This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The recent uncertain shifts in trade policies, particularly increased tariffs on imports from China, Canada, and Mexico, have introduced specific uncertainties for community banks. However, for community banks, these challenges can also present some opportunities.

Now that the cannabis industry is maturing and better understood, is it time for financial institutions to take on the risk of cannabis lending? Cannabis-related businesses (CRBs)spanning everything from cultivation to retailrepresent a market in need of lending services, from working capital to real estate and equipment loans.

The yield curve is currently flat, and the average community banks cost of funding is highly correlated to Fed Funds and SOFR (the industrys average is over 90% with a about a 6-month lag). The graph below shows the lending curve, based on a 25yr amortization, and 2.50% credit spread for terms ranging from monthly reprice to 20yr fixed rates.

Partnering with local organizations to promote the health of their economic communities is often a top priority for banks. In recent years, financial institutions have faced increasing regulations regarding their efforts to serve the needs of diverse communities. Must report on loan distribution and loan-to-deposit ratios.

What should you look for in a Business Lending Platform? This eBook explains the features of a Business Lending Platform that community banks should make their top priorities when evaluating any business lending software.

In our previous article ( here ) we analyzed the data on community bank M&A and performance, and we concluded that there is no relationship between community bank size and profitability, as measured by return on equity (ROE). While size isn’t correlated to profitability, operating leverage is.

While significantly more efficient than mailing forms to the SBA, there are some shortfalls to E-Tran, and a vendor can help Loan submission platform Leveraging E-Tran for increased SBA lending The U.S. Understanding the role of E-Tran in SBA lending is the first step for banks and credit unions to ensure smooth loan processing.

Bank and credit union leaders can use data to inform small business lending Small businesses are showing resilience. As rates stay high, concerns about credit risk and borrower health are top of mind for bank and credit union leaders, especially as it relates to lending to small businesses. Interest coverage ratios have stayed strong.

Automating the key steps that often occur in the back office leads to faster decisions, stronger customer or member relationships, and more profitable lending to small businesses. This article covers these key topics: Cultivating fertile ground for small business lending Do large lenders have an advantage in small business lending?

And to thrive, those customers need economically diverse and healthy communities in which to live and work. Partnering with local organizations to promote the health of those communities is often a top priority for banks. communities where capital tends to be scarce.

Businesses of a certain size — and in industries as varied as construction and restaurants — know the pain of wondering if they will have enough capital to fund operations, inventory, expansion and other mission-critical business activities. When it comes to SMB lending, PayPal has gone global. and global economy. and global economy.

For more community banks, the latter strategy can fast-track digitization initiatives. This week’s look at the latest bank-FinTech tie-ups shows Banking-as-a-Service and other FinTech players embracing smaller regional and community banks to elevate small- to medium-sized business (SMBs) and corporate banking offerings.

Recent data and trends of the small business lending market SMB Lending Insights is a snapshot of current financial trends and metrics that impact small and medium-sized business (SMB) lending and financial institutions. You might also like this guide for smarter, faster small business lending.

Key Takeaways Financial institutions who want to maintain a healthy share of business lending this year and through potentially tougher economic times ahead want to be in the best position possible before trouble hits. Abrigo's Business Lending Readiness Survey found many processes stymie those efforts. learn more.

In a previous article [ here ] we discussed why community banks need product managers to ensure that financial products and services are effectively developed, launched, and managed to meet customers’ evolving needs and the bank’s risk and profitability goals. Not all customers are the right fit for the product.

The most-read lending & credit blogs in 2023 Probability of default, CECL model validation, and stress testing were among Abrigo's top blogs on ALM, CECL, and portfolio risk this year. download NOW Takeaway 1 The most popular blog posts on the Abrigo site reflect many of the priorities community banks and credit unions had in 2023.

Our recognition as the #3 community bank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. consumers now consider digital banking capabilities essential (Latinia, 2024)while operational pressures require us to do more with less. What is Microsoft Copilot?

Learn why Unique needs & challenges Each financial institution is unique, and adopting new technology requires thoughtful integration withor changes toexisting operations. Feedback from community financial institutions highlights how a vendors team can influence adoption success across the organization. They are my allies.

Key Takeaways In today's uncertain economic climate, community financial institutions must resolve to manage risk and drive growth. Low interest rates and slowing growth in loan demand can put community financial institutions in a difficult position; therefore, competing effectively and mitigating any increased risk should be a top priority.

Community bankers need to understand their competitive landscape. Who the competition is, what the lending competition is offering, their delivery channels, and service levels can help community banks differentiate their services and enhance their competitive advantage.

That’s even more true for community banks, which lack the resources larger FIs have to support modernization initiatives and technology investment efforts. At the same time, the logistical challenges and competitive pressures associated with digitization remain just as pertinent for community banks.

Historically, community banks have relied on net interest margin (NIM) instead of fee income to drive return on equity (ROE). For example, 40% of JP Morgan’s commercial banking revenue is derived from fee income, and JP Morgan’s commercial banking division is composed of middle-market and commercial real estate (CRE) lending.

Personalized Touch with Efficient Service Can Boost Lending Banks and credit unions can boost business lending by combining a relationship focus with transaction-oriented processing. . This competition can only increase as the lending landscape continues to shift.

Ready to catch the next wave of lending growth? Commercial and industrial lending (C&I) will be the next big performance driver for banks and credit unions. You might also like this paper on how institutions can produce smarter, faster lending. C&I lending will be the next “bomb.”

Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. WATCH Investment accounting compliance risks U.S.

smaller community banks and credit unions (CUs) stepped up to the plate and, according to the Small Business Association (SBA), ended up facilitating more than half of PPP loan volume to SMBs. That's good news for community banks and credit unions, which could see a wave of new SMB customers and members in the coming months.

Here’s how four community banks are thriving in this environment. Clearly, community banks in the region have plenty of opportunities to do what they do best: forge deep and lasting relationships with their customers and communities. These include family-owned businesses, community businesses and operating companies.

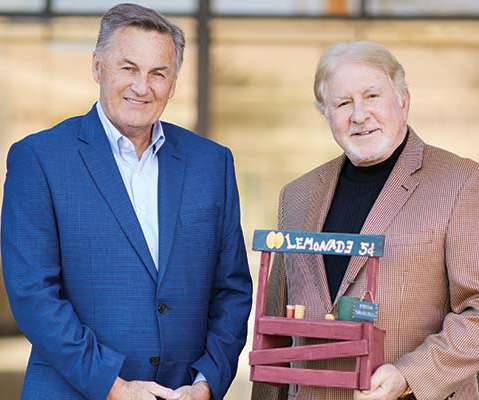

Inspired by the entrepreneurship of lemonade stands, Scottsdale Community Bank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale Community Bank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

Although the above example is a large bank, similar enforcement actions are being handed down to community banks. By being proactive, banks can safeguard themselves from regulatory penalties and ensure their operations align with evolving compliance standards. Provide timely updates in response to changes in regulations.

Loan providers share an infectious enthusiasm and growing optimism for one vertical’s prospects in 2022: commercial lending. Here’s how community bankers can take advantage of various sectors—including SBA lending—over the next 12 months. anticipates a low double-digit increase in its commercial lending in 2022.

Strong demand is a factor in the ag lending outlook ahead Ag lenders can begin taking steps to ensure they are prepared and can provide positive customer or member experiences. The outlook for ag lending has its share of uncertainty. Inflation, rates are factors in ag lending outlook. Farmers expect worse in 2023. Rising inputs.

Here’s what community bankers need to know when planning their budgets for the next year. These days, there’s a lot to contend with as a community bank, from changing consumer behaviors due to the pandemic to uncertainty surrounding the economy and inflation. Build a lending niche. By Cheryl Winokur Munk. Quick stat. Paul, Minn.,

But the latest initiatives reveal a growing interest in transforming internal processes, particularly among smaller banks looking to upgrade their core infrastructure and elevate small business lendingoperations. Hawthorn River Eyes Open Banking for Community FIs. Bectran Augments Cash Application With API.

Santander Bank has announced three high-level appointments, two overseeing lendingoperations and another overseeing marketing, according to a press release. Giancarlo Marchesi was named head of Consumer Lending, a new role at Santander. Patrick Smith was named head of Small Business Banking. Smith holds a B.S.

Some of the largest global financial institutions are taking steps further into Mexico’s small business lending and finance space, the result of heightened competitive pressure imposed by FinTechs and alternative lenders in the market, reports in the Wall Street Journal said Thursday (March 14).

These community banks are working to fix that through microlending programs. Now, some community banks are launching microlending programs to redress the balance. which operates $12 billion-asset OceanFirst Bank N.A. The bank partnered in early 2021 with Community LendingWorks, a Springfield, Ore., By Beth Mattson-Teig.

From leveraging PPP technology to building relationships, reasons for boosting SBA lending are numerous. . Takeaway 1 SBA lending can expand your product offerings to help win deals with prospects and existing business customers or members. Why SBA Lending? Would you like others articles like this in your inbox? 1 and Sept.

JPMorgan Chase is planning the consolidation its corporate payment operations by combining small business (SMB) and large enterprise solutions, the Financial Times ( FT ) reported on Thursday (Jan. and internationally,” said Co-President and Chief Operating Officer Daniel Pinto in the memo.

Now, many of the nearly 5,500 SBA-approved lenders that are participating in the PPP are weighing the option of leveraging that technology to continue to provide SBA lending after PPP. Leveraging tech for SBA lending after PPP. Or, they might wonder whether it’s too late to start 7(a) lending if they’ve never done it before the PPP.

Now, many of the nearly 5,500 SBA-approved lenders that are participating in the PPP are weighing the option of leveraging that technology to continue to provide SBA lending after PPP. Leveraging tech for SBA lending after PPP. Or, they might wonder whether it’s too late to start 7(a) lending if they’ve never done it before the PPP.

If that trend continues, operating costs will begin outpacing revenue for many farms, and demand for ag financing will grow for community financial institutions. Assigning credit risk is tricky with ag lending since both environment and economic factors carry significant weight. Pay strategies. Blanket security agreements.

Independent Banker’s annual listing top-performing community banks of 2021 alongside interviews with some of the winners. In true community bank fashion, each has its own story to tell and its own path to success. In true community bank fashion, each has its own story to tell and its own path to success. Philadelphia.

Premium benefits packages, professional development and TLC during the pandemic—this year’s winners do everything in their power to keep their community bankers happy and fulfilled. We asked both leaders and staffers to tell us what makes their community banks stand out as employers. Key Community Bank: Leading by example.

For community banks and credit unions, their physical proximity to the small businesses they’re servicing is often pointed out as a major advantage these smaller players hold over the big banks, enabling these FIs to develop deeper relationships with their small to medium-size business (SMB) clients, anticipate their needs and establish trust.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content