This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Generative AI and the new loan review process The evolution of banking and riskmanagement over the past few decades has been nothing short of remarkable. Generative AI in credit riskmanagement is the latest step forward , offering a transformative approach to loan review. Data security is also a major concern.

Our intelligent fraud detection software and riskmanagement tools help fraud professionals in their fight against financial crime. Making a difference in communitiesBanking is more than just numbers and transactions. financial institutions managerisk and drive growth in a rapidly changing world.

Our analysis shows that an average communitybank can expect $9.7mm NPV of income (about 1% ROA) on a $100mm loan portfolio when the average loan life is seven years, versus only $5mm NPV of income (about 0.50% ROA) on the same portfolio where the average loan life is 2.3 years (both portfolios measured over a ten-year life).

That fact makes the bank’s deposits less sticky and subject to outflow at any sign of insolvency. Equally important is the bank’s securities duration, as shown in the graph below. Approximately 56% of the bank’s securities had repricing greater than 15 years. at the end of 2022, with $2.4B

Our recognition as the #3 communitybank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. My goal is to convince you to approve a pilot program that will cement our position as a leader in communitybanking. What is Microsoft Copilot?

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny.

How can community financial institutions thrive in 2021? Communitybanks provide unique and important banking services for their customers, but they also face significant obstacles. Takeaway 1 Communitybanks play an important role in the economy and their communities, but they face significant obstacles.

Connect with an expert Common fraud schemes Check fraud Check fraud is one of the most concerning fraud trends for communitybanks in 2025. As mentioned above, a strong fraud prevention plan includes proactive customer outreach, security alerts, and educational resources on phishing scams, identity theft, and safe banking practices.

Communitybanks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for communitybanks. But there’s plenty communitybanks can do to meet this challenge. Here are some ideas for strengthening fraud defenses.

Wells Fargo, weeks after it was hit with a rare enforcement action from the Federal Reserve, is overhauling its riskmanagement processes and announced internally that four top riskmanagement executives would be retiring. All are retiring in April, May or June.

"With so many BSA/AML enforcement actions, it is clear that the regulatory environment is tightening up its expectations and is actively pursuing action when needed," said Abrigo Senior RiskManagement Consultant Elissa Brewer. A formal requirement for institutions to develop and update risk assessments is among the expected changes.

Furthermore, high federal government debt does not just lead to higher interest rates but also poses economic, national security, and social challenges. Federal Debt – Impact Banking The path of the federal debt is already changing economic and public dynamics. With time, these changes will only amplify.

Nonetheless, with the recent collapse of sizeable regional banks, regulators, investors, analysts, accountants, and bankers are now scrutinizing the fair value of banks’ securities and loan portfolios. This development should strongly motivate communitybanks to consider the benefits of loan-level hedging.

However, we would like to identify one important macroeconomic variable that will affect the banking industry regardless of the makeup of the legislative and executive branches of the US government. Regardless of who wins, our national debt will continue to increase, and communitybanks should be prepared for its consequences.

In banking, those numbers are markedly different. The average communitybank has thousands of customers, and the vast majority (close to 90%) earn zero or negative ROE. At an average bank, the top 10% of customers generate the entire profit for the bank. Profitability continues to grow over time.

The OCC, FDIC, and Federal Reserve Board have issued a guide that is intended to assist communitybanks in conducting due diligence when considering relationships with financial technology (fintech) companies (Guide). Banks are instructed to reference relevant guidance from the agencies that is listed in a footnote.

The root cause of Silicon Valley Bank’s (SVB) failure is poor riskmanagement – plain and simple. Bankers need to understand and manage their business on the fair value of assets and liabilities instead of managing their business on net interest margin and the amortized historical cost of assets and liabilities.

A recent Wall Street Journal article by Victoria McGrane and Jon Hilsenrath highlighted how the nation’s regulators are increasingly questioning and turning their focus toward bank boards. These smaller banks have also seen new, and more frequent, attention from regulators. How complex is the bank’s operating model?

Rising funding costs and decreasing liquidity at communitybanks are causing managers to change pricing methodology for new credits. We estimate that 25% to 50% of communitybanks have a policy requiring minimum yield or credit spreads for new commercial loans.

Banking reports to inform riskmanagement and strategy These reports on capital, growth, and liquidity help financial institutions spot warning signs. They help manage and shape strategy in volatile economic and industry conditions. the CommunityBank Leverage Ratio (CBLR) and the minimum Tier 1 leverage ratio).

“A lot of people have this notion that it will never happen to my business or my bank, because it’s too small,” says Linda Comerford, assistant vice president of incident response and cyber services at AmTrust Financial Services Inc. The bank was only able to get fully up and running after it paid a negotiated ransom.”.

Currencycloud is connecting regional banks to advanced FX and global payments technologies, while the firm’s founder, Nigel Verdon, is also targeting Banking-as-a-Service with his new startup, Railsbank. Catch up on the most recent efforts to unlock, share and integrate bank data below.

Community bankers need to practice realistic loan pricing discipline. However, we need to understand the meaning of pricing discipline and its effect on communitybank performance. This is strong evidence that communitybanks are pricing to an arbitrary minimum credit spread in this set of loans.

