This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Look for folks who: Actually understand the data (a rare breed, cherish them) Can handle details without going cross-eyed Won’t melt down when stuck between the rock of compliance and the hard place of IT Bonus: Give them a fancy title like “Data Integrity Czar.” So very, very wrong.

For those wanting to start their own cryptocurrency fund, it’s important to be well informed about cryptocurrency regulations. Regulatory cryptocurrency regulations are most fluid at the state level. State Regulations. SEC Regulation. Central Bank Digital Currency (CBDC) ).

What NBFIs Should Know About Their AML Programs NBFI AML compliance requirements are top of mind in today's regulatory environment. Takeaway 2 NBFIs should ensure their AML programs are sound and pass the scrutiny of FinCEN and their primary regulators. NBFIs’ AML compliance requirements. DOWNLOAD . Competing with Banks.

The investment advisers rule expands the definition of "financial institution" under the Bank Secrecy Act (BSA) to include certain registered investment advisers and exempt reporting advisers. This includes monitoring their activities, understanding their client base, and ensuring they adhere to the same standards as other regulated entities.

and compliance teams would manually check onboarding customers to make sure their records were clear. Wiping out the manual process and handling compliance in an automated fashion can propel companies forward,” Meier said. A client who passed through compliance checks on day one might not be compliant on day 500, for example.

The secret to understanding timing and creating truly impactful communications hinges on a deeper understanding of HIPAA’s definition of marketing. HIPAA may seem like a minefield of regulations, best avoided altogether. It’s not just knowing what you aren’t allowed to do, but more importantly what is allowed.

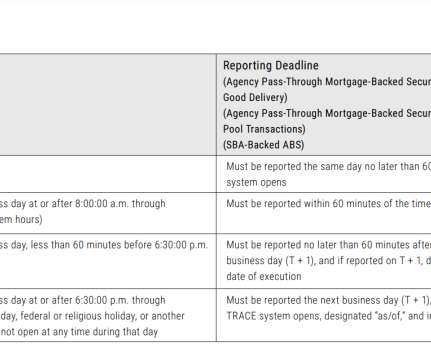

Note that the definition of treasuries for this reporting and regulations example does include principal-only (PO) and interest only (IO) Separate Trading of Registered Interest and Principal Securities (STRIPS). The following tables, starting with the most basic – U.S. Interested in learning more? You can download it here.

In short, the definition ties in with “some type of crime relating to trust.”. Compliance is also becoming an enterprise-wide endeavor, and compliance officers must adopt a global mindset. The roster of players here can extend across the organization from both insiders and external culprits, she continued.

The Federal Reserve Board, the Federal Deposit Insurance Corporation (FDIC), FinCEN , the OCC and the Conference of State Bank Supervisors participated in issuing the definitions and guidelines. It was amended to include the Patriot Act, which requires every bank to adopt a customer identification program.

While deregulation has been a trend over the past few years, compliance monitoring and regulatory change management remains a top focus for financial institutions of all sizes. Greater availability of data, facilitated by real-time integrations makes it possible for compliance experts to monitor a wide variety of sources.

In the world of supply chain compliance, complex regulatory requirements like Know Your Customer (KYC) and anti-money laundering (AML) probably come to mind. There are also the challenges of supplier management, tax legislation, cross-border compliance, worker protection and more.

Treasury’s Financial Crimes Enforcement Network (FinCEN) recently issued a new regulation on the requirements, including how AML staff will access the information through a new federal beneficial ownership information (BOI) registry. This definition is different from existing customer due diligence (CDD) rules that took effect in 2018.

Following on from my previous blog introducing the new year in the Fintech Innovation programme, I wanted to turn the focus onto the emergence of RegTech—technologies that address the challenge and cost of regulatory compliance. RegTech has two aims: increasing the effectiveness and the efficiency of compliance. Both are critical.

