, New York, Denver, Phoenix, San Jose, Oakland and Washington, D.C. As Federal Reserve Chair Janet Yellen said, it was small businesses that powered our recovery after the Great Recession.

Charlotte, Houston, Phoenix, New York, Austin, Denver, Orlando, Miami, and Nashville, many banks have not adjusted pricing or their credit appetite. The answer is that because operating leverage and customer relevance are now so important, banks can no longer compete on rate and the abundance of credit. Conclusion.

Can we have competitive products and delivery channels delivered with similar efficiency to the large banks? In times of great strain, opportunity rises from the ashes like a phoenix. We are closer to our communities, our customers, and our employees. We are a communitybank. I think so.

The transformation of Barwick Bank began in 2019 with a note left in Chad Bowling’s unlocked Range Rover. Bowling, a 22-year veteran of communitybanking who began his career as a teller, was ready for a change. The de novo Reunion Bank of Florida he had helped found and grow with his business partner and […].

Pima Federal Credit Union in Tucson plans to buy Republic Bank of Arizona in a cash transaction slated to close in the second half of this year. It's the ninth deal in 2024 in which a whole bank would sell itself to a credit union.

You recognize one of today’s most prominent technology dilemmas for communitybanks: It’s the great mobile divide. It’s where older, profitable customers have been slower to adopt new banking technologies that not-yet-profitable millennials pick up quickly and easily. By Paul Schaus. Millennials, who will make up half the U.S.

These in-depth and timely professional development programs are designed exclusively for community bankers and led by nationally recognized industry experts who know the issues communitybanks grapple with. Each certification course is designed to prepare bank professionals to handle essential tasks and responsibilities.

Outside of IBS, however, FIS is struggling to establish an identity with its core banking products, including Horizon, BancPac and Bankway. If you’re a $2 billion bank that wants an outsourced core, everyone knows FIS will bring IBS. But what if you’re a $500 million communitybank that wants to operate core in-house?

Ladies & Gentlemen, What you are about to hear is based on a true story of two mid-size banks, but names, numbers and key aspects of the story have been changed to protect the innocent. This is a tale of growth at Warm Pulse Bank and Cold Fish Bank. 4 Stages of LinkedIn at Mid-size Banks. Extensive branch networks.

Now, a major portion of the regional and communitybank industry must handicap whether FIS can execute on an ambitious strategy with a rapid-fire development road map after believing in a completely different channels story from the company for the past several years.

Not the financial industry’s “Troublemakers ” – those regional and communitybanks, credit unions and supporting fintech entrepreneurs who continue to engage customers and communities and find niches that keep the grassroots of our country’s financial system alive and kicking.

JHA promised several solutions for retail front-end branch and loan systems and a NetTeller/goDough tandem digital banking solution. D+H (and before, Harland) promised integrated loan and core systems and specialized credit union functionality in the Phoenix EFE core. The Phoenix EFE core has a Microsoft-based architecture with legs.

JHA promised several solutions for retail front-end branch and loan systems and a NetTeller/goDough tandem digital banking solution. D&H (and before, Harland) promised integrated loan and core systems and specialized credit union functionality in the Phoenix EFE core. Either double down on U.S.

. ————————————————————————— The ‘En Vogue’ Trend of the Year – Credit unions buying communitybanks. Accounts that maintain an average balance of at least $10,000 get paid higher rates.

Communitybank marketing resources. With market opportunity heating up and big bank and big credit union competitors hitting hard, too many communitybanks lack marketing resources … or they have 2X more spending in sponsorships than the campaigns, analytics and digital sales improvements that actually bring in new business.

Here's how communitybanks and credit unions can generate more home equity lending, along with a gallery of marketing examples. The post Tips to Help Financial Marketers Grab More Home Equity Lending Business appeared first on The Financial Brand.

Hats off to Thomas Shara at Lakeland and Tony Labozzetta of Provident for architecting the new $25 billion super-communitybank in New Jersey. The Smarter Bank Innovation Award. Goes to Lincoln Savings Bank – Iowa (LSBX). Provident Financial Services, Inc. merges with Lakeland Bancorp. talent market. Goes to CSI.

Nothing seems to put a bounce in a banker’s step more than a tax break and regulatory relief, and this bountiful energy was radiating at Bank Director’s annual “mecca” for bank M&A in Phoenix last week – Acquire or be Acquired. For those in the know – simply AOBA.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content