This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for communitybanks. However, for communitybanks, these challenges can also present some opportunities.

However, not all have a specific Gen AI strategy, and they should make their journey more efficient. A quality Gen AI strategy aligns an organizations objectives, its use cases, and the delivery mechanism and metrics that measure business value. Few communitybanks have the resources to accomplish both, and both are sizeable efforts.

It would make no sense to risk the banks capital without adequate compensation. However, some banks are inadvertently taking risk without any additional revenue. But at SouthState Bank, we use a much simpler solution. However, that strategy is especially painful for banks when the yield curve is flat.

In our previous article ( here ) we analyzed the data on communitybank M&A and performance, and we concluded that there is no relationship between communitybank size and profitability, as measured by return on equity (ROE). The key insight is to understand how growth translates into bank efficiency.

Treasury teams at communitybanks face an ongoing challenge of delivering frictionless customer experiences as they support treasury products – especially RDC. This infographic focuses on the efficiencies communitybanks gain when partnering with a proven managed services provider. Download the infographic today!

You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective risk management and compliance." WATCH Takeaway 1 Many financial institutions are questioning where rates are headed and how to structure their ALM strategies accordingly.

Our analysis shows that an average communitybank can expect $9.7mm NPV of income (about 1% ROA) on a $100mm loan portfolio when the average loan life is seven years, versus only $5mm NPV of income (about 0.50% ROA) on the same portfolio where the average loan life is 2.3 years (both portfolios measured over a ten-year life).

We work with hundreds of communitybanks across the country that utilize forward rate locks to decrease risk, increase fee income, and stave off competition from national and regional banks. A forward rate lock allows lenders to deliver a known loan rate on future borrower financing without interest rate risk for the bank.

For more communitybanks, the latter strategy can fast-track digitization initiatives. This week’s look at the latest bank-FinTech tie-ups shows Banking-as-a-Service and other FinTech players embracing smaller regional and communitybanks to elevate small- to medium-sized business (SMBs) and corporate banking offerings.

Communitybanks are looking for ways to leverage their technology infrastructure to drive productivity and growth. This strategy brief explores how a managed device services partner can help bridge this resource gap.

Banks & credit unions recognize the importance of new deposits After years of consistent deposit growth, financial institutions have faced a shift recently, with deposits declining since 2022. Investing in digital solutions not only improves the customer experience but also positions communitybanks as forward-thinking financial partners.

In Q2/24 the average return on assets (ROA) for communitybanks (under $10B in assets) was 1.08%, with an average ROE of 10.44%. But within the communitybanking sector, performance varied among banks significantly. The ROA for the communitybank sector is shown in the graph below. Another 16.2%

Over the last 15 years, an ever greater percentage of communitybanks have embraced some form of interest rate hedging. Approximately 1,000 banks in the country use some form of hedging products to manage risk, generate fee income, or provide product offerings demanded by their customers. Loan-level Vs. Balance Sheet Hedging.

Over the last 15 years, an ever greater percentage of communitybanks have embraced some form of interest rate hedging. Approximately 1,000 banks in the country use some form of hedging products to manage risk, generate fee income, or provide product offerings demanded by their customers. Loan-level Vs. Balance Sheet Hedging.

Innovation has always been important for communitybanks, but the driving force of digitization over the last decade has greatly sped up the pace, said Kevin Tweddle, chief innovation officer for the Independent Community Bankers of America ( ICBA ). Communitybanking is no exception. Leveling the Playing Field.

Therefore, the quarterly profile and Chairman Martin Gurenberg’s commentary on the industry are skewed by the performance of larger banks. In this article, we analyze the underlying data for communitybanks and focus on the Chairman’s view of the future of bank performance.

Communitybank cost of funds is jumping up. As shown in the graph below, the net interest margin (NIM) for communitybanks declined 22bps in Q1’23. The question is – what will happen to communitybank’s cost of funds from here? Increase product engagement and duration.

Communitybanks’ use of swaps (banks’ primary tool to hedge interest rate risk on loans) has increased substantially over the last ten years. Meanwhile, communitybanks face net interest margin (NIM) and fee income pressure. Only 304 banks (or 6.7% of the total) used swaps directly.

The current policy directions from the new administration are largely inflationary, and communitybanks should be paying attention and consider a loan-level hedge strategy. Many banks that survived the rapid interest rate hikes still struggled with net interest margin (NIM) compression caused by fixed-rate loans and securities.

Preparing for 2023 While communitybanks have until 2023 until they must comply with CECL, there is likely less time than expected. . While communitybanks have until 2023 until they must comply with CECL, there is likely less time than expected. 2023 CECL Deadline? Steps to Take This Year WATCH Webinar.

How can community financial institutions thrive in 2021? Communitybanks provide unique and important banking services for their customers, but they also face significant obstacles. Takeaway 1 Communitybanks play an important role in the economy and their communities, but they face significant obstacles.

For Brice Luetkemeyer, president and CEO of Bank of St. Elizabeth, a Missouri-based communitybank with $150 million in assets, investing in a core banking startup is critical for its future. Together with a group of other communitybanks, Bank of St. Elizabeth recently invested in Neocova, a St.

BANKSTRATEGY One item that should be on every bank’s strategic horizon is how to adapt to the changing face of payments. In this article, we highlight the newest data from the Fed and what it might mean for every communitybank.

Communitybanks are independent institutions fueled by the needs of their individual communities, so what constitutes innovation will look and feel different for every bank. That’s why ICBA has focused so intently on innovation strategy over the past few years. Photo by Robert Severi. Where I’ll Be.

