This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Document and be able to defend qualitative factors under CECL Financial institutions need to be able to explain and show how they developed Q factors for their allowance for credit losses. But documenting and defending Q factors doesnt have to be a guessing game. Why is documenting Q factors so important?

Banks are full of documents. Each document contains an extensive array of data. Then there are vendor contracts, employment agreements, statements of work, loan documents, financial statements, tax returns, deposit account documents, policies, and an array of similar applications.

Every company needs documents for its processes, information, contracts, proposals, quotes, reports, non-disclosure agreements, service agreements, and for various other purposes. Document creation and management is a crucial part of their operations. What is Industries Document Generation? How to generate documents?

Learn the ins and outs of Regulation E Even if youre not in the banking industry, you've likely heard the term Regulation E compliance (Reg E). This blog will break down what Reg E compliance entails, the basics of the Electronic Fund Transfer Act (EFTA) , and the potential consequences for financial institutions that fail to comply.

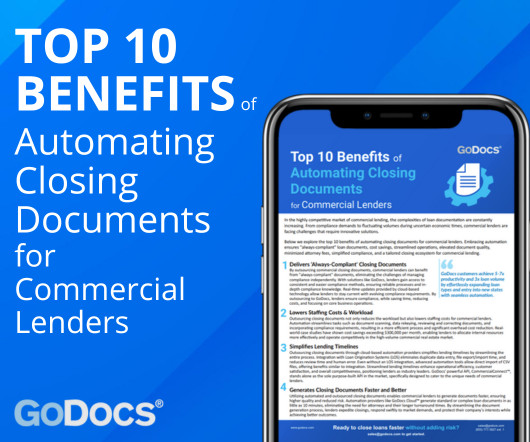

In the fiercely competitive landscape of commercial lending, where FinTech's digital transformation initiatives take center stage, the complexities of loan documentation are constantly evolving. Innovative solutions are now essential to navigate this dynamic landscape and achieve success in the fast-paced world of commercial lending.

Banks are full of documents. Each document contains an extensive array of data. Then there are vendor contracts, employment agreements, statements of work, loan documents, financial statements, tax returns, deposit account documents, policies, and an array of similar applications.

Look for folks who: Actually understand the data (a rare breed, cherish them) Can handle details without going cross-eyed Won’t melt down when stuck between the rock of compliance and the hard place of IT Bonus: Give them a fancy title like “Data Integrity Czar.” So very, very wrong.

With ServiceNow your company could achieve accelerated development, greater speed to market, and increased team execution and delivery for Financial Institutions while adhering to compliance and risks. This includes onboarding customers, assets, and products, and issuing approvals for documents.

As a best-practice it is recommended to adopt automation of certain security audits, integration of compliance oversight into key development process areas (e.g. In most organizations, this separation is enforced by having a centralized security/compliance team that works in close relationship with the development teams.

Discover the key benefits of portfolio loans and learn how to streamline your lending process with our infographic, "5 Things Lenders Need to Know About Portfolio Loans & Their Documentation." Learn how innovative technology can automate portfolio loan documentation, ensuring efficiency and compliance.

Lets talk about data governance in banking and financial services, one area I have loved working in and in various areas of it … where data isn’t just data, numbers aren’t just numbers … They’re sacred artifacts that need to be protected, documented, and, of course, regulated within an inch of their lives.

Increasing efficiency of compliant AML investigations To boost AML program productivity and keep pace with evolving compliance demands, financial institutions should focus on strategic operational improvements paired with the smart use of technology. See tailored AML/CFT solutions that can improve your compliance. Learn more 1.

Compliance is at the center of the lending process at financial institutions. Without the right tools and processes in place, however, compliance can be monotonous and inefficient. Financial institutions are looking for a solution to increase efficiency, decrease risk, and provide complete, defensible documentation for loan types.

The work being done in compliance departments across banks and credit unions is about more than just meeting regulatory requirementsits about protecting communities and stopping criminals in their tracks. Advanced technology is helping financial institutions detect patterns faster, reduce false positives, and improve SAR accuracy.

Automated tools are making it possible to keep up with demand while also ensuring compliance, but it is important to remember that not all solution providers are created equal.

The AI-driven solution enables loan review teams to complete assessments in seconds, ensuring that documentation is accurate and that potential risks are flagged early. These tools are built with data encryption, robust access controls, and compliance baked in from the start. Data security is also a major concern.

Each step of back-end loan processingfinancial spreading, risk assessment, document gatheringrequires significant effort just to make incremental progress. Risk rating Manually assigning a risk rating to each application can involve subjectivity, and documenting decisions can be time-consuming. The results?

Already reviewed by Perficient, BES provides a secure and efficient portal to exchange documents, information, and communications for consumer compliance and Community Reinvestment Act (CRA) examinations. The documents were generally minimally encrypted and therefore tended to contain non-confidential information.

The Comment stresses that the use of fraud screening tools, such as those offered by third-party vendors that generate fraud risk services, must be offered in compliance with ECOA and the CFPA. Fraud screening.

From documentation requirements to the implications of non-compliance, learn how to safeguard your lending position and prioritize legal adherence. Plus, discover how GoDocs' automated solutions can ensure compliance, efficiency, and peace of mind for lenders venturing into New York's lucrative real estate landscape.

Transaction monitoring ensures more than just compliance Without reliable client and transactional data coming into your monitoring system, either manually or automatically, you could miss crucial suspicious activity. Maintain compliance with anti-money laundering (AML) regulations. What is transaction monitoring?

There are a few reasons why a B2B program may not be understandable, as follows: Documentation: The standard B2B program requires lengthy (45 to 60 pages), multiple, and cumbersome agreements. No line lender wants to explain ISDA documents to the average client. The formula to a successful B2B program is to hold the expertise inhouse.

