This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To that end, the the Internet Crime Complaint Center (IC3), a hub to bring complaints to the Federal Bureau of Investigation (FBI), is eyeing payroll fraud. Beyond the confines of one methodology (payroll fraud, as detailed above), Europol has issued a cybercrime report that has taken note of certain attack methods. The deposits?

In its latest whitepaper, titled “Omni-Channel Payments for Merchants: Myth or Reality?,” From payments security and PCI compliance to frictionless commerce and cross-border considerations, the move to facilitate omnichannel payments is much easier said than done. “At

As my colleague TJ Horan says in his post , the worlds of fraud and compliance are moving closer together. The objectives of the fraud department are different from those of the compliance team and traditionally they have come at the thorny issue of accurately identifying and understanding their customers from different angles.

Traditionally, credit application fraud has been perpetrated in two ways: First-party fraud – where the criminal uses their own identity to commit fraud, even if they obscure some details in order to prevent detection. Where fraud data sharing is in place, their scope may well be limited across multiple organizations.

A new independent survey by research firm Ovum has found that banks in multiple regions plan to integrate their fraud and financial crime compliance systems and activities in response to new criminal threats and punishing fines — but not all at the same speed. said TJ Horan, vice president of fraud solutions at FICO. by FICO.

The recent fascination with artificial intelligence and machine learning has made some of us ( naturally intelligent) humans confused about the role that these technologies play in the broader field of fraud analytics. In the fraud management space, BI can be thought of as a descriptive performance reporter. Source: FICO Blog.

But the global adoption of such schemes, alongside the problems suffered by early adopters, has turned the focus to real-time payments fraud. As discussed in my earlier post , real-time payments make multiple types of fraud more attractive and enable the fast movement and laundering of criminal proceeds. Who Is Liable?

The German financial institution (FI) recently released a whitepaper urging banks and account servicing payment service providers (ASPSPs) to implement PSD2-related changes and reforms within their institution. It acknowledges several hurdles FIs continue to face in that effort. 12, 2018, deadline for implementation passes.

Fraud management and AML compliance are both about tackling financial crime, but often they are managed by different teams, each with their own processes and technology. It’s also true that fraudsters do not operate in siloes when they transfer the money from their frauds into cash by laundering it through a network of money mules.

What Is First-Party Fraud? From banks to telcos to debt collection agencies, what looks like unrecoverable bad debt may in fact be first-party fraud. For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. by Matt Cox.

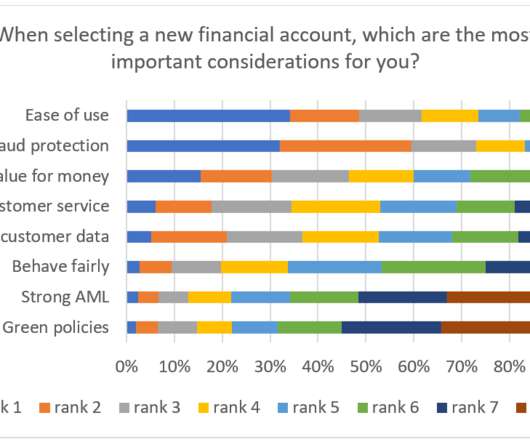

Biometric Security Crucial for Fraud Protection and CX. Because customers value ease of use and good fraud protection most, FIs must balance scam protection with making things easy for good customers – but not TOO easy. How FICO Can Help You Fight Application Fraud. Download the whitepaper on this survey.

For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. Perhaps surprisingly, consumers sometimes use their own personal information to commit fraud. Both of these crimes are first-party fraud.

Artificial intelligence and machine learning are particularly interesting, with their ability to enhance data and analytics capabilities for customer services, compliance and client onboarding and payment processes and fraud detection services, among others.

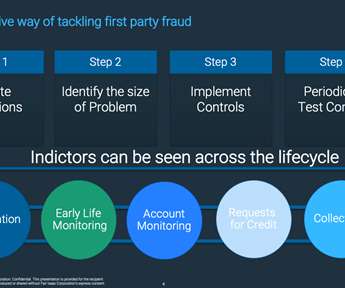

In my previous post I looked at what was driving synthetic identity fraud and discussed the difficulties in classifying both first-party fraud and synthetic identity fraud. An inherent challenge with first-party fraud is sorting out fictional customers from real ones without reducing business. What to Do.

