This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

However, in this blog, we will discuss the regulatory landscape surrounding cryptocurrency from an asset manager or fund manager perspective. For those wanting to start their own cryptocurrency fund, it’s important to be well informed about cryptocurrency regulations. Central Bank Digital Currency (CBDC) ).

As noted at the time by the OCC, advances in computing capacity, increased data availability, and improvements in analytical techniques have significantly expanded opportunities for banks to leverage AI for riskmanagement and operational purposes.

The rise of digital banking, cryptocurrency, blockchain, and AI adoption across banking operations will prompt regulatory bodies to implement clearer frameworks and guidelines to ensure stability and consumer protection. Recommended Approach: Navigating constant changes in risk and regulatory environments is crucial for banks in 2025.

Investment schemes : Investment scams lure victims with promises of high returns and little to no risk, only to steal their money. Variations include: Pig butchering scams Scammers build relationships with victims through social media or dating apps, persuading them to invest in cryptocurrency or other financial opportunities.

Speaker: Ryan McInerny, CAMS, FRM, MSBA - Principal, Product Strategy

Cryptocurrency and non-fungible tokens (NFTs) - what are they and why should you care? With 20% of Americans owning cryptocurrencies, speaking "fluent crypto" in the financial sector ensures you are prepared to discuss growth and riskmanagement strategies when the topic arises.

The funding will enable Elliptic to expand across Asia and collaborate with financial institutions for an increased understanding of the cryptocurrency ecosystem. Elliptic, founded in 2013, has become known for cryptocurrency platform tools that help find and block illicit transactions.

With it, financial institutions need to strengthen their compliance to mitigate the risk of running afoul of the law. Certainly, the use and availability of cryptocurrencies is another emerging area that is contending with its own unique set of compliance issues, but it is also one Wingert said appears to be closing gaps in regulation.

To counteract and minimize such risks, the Fed’s Supervisory Letter required that prior to engaging in any crypto-asset-related activity, a supervised banking organization must first ensure such activity is legally permissible and determine whether any filings are required under applicable federal or state laws. Financial risk.

Facebook already has about a dozen people working on blockchain and cryptocurrency. Facebook CEO Mark Zuckerberg has been vocal about his support of cryptocurrency and blockchain, and the potential to use them to “take power from centralized systems and put it back into people’s hands.”.

1) that IdentityMind’s pioneering compliance, riskmanagement and fraud prevention platform has integrated CipherTrace ’s digital currency risk assessment technology. Working together with CipherTrace, we bring transparency, integrity and compliance to the world of virtual currencies.”.

Cryptocurrencyriskmanagement platform TRM Labs announced that it has raised $4.2 Founded in 2018, TRM helps financial institutions across the US, Latin America, Asia and Europe to measure, monitor and mitigate their cryptocurrencyrisk exposure, enabling them to simplify customer due diligence and meet regulatory requirements.

Cross River Bank announced Wednesday that it will use blockchain data company Chainalysis for cryptocurrencycompliance. The $5 billion bank will integrate Chainalysis’ real-time transaction compliance platform, investigations technology and riskmanagement software into its existing crypto build.

cryptocurrency custody services on behalf of customers, including by holding the unique cryptographic keys associated with cryptocurrency.” Through intermediated exchanges of payments, banks facilitate the flow of funds within our economy and serve important financial riskmanagement and other financial needs of bank customers.

During phase one, VASPs will have to demonstrate their compliance with these standards, according to the release. And, Huobi Group expanded its support for cryptocurrency purchases via Visa and Mastercard on Huobi Global , its digital asset exchange, now allowing cardholders to access a seamless fiat-to-crypto gateway.

Learning from history, he referenced the lack of regulatory controls in derivatives and financial engineering before the 2008 financial crisis, and more recently, the unregulated growth of cryptocurrencies leading to the “Crypto Winter” of 2022.

Given the demands of day-to-day duties, however, it can be challenging for BSA officers and other financial crime compliance staff to find time for training and education on fraud and money laundering. A strong culture of compliance should be reflected in MA& plans, and critical areas should be considered. From crypto to cannabis.

Visma Connect recently interviewed Jürgen Krieg, FICO's head of global compliance sales. In this excerpt from that article, Jürgen elaborates on the importance of compliance. . At FICO, I am responsible for planning and implementing growth strategies to develop new markets, and the expansion of our compliance business globally.

Regulators have started 2023 with warnings surrounding investment in crypto for banks RiskManagement Feature Feature3 Blockchain Bitcoin Cryptocurrency Digital ComplianceCompliance/Regulatory.

Elliptic , an AI-enabled cryptocurrency surveillance service provider, has raised $60M in a Series C. UK-based Elliptic captures the blockchain sector’s analytical data to provide anti-money laundering and risk resiliency services to fintech firms, government agencies, and cryptocurrency organizations. Want the full post?

Compliance with market standards and regulations allows us to provide our clients with legal security and convenience of using the exchange, with the participation of a friendly banking system and the availability of payment operators,” BitBay said. As a licensed exchange, BitBay has to follow the market standards.

Australia and Singapore … rolling out Revolut’s banking operations in Europe … strengthening riskmanagement and compliance … multiple new product launches … $580m in new equity … and customer base up around 2.5x!” On July 15, Revolut began offering customers a way to buy cryptocurrency.

