This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Increasing efficiency of compliant AML investigations To boost AML program productivity and keep pace with evolving compliance demands, financial institutions should focus on strategic operational improvements paired with the smart use of technology. See tailored AML/CFT solutions that can improve your compliance. Learn more 1.

This month, the Federal Deposit Insurance Corporation (FDIC) launches it new Banker Engagement Site (BES) through FDIC connect. Already reviewed by Perficient, BES provides a secure and efficient portal to exchange documents, information, and communications for consumer compliance and Community Reinvestment Act (CRA) examinations.

The agreement, issued last week, addresses “shortcomings” in Discover Bank’s compliancemanagement system for consumer protection laws, the company said.

The guidance is aimed at helping banks address the operational, compliance and strategic risks of third-party tie-ups, such as those with fintech firms.

The most recent FDIC Small Business Lending Survey found that slightly more than half of large banks (those with at least $10 billion in assets) can approve a small and simple loan in one business day or less, compared with only 29% of small banks (those with less than $10 billion). The results?

The FDIC released a manual on Formal and Informal Enforcement Actions. The FDIC released its manual on Formal and Informal Enforcement Actions. For the first time, the FDIC released its manual on Formal and Informal Enforcement Actions to provide greater transparency to those processes. Key Takeaways.

Vendor management is risky business. The FDIC issued a consent order against Discover Bank last year for lacking oversight into third-party risk management and a compliance vendor management program. Does a relationship manager check in regularly with the institution—and not a month or two before renewal?

Brex , the San Francisco financial technology startup, is offering FDIC insurance on its no-fee cash management account, the company announced Wednesday (July 22). The new feature in Brex Cash allows customers the choice to hold cash savings with FDIC insurance, or invest in Money Market Funds.

Perficient provides risk management to more than 500 financial services organizations, many of whom have multiple bank regulators. Often an organization will have a state-charted non-member bank, which has the FDIC as its primary federal regulator. Introduction It’s not you. It’s the guidance.

Meet Model Risk Management Expectations Updates to the FDIC Risk Management Manual should steer institutions toward a model that manages risk and drives growth. Takeaway 1 Aside from meeting examiner expectations, proper model risk management can protect your institution from unnecessary risk. . FDIC Update.

Financial institutions are responsible for not only facilitating payments but also managing risksincluding fraud, compliance, and operational challenges. Federal Reserve Manages ACH, FedNow, and interbank payments. Reduce loss and protect your customers with our sophisticated detection and fraud management software.

The FDIC is offering a fresh take on how a bank’s board of directors should understand and manage risk. The regulator’s April edition of Supervisory Insights provides what the FDIC called a “refresher” on its Pocket Guide for Directors, the 1988 booklet outlining the basic duties and responsibilities of a bank’s board of directors.

Instead, financial institutions should focus on managing risk through better loan decisioning models. Reduce approval layers According to the FDIC, 73% of banks have at least three levels of approval for small business loans. While its true that nearly half of small businesses fail within five years, risk avoidance isnt the solution.

Navigating interest rate management in today's environment As regulators focus on interest rate risk management, read about what financial institutions can do to be ready for a rate drop. You might also like this on-demand webinar, "Navigating uncertain times: Strategies for effective risk management and compliance."

According to a recent survey by the American Bankers Association (ABA), more than 46 percent of respondents had to reduce offerings for loan or deposit accounts, or other services, at their bank because of regulatory compliance burdens. The news isn’t all bad for community banks, though.

OCC, Board, FDIC will require banks to report incidents within 36 hours ComplianceComplianceManagementCompliance/Regulatory Cyberfraud/ID Theft Security Mobile Online Core Systems Risk Management Technology Feature Feature3.

The FDIC has announced that it has entered into a settlement of the lawsuit filed against it and the OCC in 2014 by a trade group and several payday lenders challenging “Operation Choke Point” — a federal enforcement initiative involving the FDIC, OCC and other federal agencies. In July 2017, the D.C.

Manage third-party risks, especially for relationships involving higher-risk or critical activities. Once published by regulators, Perficient’s Risk and Regulatory CoE will be here to walk our clients through the changes.

The five federal agencies are: the Consumer Financial Protection Bureau (CFPB), the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve Board (Fed), the National Credit Union Administration (NCUA) and the. Risk Management. AI may be used to augment risk management and control practices. Credit Decisions.

FDIC) and the Treasury Department are looking to see if American Express Co. A representative for AmEx told WSJ, “We have robust compliance policies and controls in place, and do not tolerate misconduct.” Representatives of the Fed, FDIC and Treasury inspectors general offices would not comment on the matter, the paper reported.

Seeking additional arrows in their quiver against large bank failures, on October 14, 2022, the Federal Reserve Board (FRB) and Federal Deposit Insurance Corporation (FDIC) published an Advance Notice of Proposed Rulemaking (ANPR). Both the FRB and FDIC will accept comments and answers for 60 days after publication in the Federal Register.

The Federal Financial Institutions Examination Council (FFIEC), whose members include the CFPB, has finalized guidance setting forth a revised uniform interagency consumer compliance rating system (CCRS). The revisions reflect changes in consumer compliance supervision since the current rating system was adopted in 1980.

Public’s input sought on potential modernization of advertising and signage rules to better reflect how banks operate Compliance Retail Banking Customers Performance People ComplianceManagementCompliance/Regulatory Consumer Compliance Feature3 Feature Financial Research Duties Financial Trends.

