This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Artificial intelligence (AI) is transforming fraud prevention AI offers financial institutions a way to reduce false positives, detect fraud faster, and improve suspicious activity monitoring. Staying on top of fraud is a full-time job. Let our Advisory Services team help when you need it.

Evaluating the FRAML approach For years, financial institutions have debated the merits of combining fraud and anti-money laundering (AML) functions into a single department in what's known as a FRAML approach. With such heightened scrutiny on fraud, keeping AML and fraud teams siloed may not be sustainable.

Transaction monitoring ensures more than just compliance Without reliable client and transactional data coming into your monitoring system, either manually or automatically, you could miss crucial suspicious activity. Staying on top of fraud is a full-time job. This could put your institution at regulatory and reputational risk.

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence.

How to prevent internal fraud at your bank or credit union Of the many fraud risks banks and credit unions face, one of the most costly comes from within the institution itself. ACFE reported that 5% of an organizations revenue is lost to internal fraud each year, with an estimated $3.1 billion in total losses.

Financial institutions' will focus on these concerns related to AML and fraud Abrigo asked financial institution clients and our Advisory Services team to identify the top issues for 2025. Indeed, examiners are expected to emphasize that financial institutions must develop and maintain a culture of compliance. Heres what they said.

Can your AML/CFT and fraud staff recognize these fraud typologies? The technology used to perpetrate financial crimes may be changing, but these common fraud typologies aren't going anywhere. This is a nearly 10% increase in complaints received and a 22% increase in losses and thats just fraud that was offically reported.

Additionally, the emergence of embedded finance and an increased focus on regulatory compliance are compelling financial institutions to continuously adapt and innovate. The integration of AI is reshaping the landscape by addressing challenges such as data protection, regulatory compliance, and the modernization of legacy systems.

Increasing efficiency of compliant AML investigations To boost AML program productivity and keep pace with evolving compliance demands, financial institutions should focus on strategic operational improvements paired with the smart use of technology. See tailored AML/CFT solutions that can improve your compliance. Learn more 1.

Adhering to Payments Card Industry (PCI) Data Security Standards (DSS) is an unavoidable requirement for any and all eTailers that accept card payments, but a surprising number of firms are not up to speed on these standards. Either way, firms that do not comply with these industry standards risk leaving their customers’ data exposed.

Banks can use advanced data analytics and AI to deliver highly personalized financial services, such as customized savings plans and tailored investment advice. Recommended Approach: Banks should leverage advanced data analytics, artificial intelligence (AI) , and machine learning (ML) to create highly individualized experiences.

The economic risks of AI to the financial systems include everything from the potential for consumer and institutional fraud to algorithmic discrimination and AI-enabled cybersecurity risks. Fraud screening.

The industry faces numerous challenges, including protecting sensitive data, navigating evolving regulations, and outdated legacy systems. This transformation will require a delicate balance between innovation and compliance, ensuring that advancements in AI contribute to a secure and efficient payments landscape.

Microsoft’s Azure Integration Services , a suite of tools designed to seamlessly connect applications, data, and processes, is emerging as a game-changer for the financial services industry. This connectivity enhances interoperability, allowing for streamlined operations and improved data flow across various platforms.

This brings a longstanding challenge to the fore: Healthcare organizations have long struggled with fraud, waste and abuse (FWA), costing the United States healthcare sector more than $200 billion annually by some estimates. Moreover, the benefit cited by the greatest proportion of healthcare firms (65.6

Their contributions are massive, and if you’ve ever worked with AML Officers and fraud professionals, you know just how vital they are. Every day, I’m reminded of the critical role the teams at our 2,500 bank and credit union customers play in anti-money laundering (AML), combating the financing of terrorism (CFT), and fraud prevention.

In the fast-paced realm of finance, the significance of regulatory risk and compliance management practices cannot be overstated. The Role of Regulatory Risk and Compliance 1. Compliance with these legal obligations is not only mandated by regulatory authorities but also necessary for maintaining an institution’s reputation.

