This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Meeting investment accounting and reporting requirements The right technology tools can help institutions manage investment accounting compliance and risk exposure across various investment types. Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence.

Artificial intelligence (AI) is poised to affect every aspect of the world economy and play a significant role in the global financial system, leading financial regulators around the world to take various steps to address the impact of AI on their areas of responsibility. Fraud screening.

However, companies within certain industries may be more hesitant to incorporate a nearshore delivery model into their software development projects due to federal regulations around information and data security. based companies in a variety of regulated industries. Compliance Considerations. Traceability.

Artificial intelligence (AI) is poised to affect every aspect of the world economy and play a significant role in the global financial system, leading financial regulators around the world to take various steps to address the impact of AI on their areas of responsibility.

Secure software practices are at the heart of all system development; doubly so for highly regulated industries such as health-care providers. As a best-practice it is recommended to adopt automation of certain security audits, integration of compliance oversight into key development process areas (e.g.

Lets talk about data governance in banking and financial services, one area I have loved working in and in various areas of it … where data isn’t just data, numbers aren’t just numbers … They’re sacred artifacts that need to be protected, documented, and, of course, regulated within an inch of their lives.

The industry faces numerous challenges, including protecting sensitive data, navigating evolving regulations, and outdated legacy systems. This transformation will require a delicate balance between innovation and compliance, ensuring that advancements in AI contribute to a secure and efficient payments landscape.

For those wanting to start their own cryptocurrency fund, it’s important to be well informed about cryptocurrency regulations. Regulatory cryptocurrency regulations are most fluid at the state level. State Regulations. SEC Regulation. Central Bank Digital Currency (CBDC) ).

Federal regulations under the Controlled Substances Act (CSA) still classify marijuana as a Schedule I substance, along with heroin and methamphetamine. CRBs frequently face difficulties securing loans or even maintaining a bank account, leaving them to manage their cash businesses outside of traditional financial institutions.

Regulation is perhaps the strongest driver of Lithuania’s FinTech-friendly environment. But financial regulatory compliance can be a headache for any market. For traditional banks, compliance experts agree that it’s all about data — and the ability to share information with regulators. Resuming Operations.

Look for folks who: Actually understand the data (a rare breed, cherish them) Can handle details without going cross-eyed Won’t melt down when stuck between the rock of compliance and the hard place of IT Bonus: Give them a fancy title like “Data Integrity Czar.”

Compliance with financial regulations market-to-market around the globe is increasingly automated yet relies on the same human emotion that undergirds all forms of exchange: trust. In other words, banks and financial institutions (FIs) have an obligation to make sure you are who you claim to be.

In financial services, demand for ease of use and security are sky-high, even for business customers. But cloud migrations are often complex, particularly when it comes to remaining compliant with the mounting regulatory initiatives designed to address growing security risks in the financial services arena.

The PYMNTS Merchants Guide To Navigating Global Payments Regulations, done in collaboration with Ekata , examines rapidly changing developments in digital payments at a time when cybercrime — and identity scams particularly — are going hard on legitimate businesses. New Behaviors, Same Regulations. Contactless, Meet Compliance.

As financial institutions deal with growing portfolios, evolving regulations, and a shifting workforce, maintaining consistency in credit risk assessment is more difficult than ever. Data security is also a major concern. Addressing bankers worries about utilizing AI-powered tools, Kirby reassures, Yes, its secure.

Additionally, the emergence of embedded finance and an increased focus on regulatory compliance are compelling financial institutions to continuously adapt and innovate. The integration of AI is reshaping the landscape by addressing challenges such as data protection, regulatory compliance, and the modernization of legacy systems.

Indeed, examiners are expected to emphasize that financial institutions must develop and maintain a culture of compliance. Compliance is not optional," said Josh Hawkins, Senior Director of Abrigos Financial Crimes Investigation Unit. Those changes require upgraded technology and staffing efforts. Our Advisory Services team can help.

As a result, the pace of data privacy and data regulation has accelerated on a global scale. Ensuring the security of your proprietary and customers’ data is paramount to staying in line with ethical and regulatory standards and retaining customer trust. . Sensitive Data: Regulated. Classify your data.

By ensuring compliance with regulations, banks mitigate risks and maintain trust with customers and regulatory authorities. To stay ahead, banks should adopt compliance technologies that automate regulatory reporting and help them stay agile in a rapidly changing landscape.

Banks in the EU have been racing to comply with the General Data Protection Regulation ( GDPR ) and the revised Payment Services Directive ( PSD2 ) since both measures were enacted in 2018. He explained that the cloud can help FIs swiftly respond to compliance and security challenges during the pandemic.

However, due to their sensitive and regulated natures, some industries – especially the financial services industry – have had more complicated cloud transformation journeys than others. Security Traditionally, information was said to be most secure when separated and segmented.

What NBFIs Should Know About Their AML Programs NBFI AML compliance requirements are top of mind in today's regulatory environment. Takeaway 2 NBFIs should ensure their AML programs are sound and pass the scrutiny of FinCEN and their primary regulators. NBFIs’ AML compliance requirements. DOWNLOAD . Competing with Banks.

