This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In today’s banking world, community banks are focused sharply on shareholders’ expectations for growth in earnings and return on equity. So, how can community banks support earnings and ROE growth in the face of intense regulatory scrutiny and competitive pressures on profitability? Changing Lending Environment. What's Next.

The financial services industry must consider its customer experience game while also grappling with a sense of distrust from many communities due to systematic barriers, maintaining utmost accessibility due to the essentiality of the business, and the lack of financial literacy across the country. Trust and Transparency. .

On September 7, 2023, the FDIC released its banking profile. This quarterly publication provides a comprehensive financial results summary for all FDIC-insured institutions (4,645 commercial banks and savings institutions insured by the FDIC). Rising market interest rates. While banks under $10B in assets comprise 97.8%

Community banks (under $10B in assets) serve a key role for borrowers, local communities, and the broader US economy. Community banks are better positioned than many other creditors to follow and adapt to local economies, industries and trends, thereby, being better stewards of capital.

is set to see its first new community bank in decades, as the Federal Deposit Insurance Corporation (FDIC) lent its approval for MOXY Bank to launch in Washington, D.C. With clearance to move forward with its plans, the community banking landscape will see its first new industry player in years. have emerged to do.

Community banks’ use of swaps (banks’ primary tool to hedge interest rate risk on loans) has increased substantially over the last ten years. The market expects the current inverted yield curve to remain through much of 2024 (based on long-term interest rates and the expected rate cuts in 2024). Only 304 banks (or 6.7%

How can community financial institutions thrive in 2021? Community banks provide unique and important banking services for their customers, but they also face significant obstacles. Takeaway 1 Community banks play an important role in the economy and their communities, but they face significant obstacles.

Rising-rate environment Planning ALM strategies In today's volatile economic landscape, managing interest rate risk has become a top priority for community banks. The market has seen significant fluctuations, and with the Federal Reserve's recent actions, the banking sector is experiencing unprecedented challenges.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Community banks’ main goals are to diligently support their local communities and make an acceptable return on capital in these challenging times.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Community banks’ main goals are to diligently support their local communities and make an acceptable return on capital in these challenging times.

Add FDIC Chairman Martin J. The FDIC said that the percentage of loans and securities with maturities of three or more years hit the highest percentage in the 18 years of data records, rising to 34.6 Community banks have grown their share of longer-term assets even more quickly than the rest of the industry, according to the FDIC.

Community bankers are largely positive about the future, based on the first results of a new index gauging business sentiment among the financial professionals who serve a critical role in local economies. These insights have the potential to inform the market and policy makers on the overall health of the economy, opportunities, and risk.”.

In June of 2008 I gave a speech titled "The Death of the Community Bank" and in that speech I made predictions. Much like the General Store fell victim to the supermarket and the lumber yard fell victim to Home Depot, I predicted the community bank that did not pick targeted customer niches or develop product expertise will meet it's doom.

Independent Banker’s annual listing top-performing community banks of 2021 alongside interviews with some of the winners. In true community bank fashion, each has its own story to tell and its own path to success. In true community bank fashion, each has its own story to tell and its own path to success. Philadelphia.

According to a recent survey from four Federal Reserve Banks, small regional and community banks have the highest approval rate for small business loans. Small regional and community banks had a much higher approval rate (90 percent) for those firms classified as “Growers.

With big banks pulling back from small and medium-sized business (SMB) lending in the wake of the global financial crisis, the market was ripe for someone else to fill the credit gap. Community banks approved 49 percent of SMB loan applications in November, according to the latest data from the Biz2Credit Small Business Lending Index.

includes (from left): Christina Johantgen (head of marketing and creative), Joe York (head of product), Kelsey Cahill (summer associate), Jackie Charron (chief operating officer and executive vice president), Debbie Morin (chief financial officer), and CEO Charley Cummings. The team at Walden Mutual, a planned de novo in Concord, N.H.,

FDIC-insured “Problem Banks” list has been increasing over the past two years. For the community banking industry (banks under $10B in assets), this is particularly troubling as the number of community banks earning negative return on equity (ROE) spiked to 237 institutions in Q1/24, or 5.71% of all community banks.

Community financial institution (FI) Cross River Bank is acquiring Seed , a small business (SMB) digital banking company, reports in Reuters said on Monday (June 24). Its takeover of Seed strengthens its position in the small business FinTech market. Its takeover of Seed strengthens its position in the small business FinTech market.

Last week we wrote about loan-level vs. balance sheet hedging for community banks and provided our loan proposal generator ( HERE ). We compared and contrasted the two strategies and sized the market for community banks. A community bank may transact one or only a few balance sheet hedges over many years.

The current policy directions from the new administration are largely inflationary, and community banks should be paying attention and consider a loan-level hedge strategy. In this manner, banks can enjoy customer profitability through all types of market conditions and can simplify their process. As of Q3/24, there were almost 4.5k

FDIC officials in March outlined several types of weaknesses in loan underwriting, administration and oversight practices that are emerging at some banks with CRE portfolios. Eberley, director of the FDIC's Division of Risk Management Supervision wrote in the publication.

However, for community banks (under $10B in assets), the ROE declined to 10.44% (from 10.57% in the previous quarter). The Data In Q2/24, the number of FDIC insured community banks declined to 4,104 (a decrease of 27 community banks for the quarter). of all community banks had negative ROE for the quarter.

Most community bankers we talk believe they will get a boost to bank performance with declining short-term rates. A change in market interest rates seems to be an example where a bank’s NIM may change, and all other variables remain the same. Unfortunately, the empirical evidence shows otherwise.

