This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It would make no sense to risk the banks capital without adequate compensation. However, some banks are inadvertently taking risk without any additional revenue. Historically, loan hedging required substantial resources for documentation, accounting, legal, marketing and operations.

In this article, we highlight some Gen AI strategy insights for communitybanks and provide tools to help bankers advance their programs. For example, in the next year, does the bank want to focus on making its employees more productive or enhancing customer experience. appeared first on SouthState Correspondent Division.

The ABA Foundation offers resources for bank customers and employees on how to recover financially from disasters and on how to avoid scammers who prey on disaster victims and people seeking to donate to recovery efforts.

Our analysis shows that an average communitybank can expect $9.7mm NPV of income (about 1% ROA) on a $100mm loan portfolio when the average loan life is seven years, versus only $5mm NPV of income (about 0.50% ROA) on the same portfolio where the average loan life is 2.3 years (both portfolios measured over a ten-year life).

Treasury teams at communitybanks face an ongoing challenge of delivering frictionless customer experiences as they support treasury products – especially RDC. This infographic focuses on the efficiencies communitybanks gain when partnering with a proven managed services provider. The result?

We measured prepayment speeds, loan size, loan term, fee income, loan yield, credit performance, and return on equity (ROE) of hedged loans and compared this performance to communitybank industry averages. We also looked at how these hedged loans track communitybanks’ funding costs.

If you are a domestic communitybank, you can access the Health Prediction HERE on our Correspondent Bank “Resource Center.” ” If you do not already have a log in, you can register at the bottom of the page to gain free access to this application and several other resources.

While we are supporters of communitybanks using loan-level hedging, we continue to see communitybanks struggle to properly implement and successfully utilize a back-to-back swap (B2B) program. We understand why, and what communitybanks need to address to make such a program a success.

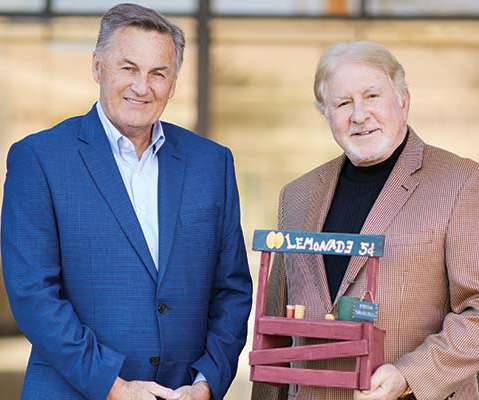

Inspired by the entrepreneurship of lemonade stands, Scottsdale CommunityBank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale CommunityBank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

Communitybanks are looking for ways to leverage their technology infrastructure to drive productivity and growth. However, the sheer volume of technology devices, capital constraints, and lack of skilled resources stand in the way.

As communitybanks navigate this process, there are plenty of resources available to answer questions and provide guidance. Three sources of information on FedNow As communitybanks look to take advantage of this new opportunity, they seek resources to help them navigate the journey.

While the final guidance clearly applies to larger financial institutions, communitybanks should still take note. ” The section further details this would only occur under extraordinary circumstances, but communitybanks should be aware of the new framework and even consider applying the guidelines as a proactive, best practice.

Preparing for 2023 While communitybanks have until 2023 until they must comply with CECL, there is likely less time than expected. . While communitybanks have until 2023 until they must comply with CECL, there is likely less time than expected. 2023 CECL Deadline? Steps to Take This Year WATCH Webinar.

This year’s winners: Left: Central Valley CommunityBank, People’s Choice Award; Middle: Kennebec Savings Bank, Exceptional CommunityBank Service Award; Right: Cross River Bank, Emerging Service Program Award. Exceptional CommunityBank Service Award. Kennebec Savings Bank.

To that end, news came earlier this week in the United States that a dozen community and regional banks have formed a group aimed at exploring the opportunities amid FinTech offerings. The group, to be known as Alloy Labs Alliance, according to a press release , is being managed by FinTech Forge.

That’s even more true for communitybanks, which lack the resources larger FIs have to support modernization initiatives and technology investment efforts. At the same time, the logistical challenges and competitive pressures associated with digitization remain just as pertinent for communitybanks.

Takeaway 2 Abrigo advisory expert Susan Sharbel offers insights into where your bank should focus its resources to manage interest rate risk, Takeaway 3 Practical steps for preparing your ALM program for rate changes include updating and validating risk models regularly, conducting tests, and reviewing portfolios.

Here’s how four communitybanks are thriving in this environment. There’s a lot of energy in the southern half of Texas, and it’s not just the resources that power our homes and cars. We spoke with four communitybanks in the southern half of Texas to learn how they are serving this buzzing region.

However, there may be an opportunity to get more contactless cards into the hands of consumers — an opportunity that involves communitybanks and is backed by financial incentives. ICBA Bancard’s 1,600 communitybank customers have issued more than 7.3 ICBA Bancard’s 1,600 communitybank customers have issued more than 7.3

With consumer expectations seeming to evolve faster every year, communitybanks could consider partnering with a fintech to keep up with technological innovation. Those conversations, he says, centered around whether communitybanks could compete against this brash group of newcomers. Photo by Pogonici/iStock. Quick Stat.

