This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Generative AI and the new loan review process The evolution of banking and riskmanagement over the past few decades has been nothing short of remarkable. Generative AI in credit riskmanagement is the latest step forward , offering a transformative approach to loan review. Data security is also a major concern.

At Abrigo, we’ve always focused on helping financial institutions thrive—not just for their own benefit but for the sake of the communities they serve. Think about it: when a fraudster targets a small business owner or when an individual’s life savings are wiped out, it doesn’t just hurt the bank—it devastates families and communities.

Stress testing, monitoring are essential Financial institutions should challenge assumptions about CRE risk while also watching for red flags as they manage the CRE portfolio. WATCH Takeaway 1 Banks and credit unions are critical sources of capital for businesses in their communities, so how institutions assess CRE credits matters.

Connect with an expert Common fraud schemes Check fraud Check fraud is one of the most concerning fraud trends for community banks in 2025. These could be held in a local branch lobby, community center, or place of worship. 880,418 c omplaints were registered, with potential losses exceeding $12.5

Equally important is the bank’s securities duration, as shown in the graph below. Approximately 56% of the bank’s securities had repricing greater than 15 years. SVB’s securities portfolio is high credit quality (Treasuries and quality MBS) but long duration. at the end of 2022, with $2.4B

Our recognition as the #3 community bank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. Our recognition as the #3 community bank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve.

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny.

How can community financial institutions thrive in 2021? Community banks provide unique and important banking services for their customers, but they also face significant obstacles. Takeaway 1 Community banks play an important role in the economy and their communities, but they face significant obstacles.

Automation fosters efficiency, accuracy, and the support that community businesses need. Automation offers a secure digital portal for borrowers to upload documents and can flag missing items and send reminders so that applications have all the necessary information and documents for processing and review to begin.

Wells Fargo, weeks after it was hit with a rare enforcement action from the Federal Reserve, is overhauling its riskmanagement processes and announced internally that four top riskmanagement executives would be retiring. All are retiring in April, May or June.

At a time when our nation’s secrets at the NSA and Homeland Security and assets at the Department of the Treasury were able to be illicitly tapped into by foreign hackers, the security and reliability of countless other online industries and enterprises have also been brought into question. Not All Bad.

Community banks have a choice about addressing the problem: Remain vulnerable or be vigilant. Fraud and cybercrimes continue to increase, causing challenges for community banks. But there’s plenty community banks can do to meet this challenge. The bank works hard to prevent attacks with many defensive layers of security.

The statement provided examples of riskmanagement and other practices that may be effective in combatting this often-underreported crime. Common tactics include pretending to be from the IRS or Social Security Administration and threatening the victim with fines or legal action unless they pay immediately.

Furthermore, high federal government debt does not just lead to higher interest rates but also poses economic, national security, and social challenges. While the US is, and will remain, the center of innovation and risk-taking, the economy will transition to fewer small businesses and more larger enterprises.

Nonetheless, with the recent collapse of sizeable regional banks, regulators, investors, analysts, accountants, and bankers are now scrutinizing the fair value of banks’ securities and loan portfolios. This development should strongly motivate community banks to consider the benefits of loan-level hedging.

Credit risk : In C&I lending, at least part of the collateral is intangible. The emphasis for commercial credit riskmanagement and evaluation is cash flow, fixed charges coverage, and working capital cycles. Being ready to capture a share of the $1.7 Prepare for the next credit cycle.

Takeaway 2 Examiners' focus is on riskmanagement related to products and services , especially those involving complex technologies like AI. First, they must evaluate whether their institution is prepared to insert AML riskmanagement procedures into the transaction process to match the speed FedNow can offer.

The root cause of Silicon Valley Bank’s (SVB) failure is poor riskmanagement – plain and simple. Bankers need to understand and manage their business on the fair value of assets and liabilities instead of managing their business on net interest margin and the amortized historical cost of assets and liabilities.

Small business lending is also a prominent line of business for many financial institutions, especially those driven by a mission to help their communities thrive. While small business loans inherently benefit business owners, they also benefit communities, according to 2021 research for the SBA. Louis Fed : [S]mall-business loans—i.e.,

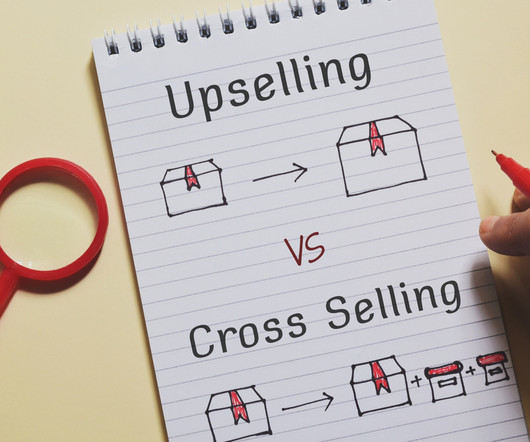

In a future article we will discuss how community bankers may structure their commercial loan products to maximize cross-selling and upsell opportunities. With proper tools and strategies, community bankers can upsell and cross-sell their products to maximize profitability. In banking, those numbers are markedly different.