OCC, Federal Reserve, CFPB, FDIC, and NCUA are seeking input from banks and other stakeholders ComplianceComplianceManagementCompliance/Regulatory Cyberfraud/ID Theft AML & Fraud BSA/AML Security Feature3 Feature Duties Technology.

With Paxos Crypto Brokerage, companies can leverage our expertise and regulatory compliance to easily and securely integrate crypto into their applications. while enabling Revolut to control “the user experience” and manage its “customer relationships.” Paxos will hold crypto assets for Revolut’s users in the U.S.,

Account for the details before your FDIC bank acquisition Consider these tips for assessing your institution and a to-be-acquired institution for a smooth integration You might also like this webinar, "Valuation and purchase accounting: Navigating the changing M&A landscape."

Shown below is the 56% increase in FDIC and state bank regulator assessment charges. In the rising interest rate environment, management had invested like an S&L executive of the 1980s and had a similar outcome. This may be of value to regulators and the management of financial institutions going forward.

In various press releases, the Federal Deposit Insurance Corporation (FDIC) has highlighted that an estimated $16.3 billion of the total cost incurred from the failures of Silicon Valley Bank (SVB) and Signature Bank was designated for safeguarding uninsured depositors. Commencing with the first quarterly assessment period of 2024 (i.e.,

According to the Federal Deposit Insurance Corporation (FDIC), in 2000, there were 8,000 commercial banks in the United States, but as of March 2022, that number had dwindled to 4,194 operating physical bank branches.

A rather small bank, as of the end of its first quarter, the bank reported $139 million in total assets and $130 million in total deposits in its FDIC Call Report. Mr. Herndon named the Federal Deposit Insurance Corporation (“FDIC”) as receiver, allowing the FDIC to take control of the Heartland Tri-State’s operations.

This is particularly true for community banks preparing to undergo their next regulatory safety and soundness or compliance examination. As David Barr, spokesperson for the FDIC, points out, “a vast majority of community banks remain well-rated and exhibit satisfactory corporate governance programs and compliancemanagement systems.”.

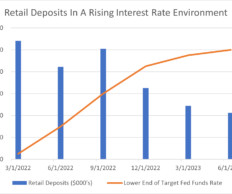

In our previous article, “ Transaction Accounts: Analyzing Deposit Stickiness in the Current Interest Rate Environment ,” Perficient’s Financial Services Risk Management and Regulatory Capabilities Center of Excellence (CoE) explored the sharp decline in transaction account balances over an 18-month period. Contact us today!

Resolution plans for the top eight US banks have been assessed by the Fed and the FDICCompliance Duties ComplianceManagementCompliance/Regulatory Feature3 Feature Big Data Digital.

The FDIC has issued an “Advisory to FDIC-insured institutions Regarding Deposit Insurance and Dealings with Crypto Companies ” to address the agency’s concerns regarding misrepresentations about FDIC deposit insurance by certain crypto companies. The FDIC identifies two issues that can create customer confusion.

The FDIC approved a final rule to increase initial base deposit insurance assessment rates by 2 basis points until the Deposit Insurance Fund (DIF) achieves the FDIC’s long-term goal of a reserve ratio of 2% of insured deposits. The FDIC’s long-term goal for the reserve ratio of insured deposits. Source: FDIC.

The FDIC has issued the March 2022 edition of Consumer Compliance Supervisory Highlights which includes a description of some of the most significant consumer compliance issues identified by FDIC examiners during consumer compliance examinations conducted in 2021. Fair lending.

This being the first blog post in a series of blogs by Perficient’s Financial Services Risk Management and Regulatory Capabilities Center of Excellence (CoE), we will be investigating the deposit structures of non-client banks over time. The challenge lies in gauging how rising interest rates act as an external force on these dormant funds.

WATCH Takeaway 1 Loan review officers must figure out how to adhere to the FDIC’s guidance on loan review and credit risk review systems. Takeaway 2 Examining the following objectives and evaluating your loan review system based on them can ensure regulatory compliance.

The GAO acknowledged that community banks, credit unions and their professional industry associations reported increased compliance burdens and reduced activity in specific business activities, such as certain mortgage lending, as a result of Dodd-Frank.

Last week, the FDIC published its Consumer Compliance Supervisory Highlights that provides observations about its consumer compliance supervision activities in 2018. The FDIC’s anonymized exam findings include: Overdraft Programs. Real Estate Settlement Procedures Act (“RESPA”) Section 8 Violations.

On October 17, the FDIC released revised interagency Military Lending Act (MLA) examination procedures for use in connection with consumer credit transactions occurring on or after October 3, 2016. The FDIC also provided guidance on its initial supervisory expectations for examinations relating to MLA compliance.

Takeaway 2 Management reports, probability of default, and model validation topics were found in the top blogs for risk professionals. Takeaway 3 Updates on interest rate forecasting and best practices for managing CRE risk were among the most-read blogs. The FASB’s description of proposed changes can be found here.

As always, the regulators’ main concern was to promote safety and soundness, consumer protection, and compliance with applicable laws and regulations, including anti-money laundering (AML) and illicit finance statutes and rules.

Cross River Bank recently found itself in hot water with the FDIC when the agency declared that the bank engaged in unsafe or unsound banking practices in relation to its compliance with fair lending laws and regulations, specifically the Equal Credit Opportunity Act and the Truth-in-Lending Act. In effect, Cross River is in time out.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content