This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Communitybanks (under $10B in assets) serve a key role for borrowers, local communities, and the broader US economy. Communitybanks are better positioned than many other creditors to follow and adapt to local economies, industries and trends, thereby, being better stewards of capital. The number of U.S.

Communitybanks’ use of swaps (banks’ primary tool to hedge interest rate risk on loans) has increased substantially over the last ten years. Meanwhile, communitybanks face net interest margin (NIM) and fee income pressure. Only 304 banks (or 6.7% of the total) used swaps directly.

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. banking regulations.

An inverted yield curve, continued bank failures, and the desire to managerisk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

An inverted yield curve, continued bank failures, and the desire to managerisk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

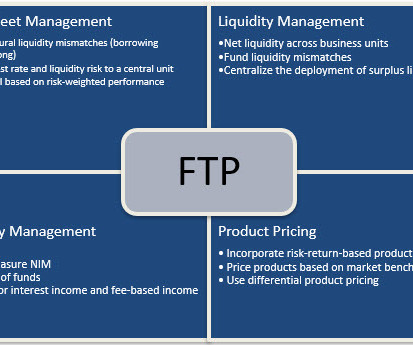

All domestic systemically important banking organizations and most large regionalbanks engage in some form of FTP practices and building blocks. However, over the years, there has been considerable debate at communitybanks on how to implement the principles of FTP to various balance sheet accounts like loans and deposits.

A recent data report culled from Sageworks Bank Information , a web-based data platform that includes financial and regulatory information on every U.S. bank and credit union, named the “ Top 15 communitybanks by commercial loan growth.” Blog Bank' From that subset of all U.S.

Last week we wrote about loan-level vs. balance sheet hedging for communitybanks and provided our loan proposal generator ( HERE ). We compared and contrasted the two strategies and sized the market for communitybanks. A communitybank may transact one or only a few balance sheet hedges over many years.

The MOU dictates that the banks will train FinTech startups with an eye on cross-border transactions. Deputy Managing Director of MAS Jacqueline Loh said the relationship demonstrates a FinTech that may extend to other countries in the ASEAN region.

Equiniti Eyes APIs for RiskManagement. Equiniti Group recently revealed its adoption of Codat’s accounting integration API for its Equiniti Riskfactor solution, a tie-up that will see Equiniti’s riskmanagement operations embrace API technology to promote automatic data sharing from small businesses.

Some stakeholders are advocating for a focus on affordable housing, community development, and supporting underserved communities. Capital rules are also being reassessed for members and the FHLB themselves in an effort to ensure greater financial stability and riskmanagement.

Nonetheless, with the recent collapse of sizeable regionalbanks, regulators, investors, analysts, accountants, and bankers are now scrutinizing the fair value of banks’ securities and loan portfolios. This development should strongly motivate communitybanks to consider the benefits of loan-level hedging.

In its biannual report on supervision and regulation, the Federal Reserve Board noted an uptick in governance issues with large banks. Regional and communitybanks, meanwhile, were plagued by IT problems and riskmanagement struggles.

Takeaway 2 Communitybanks may face challenges seeking reimbursement for breach of warranty claims filed with other FIs. Takeaway 3 Banks and credit unions should leverage new tools to improve check fraud prevention that can ease the burden on their staff and safeguard customers.

Communitybanks are expanding their loan portfolios to include more small business loans, according to the most recent CommunityBank Performance report by the FDIC. Loans across categories increased, with commercial and industrial loans growing at the fastest rate, roughly 5.3 percent over the 3rd quarter of 2013.

This week’s look at the latest in bank-FinTech collaborations and open banking initiatives finds a focus on small business lending: In the U.K., Funding Options struck a data-sharing agreement with 20 alternative lenders to make SMB loan applications more efficient, while in the U.S.,

Community bankers need to practice realistic loan pricing discipline. However, we need to understand the meaning of pricing discipline and its effect on communitybank performance. This is strong evidence that communitybanks are pricing to an arbitrary minimum credit spread in this set of loans.

RegionsBank waives fees and offers other relief while American Express donates to the American Red Cross CommunityBanking Feature3 Feature RiskManagement Branch Technology/ATMs Fee Income.

According to the OCC, institutions that have incorporated stress testing into their planning typically demonstrate an ability to withstand negative market developments more effectively than other financial institutions as a result of these beneficial riskmanagement practices.

Charlotte, Houston, Phoenix, New York, Austin, Denver, Orlando, Miami, and Nashville, many banks have not adjusted pricing or their credit appetite. For 2023, banks need to prioritize interest rate riskmanagement and credit accuracy as a top priority. of the banking market, according to Statista Research.

With wire fraud on the rise, communitybanks have to step up precautions to protect themselves and their customers. They have the money and, in theory, they are vulnerable,” adds Terri Sands, director of payments and fraud prevention for State Bank & Trust in Atlanta, a $3.3 billion-asset communitybank.

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. FTP may have prevented the demise of First Republic Bank.