These DFS500 amendments signal a crucial shift in the regulatory landscape, emphasizing the imperative for robust governance, riskmanagement, and compliance frameworks across the financial industry.

The NYSDFS Part 500 amendments signal a crucial shift in the financial services regulatory landscape and underscore the importance of robust governance, riskmanagement, and compliance frameworks.

ProfitStars , the Jack Henry & Associates division that provides riskmanagement solutions for financial institutions, announced its latest fraud tool on Wednesday (Sept.

Banking reports to inform riskmanagement and strategy These reports on capital, growth, and liquidity help financial institutions spot warning signs. They help manage and shape strategy in volatile economic and industry conditions. the Community Bank Leverage Ratio (CBLR) and the minimum Tier 1 leverage ratio).

The OCC, FDIC, and Federal Reserve Board have issued a guide that is intended to assist community banks in conducting due diligence when considering relationships with financial technology (fintech) companies (Guide). Riskmanagement policies, processes, and controls. Information security program and information systems.

Small business lending is also a prominent line of business for many financial institutions, especially those driven by a mission to help their communities thrive. While small business loans inherently benefit business owners, they also benefit communities, according to 2021 research for the SBA. Louis Fed : [S]mall-business loans—i.e.,

Takeaway 2 AI can lead to more accurate and consistent outputs or predictions, better riskmanagement, and improved customer experiences. The utilization of generative AI has sparked legitimate concerns about data security. Learn how technology helped a financial institution during uncertain times.

Takeaway 2 Client fraud education at financial institutions should include takeaways that explain how to protect themselves from phishing and tips for staying secure online. While fraud detection software and robust security measures are essential, educating clients on fraud prevention is equally important.

While the larger banks are receiving the bulk of attention, boards at smaller, community banks are realizing that they’re not immune to this heightened attention. Lynn McKenzie and Edmund Green of KMPG recently contributed an article to Bank Director on how boards can challenge their banks’ management on risk. Audit committee?

Despite the painful evolution in retail, many experts expect another year of growth for commercial real estate – and for commercial real estate lenders, including community financial institutions. Community financial institution lenders, however, will want to “pick their spots” for CRE loans this year.

This helps me understand the FI’s products/services, business culture, and face to the community. I also like to check for staff pictures on the chance that I can put a face with a name for the particular employee that I am working with on IT regulatory compliance and riskmanagement efforts.

AmTrust recently worked with one community bank client that was the target of a ransomware attack that shut down its branches for two weeks. One of the biggest benefits of a cyber policy, especially for a smaller community bank, is access to experts,” says Gentile. System configuration: Securely configure systems and services.

Rising funding costs and decreasing liquidity at community banks are causing managers to change pricing methodology for new credits. We estimate that 25% to 50% of community banks have a policy requiring minimum yield or credit spreads for new commercial loans. The drop in liquidity ratios is expected to accelerate through 2023.

This week, enterprise security startup CyberGRX announced a new funding round, with investors at Bessemer Venture Partners leading the way for $20 million in Series B financing. The investment is not only a signal of VCs’ appetite for enterprise security offerings, but of enterprises themselves needing more sophisticated security tools.

Last year, community bank loan producers were faced with both record-low interest rates and a glut of deposits. But as they always do, they came through for individuals and businesses in their communities with a combination of personalized service and prudent riskmanagement practices. Security Bank Midwest.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. Other podcasts might be internationally based and of little interest to community financial institutions or credit unions based in the U.S.

Using regtech in banking With new federal regulatory and compliance challenges like the CFPB rule on the horizon, more and more community financial institutions are exploring regtech in banking and finance. Consider what compliance and risk functions your organization would use as a starting point when integrating technology.

Using regtech in banking With new federal regulatory and compliance challenges like the CFPB rule on the horizon, more and more community financial institutions are exploring regtech for banks to enhance their processes. Consider what compliance and risk functions your organization would use as a starting point when integrating technology.

That firm recently secured funding from Visa, which is also in the process of acquiring Plaid as part of its own wide-ranging open banking initiatives. Open banking startup Railsbank, founded by Currencycloud Founder Nigel Verdon, secured some high-profile funding with the recent investment by Visa, according to recent reports.

Financial crimes riskmanagement software company Quantifind and Oracle Financial Services have teamed up to improve anti-money laundering (AML) compliance and to add intelligence and automation properties directly into the compliance workflows, according to a release.

Community bankers need to practice realistic loan pricing discipline. However, we need to understand the meaning of pricing discipline and its effect on community bank performance. This is strong evidence that community banks are pricing to an arbitrary minimum credit spread in this set of loans.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content