Before getting started, CSPs should determine who “own”’ and is accountable for subscription fraud. Is it the fraud team? Also, is there a clear and agreed fraud risk appetite that has exec sponsorship and is agreed by all stakeholders? In part, this is due to the ever-changing nature of fraud. Credit risk?

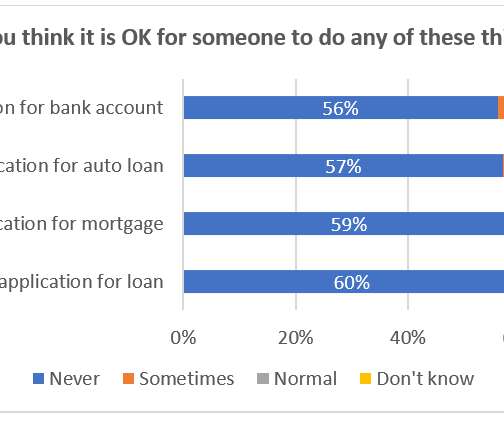

First-Party Fraud Must Be Stopped Across the Customer Lifecycle. While those in the financial services industry would term this first-party fraud, it is evident that a significant minority of people don’t think of such behaviour as unacceptable. FICO Admin. Tue, 07/02/2019 - 02:45. by Sarah Rutherford. expand_less Back To Top.

These regulatory and legal restrictions and public cloud deployment reluctance are especially true for the financial industry and, probably more so, within the financial crimes and compliance space, where highly-sensitive, entity-related information is stored and continuously examined in highly-regulated processes.

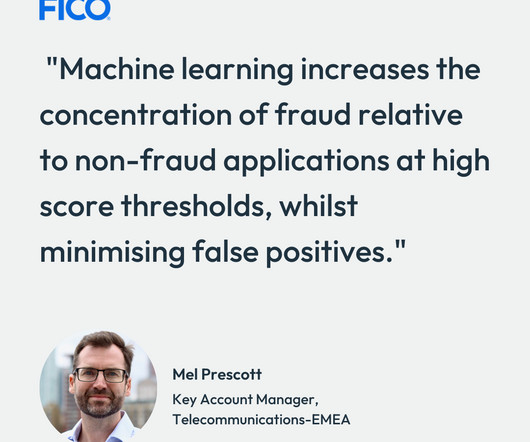

Payment fraud is an ideal use case for machine learning and artificial intelligence (AI), and has a long track record of successful use. Recently, however, there has been so much hype around the use of AI and machine learning in fraud detection that it has been difficult for many to distinguish myth from reality.

Examples given of operational areas that could be impacted by employees working remotely and create compliance and reputational risks included call centers and customer service, collections, dispute investigation, loss mitigation, fraud investigation/ID monitoring, and compliance monitoring.

Top 5 Surprises from FICO’s Fraud and Digital Banking Survey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. A report released by the FTC in February 2022 indicates a 71% increase in fraud in 2021, which cost consumers roughly $5.8 FICO Admin.

While AI has been used for more than 25 years in credit fraud detection , few people outside the banking sphere were aware of this. And it’s not just fraud detection people are asking about — they also want to know about other uses of AI and machine learning for financial crime protection, including in cybersecurity and money laundering.

While AI has been used for more than 25 years in credit fraud detection , few people outside the banking sphere were aware of this. And it’s not just fraud detection people are asking about — they also want to know about other uses of AI and machine learning for financial crime protection, including in cybersecurity and money laundering.

JP Morgan’s fine highlights the broader problem that many global banks had been facing, which was ignoring the warning signings of fraud and money laundering. This tool demonstrates AI’s transformative benefits in anti-money laundering (AML) and fraud detection. billion in 2014. This post originally appeared on the SIIA blog.

