This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The yield curve is currently flat, and the average community banks cost of funding is highly correlated to Fed Funds and SOFR (the industrys average is over 90% with a about a 6-month lag). Historically, loan hedging required substantial resources for documentation, accounting, legal, marketing and operations.

In this article, we highlight some Gen AI strategy insights for community banks and provide tools to help bankers advance their programs. Few community banks have the resources to accomplish both, and both are sizeable efforts. Coming Up Next Banking leaders can leverage Gen AI to address key business and operational challenges.

Perficient developed the La Puerta portal framework as a way of giving back to the Detroit community and to pave the way for students to benefit from a college education. The Michigan Hispanic Collaborative’s goal to improve the economic strength of the Hispanic community in Michigan. “We ” In Michigan, only 15.7%

While we are supporters of community banks using loan-level hedging, we continue to see community banks struggle to properly implement and successfully utilize a back-to-back swap (B2B) program. We understand why, and what community banks need to address to make such a program a success.

And to thrive, those customers need economically diverse and healthy communities in which to live and work. Partnering with local organizations to promote the health of those communities is often a top priority for banks. communities where capital tends to be scarce.

Partnering with local organizations to promote the health of their economic communities is often a top priority for banks. In recent years, financial institutions have faced increasing regulations regarding their efforts to serve the needs of diverse communities.

Connect with an expert Common fraud schemes Check fraud Check fraud is one of the most concerning fraud trends for community banks in 2025. Ponzi schemes A fraudulent investment operation that pays returns to earlier investors using money from new investors rather than legitimate profits. Staying on top of fraud is a full-time job.

The expanded executive leadership team will drive continued growth and operational excellence across Perficient while delivering superior solutions for clients. “As ” Prakash Chembai, AVP of India global delivery operations. She will provide resources to scale client projects and speed time to market. Ostasz, AVP of U.S.

As community banks navigate this process, there are plenty of resources available to answer questions and provide guidance. Three sources of information on FedNow As community banks look to take advantage of this new opportunity, they seek resources to help them navigate the journey.

Here are the top resources. Papers, infographics on risk management Resources related to banking headlines were popular For banking risk and accounting staff, managing challenges tied to interest rates, liquidity, and credit portfolios will remain top-of-mind in 2024.

While the final guidance clearly applies to larger financial institutions, community banks should still take note. ” The section further details this would only occur under extraordinary circumstances, but community banks should be aware of the new framework and even consider applying the guidelines as a proactive, best practice.

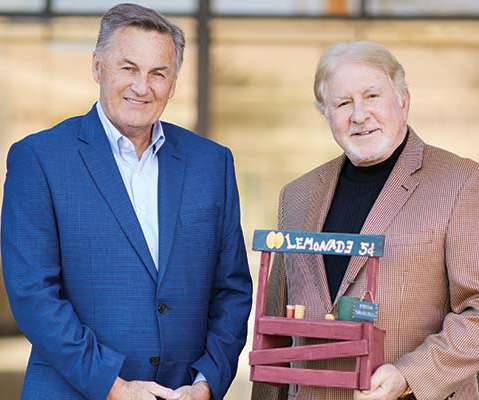

Inspired by the entrepreneurship of lemonade stands, Scottsdale Community Bank created a microloan program. Photo by Brandon Sullivan De novo Scottsdale Community Bank set out to provide microloans to small and mid-size businesses, family organizations and nonprofits—a project that was inspired by the humble lemonade stand.

Humanity, Courage, Selflessness, Sacrifice, Kindness, Conscious well-being of self and fellow beings, Judicious usage of available resources and more so have become the need of the hour. Cataract Operation sponsorship. Some more unique items that were qualified based on the tagline were: Livestock for livelihood.

Although the above example is a large bank, similar enforcement actions are being handed down to community banks. By being proactive, banks can safeguard themselves from regulatory penalties and ensure their operations align with evolving compliance standards. Provide timely updates in response to changes in regulations.

That’s even more true for community banks, which lack the resources larger FIs have to support modernization initiatives and technology investment efforts. At the same time, the logistical challenges and competitive pressures associated with digitization remain just as pertinent for community banks.

This year’s winners: Left: Central Valley Community Bank, People’s Choice Award; Middle: Kennebec Savings Bank, Exceptional Community Bank Service Award; Right: Cross River Bank, Emerging Service Program Award. Exceptional Community Bank Service Award. Instead, we give those dollars to the community.”. Asset size: $1.36

However, it is doubtful you utilize a complete operating system. This article discusses using EOS in banking – the Entrepreneurial Operating Model. The CEO can talk to everyone and communicate effectively daily. However, as a bank grows, communication gaps, unclear roles, and inefficient processes begin to creep in.

Here’s how four community banks are thriving in this environment. There’s a lot of energy in the southern half of Texas, and it’s not just the resources that power our homes and cars. We spoke with four community banks in the southern half of Texas to learn how they are serving this buzzing region. By Mindy Charski.

Community Financial Services Bank, Benton, Ky.; In our annual workplace survey, employees of ICBA’s best community banks to work for told us they benefit from engaging cultures, opportunities for advancement and innovative benefits. We don’t operate from a position of fear.”. Bank of Montana, Missoula, Mont.; By Roshan McArthur.

Premium benefits packages, professional development and TLC during the pandemic—this year’s winners do everything in their power to keep their community bankers happy and fulfilled. We asked both leaders and staffers to tell us what makes their community banks stand out as employers. Key Community Bank: Leading by example.