According to the Sageworks 2015 Bank and Credit Union Exam Survey , more than 40 percent of the 180 responding institutions had already begun stress testing, and it was recommended to 30 percent that they begin stress testing or expand current stress test practices. Understand your portfolio and its risk factors. Ensure proper data.

This article is the first in a two-part series on top concerns and growth strategies of communitybanks. These are all phrases that resonate with community bankers. Data from Bank Director’s 2014 Growth Strategy Survey in August confirms that these are bankers’ greatest concerns. Regulatory compliance.

But there are ways communitybanks can help mortgage-seekers get on the property ladder. Burmis, senior vice president and retail lending manager at $450 million-asset Chelsea State Bank in Chelsea, Mich. So how can communitybanks help? Providing educational resources. By Beth Mattson-Teig.

.; Bank of Montana, Missoula, Mont.; CNB Bank, Berkeley Springs, W.Va.; Midwest Bank, Norfolk, Neb. In our annual workplace survey, employees of ICBA’s best communitybanks to work for told us they benefit from engaging cultures, opportunities for advancement and innovative benefits. What great resignation?

We asked both leaders and staffers to tell us what makes their communitybanks stand out as employers. Key CommunityBank: Leading by example. Key CommunityBank. At the heart of Key CommunityBank’s work culture is connection. Greg Dennis, Key CommunityBank. “We

Communitybanks are pushing for a stronger role with their small business (SMB) customers. However, through an embrace of FinTech collaboration and industry consolidation, communitybanks appear poised to further dispel assumptions of a lack of digitization. A Consolidating Industry. Strengthening SMB Ties.

At a communitybank with limited staff and resources, tech transformation is all about setting priorities. The post Podcast: Step-by-Step IT Transformation at a CommunityBank appeared first on ABA Banking Journal.

Connect with an expert Common fraud schemes Check fraud Check fraud is one of the most concerning fraud trends for communitybanks in 2025. Regardless of the current budget, regulators will expect adequate technological and human resources to protect the institution's safety and soundness.

Communitybanks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for communitybanks. But there’s plenty communitybanks can do to meet this challenge. Here are some ideas for strengthening fraud defenses.

MOXY bank , preparing to be one of the first new communitybanks to launch in the U.S. in decades, has announced that it is working with technology solutions company NYMBUS to integrate its core digital banking and payment services.

Communitybanks own an enviable amount of data, but not all are leveraging it to its fullest extent. By Mindy Charski People share important data about themselves with their communitybank in myriad ways. Data about existing customers can even help communitybanks improve their efforts to find new customers.

Nuts-and-bolts strategies to help banks respond to the coronavirus pandemic . The post Coronavirus Response: Common Practices for CommunityBanks appeared first on ABA Banking Journal.

Not many bank CEOs can say their first bank job was. The post The Path Less Taken to the CommunityBank C-Suite appeared first on ABA Banking Journal. For those who can, they say it brings a unique perspective on leadership to the industry.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more communitybanks to adopt a loan hedge program. Communitybanks do this profitably by turning transactional accounts into relationships.

When Gilda Nogueira's family immigrated to the United States, East Cambridge Savings Bank in Cambridge, Massachusetts, helped them land on their feet and begin their new life in America. Today, Nogueira pays this opportunity forward through communitybanking as president and CEO of ECSB.

The Clearing House’s RTP finds expansion within the communitybank arena, while abroad, the Bank of Thailand is planning its own infrastructure development to accelerate B2B payments. RTP Gains CommunityBank Traction. In the U.S., And when it comes to legacy rails, the U.S.

Although the above example is a large bank, similar enforcement actions are being handed down to communitybanks. Key strategies to prevent BSA enforcement actions To prevent BSA enforcement actions, banks must prioritize proactive compliance measures. financial system.

Communitybanks pride themselves on superior customer service. Approximately 90% of all communitybanks believe that they provide an above-average level of customer service (of course, the math cannot work that way, as half of all banks should be providing a below-average level of customer service).

Digital lending is becoming an important business even for smaller communitybanks. Larger banks, which have the resources to build their own technology or buy a fintech provider (KeyBank acquired Bolstr; JPMorgan Chase acquired WePay).

Many banks pride themselves on superior customer service, and approximately 90% of all communitybanks believe that they provide an above-average level of customer service (the math cannot work that way). In the big picture, providing superior service across the entire bank customer base is counterproductive.

As an early-career CPA, Carissa Rodeheaver began her communitybanking career as a trust administrator nearly three decades ago. Now, she's at the same bank, as chairman, president and CEO of Oakland, Maryland-based First United Bank and Trust.

Communitybanks are independent institutions fueled by the needs of their individual communities, so what constitutes innovation will look and feel different for every bank. I’ll be at the annual meeting of the California CommunityBanking Network. Photo by Robert Severi. Where I’ll Be.

With banks, their customers and their employees facing unprecedented challenges associated with the 2019 novel coronavirus pandemic, ABA today published a suite of new resources for bankers to help them navigate this ever-changing situation.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content