FICO global survey finds customers want better fraud protection and more security from their digital banking channels. FICO’s 2022 consumer banking fraud survey shows that customers are split in their thinking on when they sufficiently trust a digital channel to apply for a new account, loan, or credit card. . FICO Admin.

The reduction of onboarding timelines from days to minutes is only the start of the benefits, those additional benefits including: Increased accuracy in detecting merchant fraud and default. FICO Data Orchestrator. Reduced portfolio risk and lower costs. Improved the customer experience, resulting in accelerated business growth.

In some cases, these will be technically defined, in some cases related to social engineering and in others these contexts will be patterns of activity that indicate a higher fraud risk, for example, changing an address and requesting a new credit card. This will dictate in many cases a set of methods which could be used.

With acceptance of biometrics becoming mainstream, and the need for fraud protection ever front of mind, how can banks use biometrics in order to be more effective and efficient? Fraud—do you need to change your approach to thwart a change or increase in attacks. Intelligent Orchestration of Multi-Factor Authentication.

Cordray referenced an April 2020 whitepaper he co-authored that outlined immediate actions the CFPB could take to address the pandemic.) Chopra “his own person” and expects him to take the CFPB in new directions. He expects Mr. Chopra to vigorously pursue ways for the CFPB to support consumers financially injured by the pandemic.

It took the resignation of Lending Club’s CEO and the compliance issues flagged before their Monday earnings to cause the heavens to open up and just drench the entire industry. Then there’s the Treasury’s whitepaper assessing the segment which was released the day after Lending Club’s meltdown.

Note for you damn haters: yes, it’s down from a frothy high of $66,0000, but look at the normalized return over the past 15 years since Satoshi Nakamoto’s whitepaper.) The laser eyes are shining brighter going into 2024. A wonderful investment to help some very valued Americans. The Overhyped Tech of the Year – Real-Time Payments.

If the device profile has also changed, you know there is a potential SIM swap fraud and prevent access or invoke step-up authentication. To prevent fraud and money laundering, activities must be secured with identity checks, including: When an account is accessed. Authentication.

This approach makes a lot of sense– but not sure if it would meet the governance and compliance considerations of most banks and investment management firms. ^SR Download our latest whitepaper that discusses what it really takes to develop a successful Fintech startup. 01:15 pm 10 Reasons Why Fintech Startups Fail.

Andrew just needs to review the account and forward on to compliance for their review. Andrew can snooze until Compliance has done their work so his workspace is not cluttered. They are introducing CrossCore – First smart plug in play fraud and identity platform. About to show use case on credit card fraud.

Started talking about the challenge of having to change credit cards all the time (due to fraud). Helps with mobile onboarding and anti-money laundering compliance. ^SR. We are the global leaders in identity solutions while protecting FI’s and providers from compliance and fraud.” Boy, this is a problem for ME.

One use case is to use a bot, via text messaging, to help customers when they have potential credit card fraud. There is a growing focus on customer experience and related compliance issues. Download: 10 Reasons Why Fintech Startups Fail WhitePaper. You can query the bot to find out your recent transactions.

To those community bankers claiming their growing Compliance departments say no to everything. How about fighting harder with better examples and holding compliance officers as accountable as everybody else. Seriously, given what we see in origination process reviews, we almost understand this. Somebody-Call-the-Whaambulance Award.

I like the idea but I am a bit concerned about the potential for fraud from both companies and investors. Addresses compliance, fraud experience and customer experience analytics. Social media is a special challenge since social media was not created with compliance in mind. users fall victim to fraud.”

To share what we’ve learned about the financial crimes compliance risks associated with crypto, I am delighted to announce an exciting session at FICO’s upcoming Virtual Event, “Success Realized: Digital Transformation Delivered,” which runs April 26-30. Read FICO’s Crypto AML WhitePaper. Sign up today! Want to Dive Deeper?

Companies are turning to accelerators, funds, and labs to try to find the next big thing that will reduce fraud, speed up transaction times, and catch on with consumers. Working with FCAT, the charity searched for third-party vendors and iterated testing on compliance with legal and regulatory requirements to be able to accept Bitcoin.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content