With digital transactions and eCommerce soaring during the pandemic, the rate of increasingly sophisticated fraud has also risen. With it, financial institutions need to strengthen their compliance to mitigate the risk of running afoul of the law. Accurate and reliable data is a critical piece of modernizing the AML regimen,” he said.

Share these reports on AML activities to inform directors Reporting to the board on AML and fraudcompliance is an essential obligation. Takeaway 3 Recommended reports on AML and fraud metrics for the board include those on high-risk customers and trends on types of fraud and suspicious activity seen.

Payment system types, trends, and fraud risks Understanding how payment systems function, the different types in use, and the associated risks is critical for financial institutions to be able to balance innovation with security. Need short-term fraud or AML staffing relief? trillion in 2021, according to the latest data from the Fed.

The economic risks of AI to the financial systems include everything from the potential for consumer and institutional fraud to algorithmic discrimination and AI-enabled cybersecurity risks. By continuously improving and adapting over time, AI-driven credit scoring ensures a fairer assessment and broader availability of credit.

According to FinCEN suspicious activity report (SAR) data , over 800 financial institutions have decided yes, at least to banking deposit services for CRBs. Abrigos new fraud detection software for banks and credit unions finds more fraud faster. However, compliance goes beyond software. But what about lending?

AI can eliminate certain processes altogether while maintaining compliance and consistency to provide a better experience for customers and staff. Autonomous agents can retrieve data from an existing customer profile, pull credit, and generate scores for the customers cash flow and business risk.

As data privacy becomes enshrined in international law, regulatory compliance will grow more stringent and costly to companies that fail to provide the digital defenses these laws demand. Gateways To Success And Data Vaulting. Data vaults play an increasingly important role in that sequence.

Mari Anne Bayliss , senior director of solution management at CyberSource , told Karen Webster that simply relying on machine learning as a weapon against fraud is not enough — not in an age where managing fraud risk during the great digital shift (and unprecedented transaction volumes) is so challenging. . Human Touch .

Avalara , a tax compliance software firm with a focus on the business sector, said on Tuesday (Dec. Avalara’s acquisition of INPOSIA Solutions is expected to enhance its offerings, with the German software company focused on “e-invoicing, digital tax reporting, and business and data integration,” the companies said.

With third-party due diligence and supply chain security as increasingly critical components of organizations’ procurement operations, compliance executives are finding important positions in their firms’ purchasing processes. That’s only if analysis of that data can be done correctly, however.

Combating Cyber-Enabled Fraud Requires Communication Increases in cybercrime or cyber-enabled fraud deserve attention from financial institutions, as Abrigo expert Terri Luttrell explains in this video. . You might also like this whitepaper, "The 2021 BSA/AML and Fraud Staff Survey: Top Issues for FinCrime Fighters".

Artificial intelligence, machine learning, and compliance were some of the topics that dominated day 1 of fintech conference Data Disrupt, taking place in New York. The panel “Consumer Finance: Fighting Fraud with Fire” brought together three fintech companies, who discussed different methods of combating fraud.

The most popular financial crime blogs in 2023 Check fraud, the SAFER Banking Act, and BSA exam topics were among Abrigo's top blogs on AML/CFT and fraud this year. You might also like this infographic on the true costs of fraud at financial institutions. Here are Abrigo’s 10 top AML and fraud blogs in 2023.

Popular use cases include request for payments using the instant payment rails (above), loan payments and transaction verification to prevent fraud. Banks must ensure robust security measures are in place to protect customer data. Fraud alerts and verification: RCS transforms scam warnings from scary notifications to helpful heroes.

Banks in the EU have been racing to comply with the General Data Protection Regulation ( GDPR ) and the revised Payment Services Directive ( PSD2 ) since both measures were enacted in 2018. He explained that the cloud can help FIs swiftly respond to compliance and security challenges during the pandemic. Security Takes Center Stage.