Following on from my previous blog introducing the new year in the Fintech Innovation programme, I wanted to turn the focus onto the emergence of RegTech—technologies that address the challenge and cost of regulatory compliance. RegTech has two aims: increasing the effectiveness and the efficiency of compliance. Both are critical.

The regulations will also hit Alibaba’s Ant Group, which took a beating last week after the government suspended its planned initial public offering (IPO). For example, the definition of “relative market” means that companies in a “dominant position” if they control more than 50 percent of the market would come under the new regulations.

Takeaway 2 The change includes an obligation to inform regulators of a “notification incident” ASAP and no later than 36 hours after a reportable event occurs. In this guest column by Jeffrey Taft and Matthew Bisanz of Mayer Brown 's Financial Services Regulatory & Enforcement practice, learn more about how to be ready for compliance.

Definitions, clarifications and other non-obligation material make up 65% of the information in regulations. That means banks and other regulated industries — and more specifically, their lawyers — spend hours combing through information in search of actionable items, according to […].

While the delinquency numbers are favorable at this point for the bank lenders as compared to CMBS, if you look in their portfolios, there are some markets that are heavily criticized, and those loans, by definition, at some level will convert to delinquency, he said.

Payments is already a highly regulated and complex space, but when it comes to moving money for Global Citizens , the rules that govern these kinds of payments are well beyond just the basics. If there are licenses required, Butterfield suggested investing in practical legal advice and potentially working with locally situated regulators.

His definition of RegTech is automating highly manual processes or high-cost centers to achieve a new level of scale, but this definition can mean different things depending on the business itself. It’s no question that compliance is now a massive line item on the balance sheet of bigger banks. Raising The RegTech Bar.

The foreseeable changes stem from the already delayed strong customer authentication (SCA) regulations that are due to go into effect in Europe by the end of the year. Barclays Transact aims to help merchants make online transactions simpler, safer and compliant with the upcoming SCA regulations. card transactions.

In addition, Guo noted that many of the businesses that started as part of Dianrong’s expansion have now become “heavy burdens with unbearable high costs” due to the regulations. We hope regulators can give the industry a clear and definite timetable, and give guidance and a ray of hope for companies that stick to compliance,” Guo said.

Definition of LOS. Compliance. Another factor to consider in the “build vs. buy” argument is that any loan origination system must comply with current regulations and industry standards. Some third-party vendors are regulated by the Federal Financial Institutions Examinations Council (FFIEC). Credit Risk Regulation.

According to Brad Fauss, president and CEO of the Network Branded Prepaid Card Association, the recently released regulations on prepaid cards from the Consumer Finance Protection Board could be another instance of good intentions gone wrong. The updated regulations are slated to take effect Oct.

But compliance deadlines are tiered. June 28, 2023, based on the Code of Federal Regulations and the March 30 publication). However, compliance deadlines for affected financial institutions are tiered so that small business lenders originating the most transactions begin reporting data earlier than less active small business lenders.

PCI compliance is vitally important for businesses that process credit cards. That’s why utilizing tokenization to eliminate the need to store sensitive data in the first place can reduce scope and simplify compliance, said John Noltensmeyer, TokenEx’s Head of Global Privacy and Compliance Solutions.

The ministry said that policymakers have to consider the basis for new regulations that mirror the evolving nature of economic activity in the digital era. The ministry acknowledged in its report that there is not a single definition that can describe the sharing economy. Comments will be accepted through March 3, 2021.

Keep leadership informed on AML/CFT trends to ensure a strong culture of compliance at your financial institution. Introduction Corporate Transparency Act guidance FinCrime professionals have been on high alert for new regulations since the Anti-Money Laundering Act of 2020 (AMLA) was signed into law, but updates have been slow to arrive.

On February 7, 2020, the California Attorney General’s (AG) Office released modifications to the proposed regulations to the California Consumer Privacy Act (CCPA). The modifications incorporate amendments to the CCPA signed into law after the AG’s Office issued the proposed regulations in October 2019. Removal of Webform Requirement.