Co-signed by the American Bankers Association, Bank Policy Institute, Independent Community Bankers of America and The Clearing House, the letter argues that banks and non-bank technology firms are both already embracing innovation in customer service offerings. FDIC), the states and the courts.

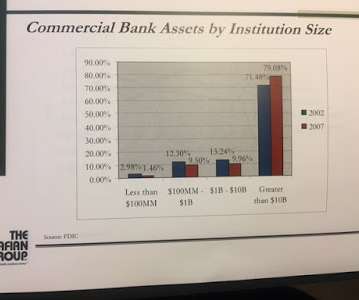

How should community banks target and compare their ROE to the industry and their peer group, and what defines a top-performing bank? Bank ROE Historical Performance Total assets for all FDIC-insured institutions was $23.7T Community banks (assets under $10B) composed 14.3% Community banks (assets under $10B) composed 14.3%

The FDIC today said it has partnered with the nonprofit Operation Hope to promote financial education to minority and women-owned businesses. Through the partnership, Operation Hope will use the FDIC's Money Smart financial education resources to help teach how to do business with the agency.

.” Other critics have raised the issue that the OCC is advising examiners to take community group concerns into consideration separately from their M&A approval processes. ” Now, Powell is also raising concerns about how bank industry consolidation could negatively impact the small business community.

More construction loan monitoring ultimately decreases loan default, according to a new FDIC Center for Financial Research working paper. The paper, “ Bank Monitoring with On-Site Inspections," will be presented later this month at the Community Banking in the 21st Century Research and Policy Conference.

The ABA’s 2015 Survey of Bank Compliance Officers , conducted February through March 2015, had participation from more than 450 financial institutions, with almost 80 percent being community banks. ABA president and CEO, Frank Keating, commented that Dodd-Frank has impacted banks, their customers and the communities they serve.

However, as of Q2/22, the average community bank’s COF has risen only a few basis points. Community banks should be concerned about their COF because looking at current deposit conditions is like driving a car while looking at the rearview mirror. Community banks will feel the effects of these hikes over the next few quarters.

A secure, open-loop, cost-saving, customer-accessible, multiplatform P2P payments network might sound too good to be true, but community bank consortium Alloy Labs Alliance hopes to achieve just that with the CHUCK payment rail. A different kind of peer-to-peer payment service is now available, “built by community banks for community banks.”.

Takeaway 3 Community banks have seen less volatility in noninterest income, and many are still eyeing growth across the category. Noninterest income associated with the housing markets such as securitization, trading, and real estate slowed significantly during the financial crisis and beyond. Community banks target growth.

The regulators also let banks know their position on using reserves and buffers during times of stress in the market, and whether that would lead to future penalizations. Also, it said that the lending would help a bank’s Community Reinvestment Act (CRA) score. Regulators, for their part, said they want to encourage lending.

Community financial institutions are familiar with utilizing their asset/liability management solutions to limit the risk of rising interest rates. FDIC FIL-46-2013 October 8, 2013. However, back when the FDIC sent that 2013 letter mentioned above to financial institutions, the effective federal funds rate was 0.09%.

Despite the painful evolution in retail, many experts expect another year of growth for commercial real estate – and for commercial real estate lenders, including community financial institutions. Community financial institution lenders, however, will want to “pick their spots” for CRE loans this year. Real Estate Market Outlook.

Banks of all sizes are hearing from many customers that they want exposure to the fast-growing but volatile cryptocurrency market. Vast Bank recently became the first nationally chartered, FDIC-insured bank to offer crypto banking. The post How a Community Bank Launched a Retail Crypto Platform appeared first on ABA Banking Journal.

On the liability side of SVB’s $173B in deposits at the end of 2022, approximately 97% were uninsured and above the $250k in FDIC protection threshold. The SVB Takeaway For Community Banks Community banks should continue to monitor their deposit base, liability sensitivities, and duration risks.

Based on the futures market, the Federal Reserve is expected to raise the Fed Funds rate to 3.00% at its December 2022 meeting. In this article, we analyze the industry’s cost of funding earning assets (COF) and track how community banks’ COF behaves relative to larger banks. Historical Cost of Funds Analysis. Future Short-term Rates.

After moving alone in 2020 to reform its Community Reinvestment Act (CRA) regulation, the Office of the Comptroller of the Currency (OCC) has joined the Federal Deposit Insurance Corporation (FDIC) and Federal Reserve Board in issuing a joint notice of proposed rulemaking setting forth proposed amendments to their regulations implementing the CRA.

Banking technology decisions now affect future growth With the possibility of a recession, community financial institutions may consider a delay or cut in technology spending. But a community financial institution often has different needs related to origination than those of a giant lender. Experts say that would be a mistake.

Other podcasts might be internationally based and of little interest to community financial institutions or credit unions based in the U.S. or largely focused on the domestic banking market. Main Street Banking: A Podcast for Community Bankers 8. So here’s your head start on finding some banking podcasts that might work for you.

The OCC, FDIC, and Federal Reserve Board have issued a guide that is intended to assist community banks in conducting due diligence when considering relationships with financial technology (fintech) companies (Guide). Financial condition and competitive market environment and client base. Legal and regulatory compliance.

The FDIC designated SVB as systemically important. I chose five years because banks that focus on year-over-year returns tend to cut strategic investments come budget time, which hurts their market position, earnings power, and future relevance more than those that make those investments. million in net income for an ROA of 0.73%.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content