As a share of their total assets, communitybanks have more business loans below $1 million than larger banks, according to the St. When a small business owner can upload supporting documents securely anytime from anywhere, the bank or credit union spends less time chasing documents.

Last year, communitybank loan producers were faced with both record-low interest rates and a glut of deposits. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent riskmanagement practices. Red River State Bank.

With the recession fading into the more distant past, banks – in particular, communitybanks – have seen several years of loan growth. Banks, according to Comptroller of the Currency Thomas Curry, are starting to reach for additional growth by lending to less creditworthy borrowers, a move that increases risk to the institution.

The Clearing House (TCH), which operates the RTP Business Committee, has added four seats to the committee to incorporate communitybank and credit union representation, and also released a set of business principles to outline the RTP’s work. The RTP network was built for financial institutions of all sizes throughout the U.S.

CRE loan growth at communitybanks has been outpacing noncommunity banks, both in the quarter and over the last year, according to the FDIC’s latest Quarterly Banking Profile. . “CRE Heading into 2020, banks seem to be continuing to respond to risk concerns.

According to a statistic released as part of the ICBA 2014 Top 50 CommunityBank Leaders in Social Media, nearly 2,500 banks have a Facebook or Twitter presence, and the numbers continue to exponentially grow. It is apparent everywhere you turn that social media is one of the hottest new communications tools in our society.

As a share of their total assets, communitybanks have more business loans below $1 million than larger banks, according to numbers from the St. When a small business owner can upload supporting documents securely anytime from anywhere, the bank or credit union spends less time chasing documents.

Every year, it is estimated elder adults are exploited for up to $36 billion Compliance RiskManagement Duties Management Feature Feature3 Customers Compliance/Regulatory Cyberfraud/ID Theft Consumer Compliance CommunityBankingSecurity.

During the pandemic, many communitybanks needed to change how they operated. For this and other reasons, now is a good time to review and refresh articles, bylaws and committee charters to ensure resilience and bolster riskmanagement. But if they see it as a riskmanagement tool, it’s a game changer.

But as the prevalence of security breaches grows, so do the opportunities for communitybanks to position themselves as guardians of their customers’ personal data through compliance, technology and relationship building. Data privacy and security is a hot topic and is only getting hotter. By Katie Kuehner-Hebert.

The board noted it has already taken actions to strengthen oversight and has held those responsible for the fake bank accounts scandal accountable, including John Stumpf, CEO , and Mary Mack, head of communitybanking.

Saving money by conducting inside riskmanagement and compliance reviews. As a group, communitybanks spend substantial funds hiring outside consultants to help with various management functions, and a substantial share of dollars are spent to help oversee their riskmanagement and compliance activities.

While the pace of bank regulatory changes has diminished from a few years ago, several issues will either become effective or likely develop in 2023. Communitybanks must continue to stay focused on regulatory discussions and remain nimble to respond to proposals and address requirements quickly and accurately. Evolving risks.

While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate riskmanagement. While interest rate risk caused the most significant impact on value, several other factors contributed to the terminality of each bank that was closed.

That’s where a bank’s enhanced due diligence protocols come into place. McShirley pointed out that linked2pay offers a bank platform with a built-in registration for merchants that helps banks review the compliance, security and fraud aspects to help institutions construct a profile of potential new clients and better understand their risks.

This week’s look at the latest open banking and bank-FinTech collaborative initiatives reveals financial services firms continue to focus on elevated functionality, with data security seemingly more of a background priority. Amex Joins Revolut’s Open Banking Platform. Arvest Bank Taps Finzly Platform.

Communitybanks cannot afford to ignore the staggering pace of lending adoption by both individuals and businesses using digital-only platforms from various nonbank technology-based specialty lending firms. But communitybanks should not be without hope, nor should they underestimate the significance of customer relationships.

Regardless of the name, nonbank technology firms are wedging themselves between communitybanks and their customers by offering a slew of traditional and nontraditional banking products. This is why ICBA and communitybanks must continue to push consistent regulation of bank and nonbank financial service providers.

Growing loans, earnings are banks' top challenges in 2021. The top banking challenges in 2021 are growing loans and earnings, according to Independent Banker’s recent 2021 CommunityBank CEO Outlook survey. Lending & Credit Risk. Credit RiskManagement. Lending & Credit Risk.

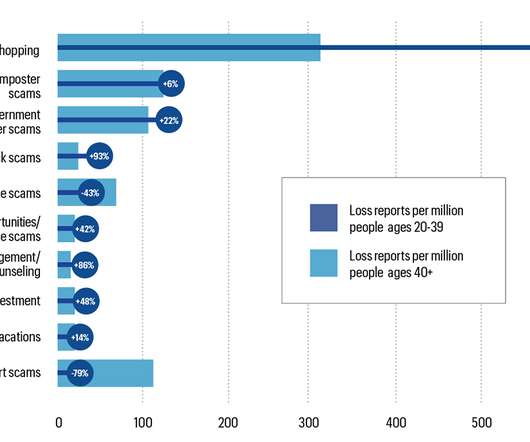

By identifying the preferred banking and spending habits of different generations, scammers can tailor how they reach their targets. We look at communitybanks’ options for fighting this type of crime. By Katie Kuehner-Hebert. The only thing the criminal wants is for the scheme to succeed.”. Rehman Khan, Travelers.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content