Overall, banks, credit unions, and NBFIs should modernize their BSA/AML programs with appropriate risk-based innovative solutions to streamline those processes and use resources efficiently and effectively. 10 NBFI AML Compliance Essentials. According to a 2021 Crypto Crime Report ? Learn More. BSA Rules and Regulation. BSA Training.

Anchorage is not any regular entity overseen by the OCC: it is a cryptocurrency custodian. As we will discuss, the timing of the Consent Order indicates that even when regulators permit crypto activities by financial institutions, they remain cautious, particularly as to BSA/AML compliance.

Develop your risk assessment with the AML/CFT priorities in mind Evaluating each FinCEN priority and addressing them in your financial institution's risk assessment is key to compliance. Institutions should also monitor virtual currency or cryptocurrency transactions for unusual activity. This checklist can help.

Joint s tatement emphasizes understanding a customer’s risk profile for BSA/AML An individualized, risk-based CDD approach is best when it comes to creating your BSA program protocols. You might also like this webinar, "Balancing compliancerisk & reward with high-risk businesses." keep me informed.

Cryptocurrency exchange rates have skyrocketed in the past month. According to a recent report , the total of cryptocurrency related frauds and thefts stands at a staggering $7.69b. At the same time, all top US banks now have customers transacting in cryptocurrency through virtual asset service providers (VASP’s).

The last thing that anyone wants to hear in almost any financial organization is that the people tasked with riskmanagement is feeling less than fully confident about their ability to actually do that job — because they aren’t sure if their data is good.

Technology platforms around cryptocurrency, student loans, or financial education may be cool and cheap. We all say the customer comes first, but our actions around innovation often put cost, compliance, or our present way of doing business first. Banks have limited resources and must carefully choose their projects and priorities.

Both corporates and banks have said Know Your Customer ( KYC ) regulations are their most pressing compliance concerns, with nearly three-quarters of businesses with more than $1 billion in revenues pointing to KYC as their top challenge. Most also said payments management is the most time-consuming process, followed by cash forecasting.

The 2022 clarity promised by the “roadmap” presumably will supersede, once issued, Interpretive Letter #1179, which appears to function as a general stop-gap until the 2022 publications hopefully provide more detail regarding exactly how banks can attain compliance. Federal banking regulators have been busy in this space.

“Over the past few years, the rise of new financial marketplaces, globalized eCommerce, cross-border payments, international remittances, and cryptocurrencies have become significant opportunities for banks,” Caldera wrote in a recent report. Not if you ask Jose Caldera, IdentityMind Global’s VP of Product.

In addition, the Federal Reserve and a host of other regulators have released guidance on not only how to address the opportunities of artificial intelligence in financial crime as well as riskmanagement, but what is expected once they look to apply innovative technologies. Heightened supervision expands the aperture.

This subcategory includes companies enabling the trading, storing, and/ or usage of cryptocurrencies, but excludes companies working on cryptoassets unrelated to financial services (e.g. For example, KNØX Custody (disclosed equity funding of US $6.2M) provides insured cryptoasset and cryptocurrency custody solutions. Capital markets.

The Federal Reserve's top regulator said banks drop customers they see as too risky, and anti-money-laundering actions are "just straight-up-the-middle riskmanagement and banking."

We predict that regulators will continue to emphasize financial crimes compliance by looking to close the gaps in existing frameworks and regulations. So will high-risk products/services such as correspondent banking and trade finance transactions. A number of proposed bills are also with law makers on Capitol Hill.”.

Regulation and Compliance: Not one of the more exciting topics, but there seems to be a growing emphasis on FinTech regulation and compliance, particularly around industry stability and consumer protection. Two years ago, the buzz was all about cryptocurrency and blockchain/DLT. The application of AI was highlighted many times.

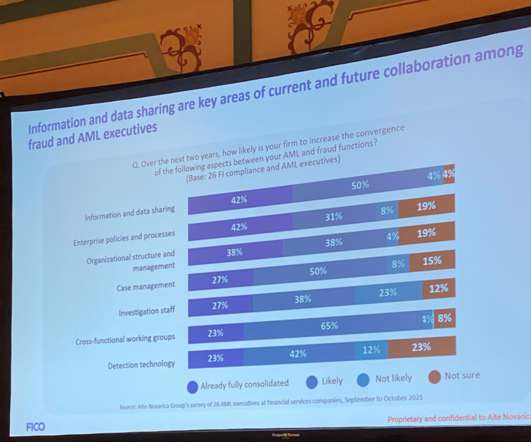

Already, 42% of the respondents (which comprised 26 compliance and AML executives) had some level of info and data sharing between fraud and AML, another 50% said they were likely to do this in next one to two years. Have lunch with your counterpart in fraud or compliance. Go to lunch,” I said. TJ holds a B.S.

While Arizona’s law does not specifically mention blockchain technology, the State’s AG has said “certain blockchain or cryptocurrencies products or services might also be eligible.”. Further, neither Utah nor Arizona may exempt participants from compliance with federal laws and regulations.

Insights from the 2022 Federal Reserve/CSBS survey of community banks. The post One in 10 community banks planning to launch crypto services appeared first on ABA Banking Journal.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content