This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

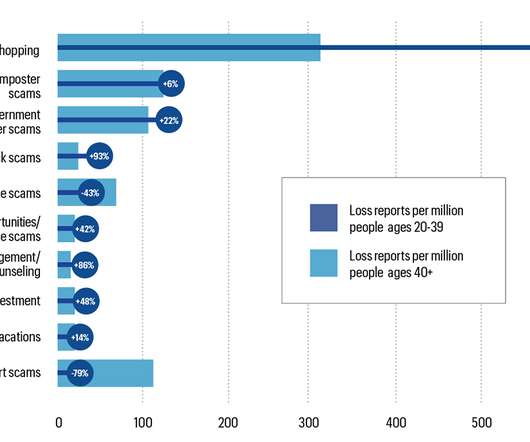

Connect with an expert Common fraud schemes Check fraud Check fraud is one of the most concerning fraud trends for community banks in 2025. Investment schemes : Investment scams lure victims with promises of high returns and little to no risk, only to steal their money. These scams often take place on dating apps and socialmedia.

Based on the bank’s own filing, and like many banks, SVB did not deploy hedging instruments to manage its securities duration risk. The SVB Takeaway For Community Banks Community banks should continue to monitor their deposit base, liability sensitivities, and duration risks.

The statement provided examples of riskmanagement and other practices that may be effective in combatting this often-underreported crime. Romance scams: These scams involve fraudsters building online relationships with elderly victims, often through socialmedia or dating apps.

The ABA has a new report out on how banks are using socialmedia, and much of the report focuses on using Twitter, Facebook, LinkedIn and the like to boost customer service, make connections in the community and recruit staff. 14) @News_CUInsight – CUInsight is an independent source of news on the credit union community.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. Other podcasts might be internationally based and of little interest to community financial institutions or credit unions based in the U.S.

A status update on banks and socialmedia. According to a statistic released as part of the ICBA 2014 Top 50 Community Bank Leaders in SocialMedia, nearly 2,500 banks have a Facebook or Twitter presence, and the numbers continue to exponentially grow. .* By Russ Horn, CoNetrix. Following the tweets.

Some blame the dilution of the Dodd-Frank provisions, others the lack of oversight by regulators, and others still blame socialmedia for exacerbating the deposit run. The root cause of Silicon Valley Bank’s (SVB) failure is poor riskmanagement – plain and simple.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. Other podcasts might be internationally based and of little interest to community financial institutions or credit unions based in the U.S.

This helps me understand the FI’s products/services, business culture, and face to the community. I also like to check for staff pictures on the chance that I can put a face with a name for the particular employee that I am working with on IT regulatory compliance and riskmanagement efforts.

Effective fraud riskmanagement includes detection and fraud monitoring that should consider customer or member history and behavior. Clients should also be wary of socialmedia scams. While interacting with friends and family online can be a fun pastime, social platforms are a feeding ground for fraudsters.

Recent bank failures hurting public perceptions, the current market trends of higher rates, Quantitative Tightening, digital banking, socialmedia, and a flight to safety have increased the difference between model and observed liability durations. Banks take a pool from 2018, as an example, and then track runoff to the present.

While we wrote about the root cause of the failure of Silicon Valley Bank (SVB) HERE , the lessons of the current banking crisis go beyond interest rate riskmanagement. While interest rate risk caused the most significant impact on value, several other factors contributed to the terminality of each bank that was closed.

In a world where information can be the most valuable currency, community banks are gathering more of their internal data. a bank software provider in Cedar Park, Texas, most community banks gather data well for reporting purposes. Drew McMullen, a partner and managing director for Sense Corp. They have lots of options.

We look at community banks’ options for fighting this type of crime. Community banks can find ways to mitigate age-related fraud through technology, as well as by educating their customers of their particular risks. Socialmedia. By Katie Kuehner-Hebert. A cohesive strategy. Baby boomers. Robo calls. Romance scams.

While some of the recent trending fraud schemes are not new, they have been transformed to prey on communities already dealing with unprecedented times. According to PWC , rising prices can have substantial implications on fraud risks. The downturn in the economy has undoubtedly affected fraud statistics as well.

In a world where information can be the most valuable currency, community banks are gathering more of their internal data. a bank software provider in Cedar Park, Texas, most community banks gather data well for reporting purposes. Drew McMullen, a partner and managing director for Sense Corp. They have lots of options.

Community-based institutions have unique circumstances (and personal viewpoints) that impact how they see the world in the future and what planning will look like for them. RiskManagement. Regulators are now ramping that back up, and model riskmanagement focused on portfolio risk is going to top the list.