A profitability strategy has a lot to factor in given today’s uncertain market. Here’s what community bankers need to know when planning their budgets for the next year. of digital banking customers said they switched to digital banking because of the pandemic. Source: 2021 Provident Bank survey. Quick stat.

We concluded that the market does not adequately compensate banks for credit and interest rate risks. Top-performing communitybanks deploy relationship banking. We define relationship banking as a model focused on a consultative banking approach. uses at our bank.

Alloy’s Julieann Thurlow, CEO of Reading Cooperative Bank, said, “Communitybanks play a special role in the lives of our customers, but we don’t have the same IT and innovation budgets as the big banks to capitalize on that relationship.” Here In The States.

Independent Banker’s annual listing top-performing communitybanks of 2021 alongside interviews with some of the winners. In true communitybank fashion, each has its own story to tell and its own path to success. In true communitybank fashion, each has its own story to tell and its own path to success.

These actions can result in costly civil penalties and reputational damage, so banks and credit unions should take proactive steps to ensure their BSA compliance programs are robust and effective. In a recent high-profile case , a major bank faced significant civil and criminal consequences for violating the BSA.

.; Bank of Montana, Missoula, Mont.; CNB Bank, Berkeley Springs, W.Va.; Midwest Bank, Norfolk, Neb. In our annual workplace survey, employees of ICBA’s best communitybanks to work for told us they benefit from engaging cultures, opportunities for advancement and innovative benefits. What great resignation?

Investments in financial technology have been increasing for years, but the events of the last 18 months have created a new sense of urgency for communitybanks and credit unions to fine-tune their digital strategies across the spectrum of various fintech investments.

This development is creating an opportunity for communitybanks to book longer-term fixed-rate loans with higher profit margins. However, borrower demand is forcing banks to make loans with 5, 10, and even 20-year fixed-rate maturities. CenterState Bank uses a strategy that enables the pricing of

In June of 2008 I gave a speech titled "The Death of the CommunityBank" and in that speech I made predictions. Prediction: The General Bank will become extinct. Much like competitors nip at communitybanks' customers. Eighteen percent of that group opened an account at a digital bank. Result: Mixed.

When you are Chief Strategy Officer for a bank, sometimes your work load doesn’t come in neat memos or emails. In fact, the number one issue among communitybanks right now is the nebulous “Need to increase profitability” which for more than half the estimated banks is an easy one to solve

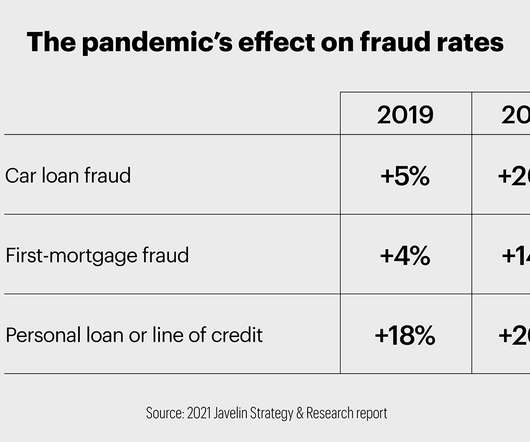

Experts say communitybanks can use education, biometrics and solid cybersecurity practices to fight this growing area of crime. Say a scammer calls a communitybank customer and gains their trust by using information obtained from a major data breach. By Elizabeth Judd. Examples of remote authentication fraud.

Communitybanks own an enviable amount of data, but not all are leveraging it to its fullest extent. By Mindy Charski People share important data about themselves with their communitybank in myriad ways. Data about existing customers can even help communitybanks improve their efforts to find new customers.

In a previous article [ here ] we discussed why communitybanks need product managers to ensure that financial products and services are effectively developed, launched, and managed to meet customers’ evolving needs and the bank’s risk and profitability goals. Not all customers are the right fit for the product.

Banking association and payments company The Clearing House (TCH) has been confronting such concerns as it advances its real-time payment ( RTP ) offering in the U.S., according to Steve Ledford, TCH’s senior vice president of Product Strategy and Development. Facilitating Uptake.

As a change agent serving the financial services industry for over 20 years, it is a great privilege to collaborate with Bank, Insurance, and Wealth Management institutions to devise and execute digital transformation strategy, solve complex business problems, and leverage technology to strengthen business results.

With megabanks spending billions on digital investments each year, regional and communitybank executives understand they cannot compete on resources. Instead, these players are focusing on specific niches, brand strategies and community connections to differentiate themselves. Appoint Digital Ambassadors.

Source: FRED With deposits trickling back into the banking system and the promise of a potential rate cut this year, banking executives are experiencing a glimmer of hope. Instead, it’s time to build deliberate strategies to ensure a sustainable approach to deposit growth. Optimize pricing strategies.

Fallout from recent global events presents an obstacle to generating revenue for communitybanks. As we enter budgeting season, the answers might be found in a mix of strategies. It’s certainly an interesting time to be a communitybank, but there are still plenty of ways to make efficiencies with an eye on profitability. ?

As communitybanks navigate this process, there are plenty of resources available to answer questions and provide guidance. After much strategy, planning and discussion, the implementation phase has arrived. Photo by Ismail Rajo/iStock The time has come for the long-awaited FedNow launch.

FDIC-insured “Problem Banks” list has been increasing over the past two years. For the communitybanking industry (banks under $10B in assets), this is particularly troubling as the number of communitybanks earning negative return on equity (ROE) spiked to 237 institutions in Q1/24, or 5.71% of all communitybanks.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content