With consumer expectations seeming to evolve faster every year, community banks could consider partnering with a fintech to keep up with technological innovation. Swashbuckling, nimble, well-funded and unapologetically entrepreneurial, fintechs are offering innovations that allow community bankers to dream big in a host of ways.

According to Brennan, EforAll is a growing nonprofit organization that partners with communities to help under-resourced entrepreneurs start and grow a business through intensive business training, mentorship and an extended professional support network. EforAll began operating in Holyoke in 2018 and in Roxbury in 2019.

The FedNow Service enables community financial institutions to stay competitive by meeting instant payment demands. Takeaway 2 It's important to review resources on how to prepare for FedNow and also look internally to create a plan for your unique financial institution. Make FedNow work for your bank or credit union.

The grants are part of the San Jose, California-based worldwide online payments system’s $530 million pledge made earlier this year to strengthen minority communities and fight for economic equality and racial justice. “To In addition to the donations, PayPal employees volunteered to work with these nonprofits.

Enable 2FA: Use two-factor authentication for managing access to resources. You can get involved at home, at work, and in your community. See open jobs or join our talent community for career tips, job openings, company updates, and more! Password Rotation: Change your passwords every 90 days or less.

The Clearing House’s RTP finds expansion within the community bank arena, while abroad, the Bank of Thailand is planning its own infrastructure development to accelerate B2B payments. RTP Gains Community Bank Traction. In the U.S., And when it comes to legacy rails, the U.S. ” HSBC Debuts Real-Time Direct Debit. .

They focus predominantly on swiftly implemented self-service, community support, communication, and outreach. Boost existing resources with powerful enhancements. Automate user interaction with chatbots. Meet call center demand… at scale. Cultivate rapid, tailored outreach powered by CRM.

Operational innovation is vital in a highly competitive financial services sector, with a new community of digital banks and other firms vying for market share. Drivers for Operational Innovation. These terms look good on paper, but what do they mean in practice for operational innovation?

Community banks are pushing for a stronger role with their small business (SMB) customers. However, through an embrace of FinTech collaboration and industry consolidation, community banks appear poised to further dispel assumptions of a lack of digitization. has dropped from 8,000 in 2004 to about 5,400 in 2018. Strengthening SMB Ties.

Community banks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for community banks. But there’s plenty community banks can do to meet this challenge. Fraud and cyber attacks are on the rise, and at great expense to the industry.

Community banks pride themselves on superior customer service. Approximately 90% of all community banks believe that they provide an above-average level of customer service (of course, the math cannot work that way, as half of all banks should be providing a below-average level of customer service).

This merger combines the best of both companies and provides the scale and resources to drive increased long?term He added that the two companies are stronger together and in a better position “to support our customers and drive economic growth in the communities we serve.” . regional banks. . term shareholder value. winning people?first,

Sheryl Sandberg, chief operating officer of Facebook, said on her page and in a blog post on Tuesday (March 17) that the social media giant wants to “do our part” to help with the “enormous challenge in front of us.”. Whatever happens next, we will be working to help businesses weather this storm.

Online account opening remains the wild west for most community banks. And naturally I was keenly interested in how to solve this problem, or even diagnose what exactly is the problem, for community banks and online deposit account opening, either retail or business. Community Savings had a >100% loan-to-deposit ratio.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Community banks’ main goals are to diligently support their local communities and make an acceptable return on capital in these challenging times.

An inverted yield curve, continued bank failures, and the desire to manage risk and offer clients higher service are all factors that are driving more community banks to adopt a loan hedge program. Community banks’ main goals are to diligently support their local communities and make an acceptable return on capital in these challenging times.

Many banks pride themselves on superior customer service, and approximately 90% of all community banks believe that they provide an above-average level of customer service (the math cannot work that way). Service (a scarce resource) must be directed at its highest return.

Back-end processes for small business loan approval in some financial institutions operate in an automation desertand it shows. Automation fosters efficiency, accuracy, and the support that community businesses need. Theyre energy-draining, slow-moving, and inefficient.

Prepare now for potential changes to FHLBs Capital rules and membership criteria are among the areas where banks could see changes in how the Federal Home Loan Bank system operates. You might also like these popular resources on interest rate risk, liquidity, and CECL. Would you like other articles like this in your inbox?

Other podcasts might be internationally based and of little interest to community financial institutions or credit unions based in the U.S. We have webinars , whitepapers , and other resources to make your job easier. Main Street Banking: A Podcast for Community Bankers 8. The Community Bank Podcast 10.

Recent weeks have dramatically demonstrated how important it is for communities to be able to adapt and respond in the face of cataclysmic events, which requires them to have resilient systems in place. Smart sensors can ensure these resources are delivered cleanly and efficiently. Adapting to a Post-COVID-19 World.

The FDIC today said it has partnered with the nonprofit Operation Hope to promote financial education to minority and women-owned businesses. Through the partnership, Operation Hope will use the FDIC's Money Smart financial education resources to help teach how to do business with the agency.

Relationship focus helps CFIs Small banks can leapfrog competitors and better serve their communities by combining their unique advantages with smart management and partnerships. How can community financial institution leaders manage their challenges and seize their opportunities at the same time?

lags behind many other countries in financial literacy, meaning millions of Americans lack the resources they need to chart a healthier financial future. FICO is taking a number of steps to promote credit education and financial independence alongside our partners at Operation HOPE. Operation HOPE Global Board of Advisors.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content