Not the financial industry’s “Troublemakers ” – those regional and community banks, credit unions and supporting fintech entrepreneurs who continue to engage customers and communities and find niches that keep the grassroots of our country’s financial system alive and kicking. We are in awe. Seriously in awe.

Banks and credit unions had to fundamentally change their delivery, support and relationship management models at scopes and speeds that were unheard of. And how did community banks and credit unions respond to the COVID craziness? Jill is continually demonstrating just how loud a $300 million community bank can roar!

Here are seven key areas where bank executives need action plans to address burning challenges: Communication – Bankers have been working to calm their customers and community, but the quantity and quality haven’t yet met the standard in an always-on socialmedia world where the public is sniffing for transparency and authenticity.

The team also consists of Rachel Morrissey, executive producer of Fintech5, and Mike King, a fintech socialmedia leader and author of Bankwide. Topics include fintech, riskmanagement, blockchain, fraud detection and more. Bank on IT. BAI Banking Strategies.

If you operate in any regulated industry, you need to assure both the regulatory community and your clients that you are acting in the best interests of the customer. In most cases, riskmanagement and compliance teams haven’t been able to evolve quickly enough to keep pace with the relentless ingenuity of the wrongdoers.

A striking dynamic has occurred among regional and community banks over the past 10 years: their assets have grown much faster than their maturity. It is an active risk program integrated across the bank where owners take charge of their assigned riskmanagement activities. #5:

This past week I attended the American Bankers' Association National Conference for Community Bankers (NCCB). This factoid is sure to get me socialmedia shares from environmentalists. At such affairs, I like attending the general and education sessions for my own knowledge, and for the benefit of my clients and readers.

There is strength in numbers, and there’s absolutely no reason for community bankers to try to compete against players a hundred times bigger on their own. We see the types of content being shared through socialmedia. As consultants , we haunt the halls of industry conferences.

Smaller community banks are finding it beneficial to collaborate with neobanks. Alternative lenders collect data from different sources than traditional banks (such as socialmedia interactions) and continuously update their riskmanagement knowledge base with new sources of data.

This allows us to apply AI to improve risk prediction without creating “black box” models that don’t give riskmanagers, customers and regulators the required insights into why individuals score the way they do. By contrast, FICO analyzes new data sets along five lines to see if they will add value to credit risk scoring.

recently did a study where we looked into how many banks & credit unions were on socialmedia. Designs for the web can easily be translated over to social while informative articles around calculators and information for newsletters can be used for content on social. What if socialmedia is a fad?

No one has been more successful at using socialmedia to generate awareness and a positive image for their bank than Jill (@JillCastilla, @CitizensEdmond). Jill’s use of Twitter is a model for any bank CEO looking to engage on socialmedia. Community bank marketing resources. Information Management Award.

Although community banks did not lend to sub-prime borrowers in any meaningful way, did we participate? In many respects, community banks were caught in the cross-fire through the purchase of those mbs instruments – and subsequent trial through public sentiment. We were concerned about the panic.

We amplified what was happening in Orlando on socialmedia channels such as the FICO blog , FICO’s YouTube channel , LinkedIn livestreaming , Instagram and Twitter , where event goers made #FICOWorld22 such a popular hashtag it appeared on Twitter’s list of global trending topics. TJ holds a B.S. in computer science and a M.S.

Wysh: Emerging player in the wish-list market, innovative features attracting young demographics, growth driven by effective socialmedia use. 9Spokes: Raised $17M for its comprehensive business management platform; increasing partnerships with major banks. SAVVI AI: Raised $5.6M

Facebook, for example, disclosed that an unprecedented data breach in September 2018 exposed the socialmedia accounts of up to 90M users — including login credentials — effectively compromising access to any site that lets users log in with their Facebook account. But the company is not alone. But Facebook is also accountable.

Banks that are looking to enhance their riskmanagement practices should consider incorporating the concept of the velocity of risk into their enterprise-wide riskmanagement practices. Some risks occur slowly; others strike quickly and hard. Optimizing Risk. Luckily, nothing became of it.

Facebook continues to be whipsawed and other major names like Google, Amazon, Netflix, and Microsoft fell in sympathy with their socialmedia favorite. Dorothy has been with Penn Community Bank and its predecessor since November, 2004. Tech stocks added to the volatile environment during the past few months.

According to a recent survey by Gartner, Revenue growth, margin improvement and better riskmanagement are the top three functional objectives, in order, for next year. Improving treasury management services is a strategic imperative for many banks due to its sheer profitability. more next year than compared to 2024.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content