According to some studies, as many as 30,000 to 40,000 regulatory changes can occur in a given year, and they are projected to culminate into 300,000,000 pages of regulation by the end of 2020. Given these issues, it is critical that governance, risk and compliance (GRC) systems are leveraged to enhance this process.

Anti-Money Laundering Act of 2020 BSA professionals should prepare for changes as new regulations and guidance from FinCEN unfold. Takeaway 2 While the AMLA is now law, regulations, guidance, and other information still needs to be written. These include conducting studies, writing regulations, and publishing guidance.

But the banks themselves also have complex demands for their own treasury departments, which, like other corporations, must be able to manage finances, risk and compliance. Compliance with domestic and international standards is considered a must,” Beaulande recently told PYMNTS.

The definition of who is considered a beneficial owner is expanded. BSA Rules and Regulation. AML Compliance and Sanctions Requirements for Non-Bank Financial Institutions. BSA Rules and Regulation. BSA Rules and Regulation. 10 NBFI AML Compliance Essentials. Who is a Beneficial Owner? Keep Me Informed.

CDD requirements are risk-based and require the grower to provide their compliance with licensing requirements. BSA Rules and Regulation. SARs should only be filed if suspicious activity is detected beyond legal hemp growing. . In fact, the guidance should give financial institutions confidence to bank hemp-related businesses.

Takeaway 1 BSA and fraud functions have historically been siloed, and IT has been external to compliance. Bank Secrecy Act (BSA) and fraud functions have historically been siloed within financial institutions' structures in the compliance world. Similarly, IT security professionals generally do not have a compliance background.

The most common is known as a trade-based money laundering (TBML) scheme. FICO explains: “In its simplest definition, TBML is the process of disguising the proceeds of crime and moving value (i.e., Financial institutions can expect additional scrutiny from regulators and auditors on EDD processes and high-risk customer monitoring.

Businesses depend on the public services tax revenues pay for: roads that facilitate deliveries, courts where firms resolve legal disputes and regulators that help protect businesses from fraud. Wayfair ruling have made tax compliance challenges highly visible. Wayfair ruling have made tax compliance challenges highly visible.

On April 1, 2021, the FDIC’s final rule issued in December 2020 revising its brokered deposits regulation became effective. The full compliance date for the final rule is January 1, 2022.

Cohen described the numbers tied to ill-gotten gains as “eye-opening and [likely to] raise flags for the regulators. The more comprehensive such efforts are at the enterprise level, the executive said, the odds increase rapidly that they will be well-aligned with different regions, organizations or even regulators. The Crypto Factor.

A small business (SMB) in Massachusetts borrowing funds via marketplace lender Kabbage has sued the platform, igniting new debate in the conversation over the definition of a “true lender,” according to reports in the National Law Review on Tuesday (Oct. Usury laws regulate how much interest can be charged on a loan.

The CFPB recently issued a final rule that amends the Regulation Z ability to repay/qualified mortgage rule by extending the sunset date for the qualified mortgage (QM) based on a loan meeting certain product requirements and being eligible for sale to Fannie Mae or Freddie Mac. The QM often is referred to as the “GSE Patch.”

Last April, the FDIC released an Interagency Statement titled Model Risk Management (MRM) for Bank Models and Systems Supporting BSA/AML Compliance. What regulators look for in top-down guidance. BSA Rules and Regulation. BSA Rules and Regulation. BSA Rules and Regulation. Model Risk Management in the spotlight.

Regulators are also looking more closely at the authentication measures attached to online payments as they continue to jump in volume, meaning merchants must keep pace with new compliance requirements as well as shifting consumer perceptions. Merchants, their payment providers and their regulators must keep up. under the GDPR.

Compliance with the new disclosure requirements is not required until the DFPI’s final regulations become effective. The most significant changes in the fourth modifications concern the definitions of “Average monthly cost” and “Estimated monthly cost,” items which must be included in the disclosures for certain products.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content