The capabilities to unlock bank data and integrate new services into emerging FinTech platforms via API integrations is a FinTech trend that hasn’t ignored the B2B payments arena. However, B2B payments are not the same as B2C, largely thanks to high transaction sizes and volumes, as well as expanding fraud risks. With the U.K.

Prevent fraud when adopting FedNow Credit unions can prevent fraud as they connect to FedNow. Use this guide to understand available tools and the steps AML and fraud teams should take. You might also like this FedNow implementation guide with details on appropriate AML/CFT and fraud considerations.

Fraud on Alert for 2022 A review of SAR data , government agenc y releases, a nd fraud findings found these f raud c oncerns and trends to wat ch in 2022. Takeaway 1 An Abrigo review of SAR data, government agency releases, and fraud findings revealed fraud trends to watch for. Fraud Concerns.

What NBFIs Should Know About Their AML Programs NBFI AML compliance requirements are top of mind in today's regulatory environment. NBFIs’ AML compliance requirements. But what about the NBFI compliance factor, particularly Bank Secrecy Act and anti-money laundering (BSA/AML) compliance? DOWNLOAD .

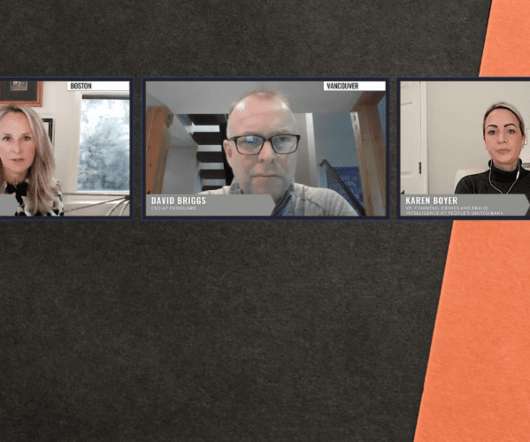

But as GeoGuard CEO David Briggs and People’s United Bank VP of Financial Crimes and Fraud Intelligence Karen Boyer told Karen Webster, realizing the full benefits of using geolocation will take a bit of education – for consumers, yes, but also for banks. Not all data are created equal, of course.

Court case: Credit union held liable for ACH fraud losses A construction company argued the financial institution "failed to establish a reasonable routine" for monitoring suspicious activity alerts tied to ACH. Takeaway 3 Remember that ACH fraud risk also occurs in the placement stage of a fraudulent or money laundering scheme.

Financial services providers that slack on regulatory compliance and fail to safeguard their operations against money laundering, terrorist financing and other criminal activities may face damaged reputations and significant fines. A team of analysts can only handle so many potential fraud cases at a time, after all. . resources.

Keeping customers' digital payment data safe and secure is a critical part of doing business in the digital economy, and following Payment Card Industry (PCI) compliance guidelines is an effective way for firms to accomplish this. Getting Up to Speed on Compliance. This can be particularly burdensome for smaller firms.

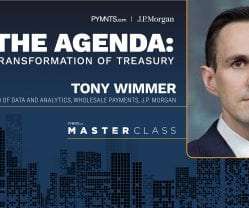

As merchants accelerate their digitization roadmaps, the volume of data they’re able to work with increases. But data in payment transactions provides an often-untapped opportunity for merchants to optimize their payment operations and grow their businesses, Tony Wimmer , head of data analytics for J.P. Growing Your Business.

Measuring the cost of fraud losses. The true cost of fraud goes beyond the initial reported fraud losses Would you like other articles like this in your inbox? Takeaway 1 Fraud scams made worse by the pandemic continue to be successful, while crypto-scams are emerging. That equates to $35 billion annually.

A significant portion of consumers in various global markets are even planning to increase their use of digital banking services in the coming months, which means banks are going to need to seamlessly support a new flood of digital consumers’ requests, as well as the data that comes with them. Around The Cloud Banking World.

Retailers must protect customers’ card data from hackers who try to snatch payment details, and following best practices to ensure security requires adhering to the regulations established by the PCI SSC, a global payments industry forum. Compliance Complexities. Compliance Complexities.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content