A strong BSA prog r am starts with FFIEC compliance Building a robust BSA program means having access to the staffing and resources you need. You might also like this podcast, "Ensuring access to the FFIEC’s suitable resources at your financial institution: What BSA compliance officers need to know.

AI can eliminate certain processes altogether while maintaining compliance and consistency to provide a better experience for customers and staff. It then offers to initiate an online application, outlining the required documents and information. Identify all roles, actions, and systems used in each process.

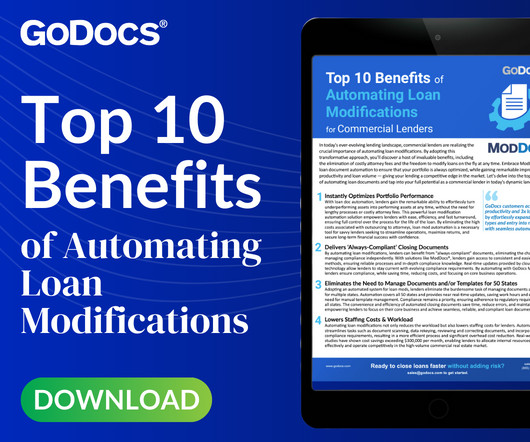

But with ModDocs®, you can enjoy an innovative solution that eliminates attorney fees, allows on-the-fly loan modifications, and ensures compliance. Learn how to generate compliant closing documents in minutes, streamline operations, and reduce risks.

Social distancing restrictions implemented to curb the virus’s spread are preventing compliance professionals from obtaining physical identification documents and holding in-person meetings that typically enforced anti-money laundering/know your customer (AML/KYC) compliance. Compliance Enforcement Goes Remote With Biometrics.

Exterro is a leading software platform focusing on an area known as Legal GRC (Legal Governance, Risk, and Compliance). Exterro helps our clients with three big e-discovery components: Locating the electronic documents. Collecting and preserving the documents and present them to the demanding party.

Reducing fees for remittances might push price points low enough that more consumers could resume sending money home, though, and some researchers believe that money transfer service providers could make such price adjustments if they are able to reduce their own expenses through more robust and cost-effective regulatory compliance measures. .

Even with strong compliance programs, theres always the potential for scrutiny from regulators. For financial institutions, this means investing in the right anti-money laundering/combating the financing of terrorism (AML/CFT) software to monitor transactions, flag suspicious activities, and ensure compliance with AML/CFT requirements.

Trulioo , the Canadian company that provides online identity verification, has introduced a facial recognition and document validation technology it says will enable small and medium-sized businesses (SMBs) to provide the same level of online protection to their customers as global conglomerates. Trulioo said it’s easy to use.

However, compliance departments are frequently understaffed. How would your institution manage this additional workload while maintaining compliance with daily deadlines? Taking a vacation is often a well-deserved break, but for financial crime professionals, it can trigger significant stress.

Updated AML/CFT programs: If their financial institution is involved in any part of the covered transaction, such as providing escrow services, AML/CFT professionals must ensure that real estate professionals and advisers are fully integrated into their institution’s compliance framework.

Teaching staff these KYC tips to make clients feel more comfortable In 2023, KYC procedures must both support CDD compliance and make sure your institution is a welcoming place for all customers. You might also like this resource, "Customer due diligence checklist." Miss” and thus alienating nonbinary customers.

“In this industry, borrowers and lenders have high expectations; they want a mortgage document processing solution catered to improving operational efficiency, while ensuring speed and data accuracy. They also want a document automation process that helps enhance their current security and compliance posture,” she explained.

Banks must document their CECL transition process thoroughly to satisfy auditors and regulators. Simply folding the acquired banks portfolio into the existing CECL model without justification can lead to compliance issues. "This is something often overlooked but critically important."

By having an inaccessible site, you are turning away 26% of your overall potential market and expose the organization to compliance violations. Identifying and documenting accessibility requirements prior to development hand-off will significantly reduce the number of accessibility errors on a live page. Heading Structure.

Understanding AML compliance and regulatory expectations. AML compliance is not for the faint of heart. Takeaway 3 Be your champion and fight for whatever is necessary to instill a culture of compliance. A culture of compliance AML compliance Having a solid culture of compliance is critical to avoiding AML penalties.

The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party risk management and a compliance vendor management program. This documents how critical and important vendors perform compared to their contractually obligated promises of system uptime, ticket response time and ticket resolution time.

Here are key strategies to mitigate internal fraud risks: Set the right tone at the top Leadership should communicate a strong culture of compliance and a zero-tolerance policy for fraud. Regular audits ensure compliance and identify potential vulnerabilities.

There are also many gray areas in banking compliance, which can lead to different interpretations among compliance professionals. By reaching out to your examiners for compliance guidance, you are establishing a trusted relationship between the regulatory agency and the institution.

On April 28, 2022 the New York Department of Financial Services (“NYDFS”) issued its Guidance on Use of Blockchain Analytics , a document directed to all virtual currency business entities that either have a NYDFS Bitlicense or are chartered as a limited purpose trust company under the New York Banking Law.

For organizations using Teams Calling, it is recommended to start notifying your users about this new capability and update your training and documentation accordingly. Well, if you’d like to manage this capability you can do so by enabling or disabling this add-in for individual users via PowerShell (documentation coming soon).

New compliance standards from SWIFT now require internal SWIFT domain expertise with annual certifications and annual documentation. Businesses need the flexibility to define new banking relationships without the large, inflated IT projects. ”

A starting point to conducting identity verification is document-based, he said. In that event, “the first part of the whole equation is making sure that identity document is authentic,” Patel said. Traditionally, that begins with an individual presenting a government-issued ID to confirm identity. Boots on the Ground .

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content