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. FTP may have prevented the demise of First Republic Bank.

Bank executives that measure and manage the balance sheet based on the fair value of assets and liabilities invariable will change risk behavior, compensation structures, and capital allocation for the long-term benefit of shareholders. FTP may have prevented the demise of First Republic Bank.

Banks are critical financing partners for growing enterprises. Eight in 10 business owners report that a major, regional or communitybank is their main financing partner for capital. After all, most of the nearly 29 million businesses in the U.S. are small businesses – a trend unlikely to shift much in the coming years.

Welcome to the Crescent City, where the largest educational gathering of community bankers convenes this month. It’s CommunityBanking LIVE 2016 in New Orleans. State/Regional Partners Reception*. State/Regional Affiliate Associations & Exhibitor Receptions*. Monday, March 7. Concurrent Workshops.

While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate riskmanagement. While interest rate risk caused the most significant impact on value, several other factors contributed to the terminality of each bank that was closed.

This suite of systems can take banks from chaotic and fragmented operations to a smart, scaled future. A striking dynamic has occurred among regional and communitybanks over the past 10 years: their assets have grown much faster than their maturity. A GRC system is more than a pure audit system.

In our region, the Philly Fed indices of business activity all turned negative in December, but, hey, higher rates will help, right? Dorothy has been with Penn CommunityBank and its predecessor since November, 2004. Housing is volatile, especially at this time of year. Why is the Fed trying to slow down GDP growth of 1%?

Lenders are scrambling to pause ranchers’ loan payments as meat processing plant shutdowns during the pandemic threaten $25 billion in losses for the livestock industry.

Not the financial industry’s “Troublemakers ” – those regional and communitybanks, credit unions and supporting fintech entrepreneurs who continue to engage customers and communities and find niches that keep the grassroots of our country’s financial system alive and kicking. billion bank in the Mid-Atlantic region.

Pillar #2: Leaders Transcend Daily Hustle to Build New Systems Most regional and communitybanks grew up executing the fundamentals with sheer hustle and hard work. riskmanagement and operations, trust becomes the fuel to move quickly across organizational lines, and trust becomes the personal currency of leaders.

Stratyfy: Raised $12M, decision intelligence technology gaining traction, particularly in riskmanagement. Spring 2022 (San Francisco): Array: Credit and identity management platform, seeing increased adoption due to robust features and user-friendly interface.

. ————————————————————————— The ‘En Vogue’ Trend of the Year – Credit unions buying communitybanks. Might be time to. Well done, sir! Congrats to the DNA team for this huge win.

Cornerstone Advisors has been a broken record telling the story of a communitybanking industry that’s falling behind in online and mobile capabilities. Our long novels about slowly losing ground to the mega banks just became an audio book to be played on high speed while walking between the kitchen and home office to refill on coffee.

ISMs and regional Fed surveys have been mostly negative for months on end. DLJ 03/15/24 Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis. GDP shows up as weak every other quarter.

Bank Acquisition of the Year - BB&T Corp. Nice communitybank culture fit between the two as well. Bank Merger of the Year – California United Bank and 1 st Enterprise Bank in Los Angeles. RiskManagement. ??? takes Susquehanna Bancshares Inc. Performance Solutions. System Selection.

Bank Merger of the Year Although this technically was an acquisition , the $25 billion Atlantic Union Bankshares combining with $14.4 billion Sandy Springs Bancorp builds a powerhouse in the Mid-Atlantic region. GonzoBanker of the Year (RegionalBank) goes to Kevin Blair of Synovus Financial Corp.

The merger of equals activity in 2021 was sky high, primarily because banks with pinched margins from low rates worked to grabbed scale. From nowhere, sizable regional players are being created. Bank Merger of the Year. Performance and multiples continue to be solid, outperforming most regionalbanks. You tell us.

Our regional economy, covered by the Philadelphia Federal Reserve’s Third District, is doing well into the fourth quarter. Dorothy Jaworski has worked at large and small banks for over 30 years; much of that time has been spent in investment portfolio management, riskmanagement, and financial analysis.

The recent March, 2018 report for our Philadelphia Region was overall quite positive; the words “modest” or “moderately” were used 16 times on two pages. Dorothy has been with Penn CommunityBank and its predecessor since November, 2004. The Federal Reserve Beige Book is released in advance of the Federal Reserve meetings.

Mergerama Region of the Year – The Midwest: Huntington-First Merit, Chemical-Talmer, Old National-Anchor … the list goes on. Or the need to take market share in a slowest growth region? Acquisition of the Year – Guaranty Bank and Trust Company in Colorado for its acquisition of Home State Bank. Is it in the water?

Mergerama Region of the Year – The Midwest: Huntington-First Merit, Chemical-Talmer, Old National-Anchor … the list goes on. Or the need to take market share in a slowest growth region? Acquisition of the Year – Guaranty Bank and Trust Company in Colorado for its acquisition of Home State Bank. Is it in the water?

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content