Payment system types, trends, and fraud risks Understanding how payment systems function, the different types in use, and the associated risks is critical for financial institutions to be able to balance innovation with security. Payment systems are at the heart of modern banking, enabling secure and efficient money transfers.

Trade finance players, including corporates, banks and regulators, are finally ready to embrace modernization and technology. As a highly regulated area of financial services, trade finance has struggled to enter the digital age. Previously, regulation was very slow in adapting and approving of different technology," he said.

The rise of insurtech is running parallel to the rise of regtech, as financial firms and startups apply artificial intelligence, blockchain, and other technologies to the dizzying world of financial regulation.

As data privacy becomes enshrined in international law, regulatory compliance will grow more stringent and costly to companies that fail to provide the digital defenses these laws demand. Payments orchestration is a hot commodity now for its potent capabilities in streamlining and security. Tokenization Takes A Bow.

Reducing fees for remittances might push price points low enough that more consumers could resume sending money home, though, and some researchers believe that money transfer service providers could make such price adjustments if they are able to reduce their own expenses through more robust and cost-effective regulatory compliance measures. .

Last year, regulators in New York decided to take cybersecurity matters for financial institutions into their own hands, releasing a set of rules (which went into effect in March), requiring banks and other FIs to establish a stricter cybersecurity program.

The California Consumer Privacy Act went into effect in January, and the European Union’s General Data Protection Regulation ( GDPR ) went into effect in 2018. The result of single-state legislation could result in a patchwork of laws that force businesses to establish state-specific compliance systems, he added. “It

Secure Authentication: RCS offers stronger security features compared to SMS, making it a viable option for two-factor authentication and other bank security measures. Security Concerns: Despite its enhanced security features, RCS is still susceptible to cyber threats.

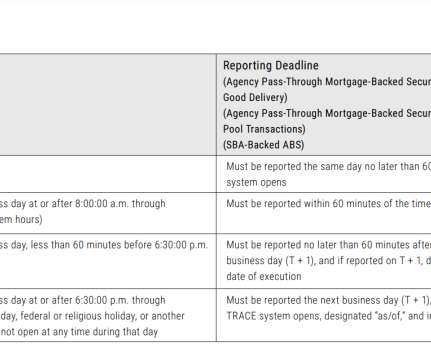

debt market, the Financial Industry Regulatory Authority (FINRA) developed the Trade Reporting and Compliance Engine (TRACE) in 2002 to facilitate the mandatory reporting of OTC bond transactions in eligible fixed-income securities. Treasury Securities to TRACE. To promote transparency in the large U.S.

Already reviewed by Perficient, BES provides a secure and efficient portal to exchange documents, information, and communications for consumer compliance and Community Reinvestment Act (CRA) examinations. Bank executives and supporting third parties will be authenticated using a secure two-factor authentication process.

A strong BSA prog r am starts with FFIEC compliance Building a robust BSA program means having access to the staffing and resources you need. You might also like this podcast, "Ensuring access to the FFIEC’s suitable resources at your financial institution: What BSA compliance officers need to know.

Consumers pivoting to online banking are also more concerned over the privacy and security of their data, especially as fraud volumes creep up —and financial regulators are taking notice. Banks are continuing their ongoing movement to the cloud even as data and security questions continue to grow. Around The Cloud Banking World.

Takeaway 3 By staying vigilant and adopting a proactive approach, financial institutions can create a more secure real estate environment that safeguards against money laundering. Real estate money laundering is a serious issue that has become increasingly prevalent in recent years, although it is one of the oldest forms of money laundering.

FINRA member participation in TRACE is mandatory and obligates members to submit transaction reports in TRACE-eligible securities to conform with the Rule 6700 Series. Once FINRA receives and executes the TRACE Participant Application Agreement, a TRACE participant may input the trade information in TRACE-eligible securities.

Atlanta payments encryption firm Bluefin is partnering with New York mobile payments processor PAAY to advance eCommerce security. Founded in 2007 by Miles and John Perry, who serves as chief executive officer, Bluefin specializes in encryption and tokenization payment and data security. . Each $1 of fraud costs retailers $3.13. .

EXCLUSIVE— Cryptocurrencies are experiencing one of their highest points in recent weeks, after remarks made by former financial regulator Gary Gensler brought back concerns that certain tokens should really be considered securities.

Culture of compliance is crucial to BSA/AML programs Culture of compliance within the BSA/AML framework is not new and was first introduced by FinCEN in 2014. Takeaway 2 Poor culture of compliance will result in shortcomings in a financial institution's BSA/AML program. A strong culture of compliance is crucial.

Robinhood has come under the watchful eye of regulators — this time in Massachusetts. State regulators are set to file a complaint on Wednesday (Dec. 16) saying that the stock-trading platform failed to protect its customers and their assets, violating state laws and regulations.

Government regulators and cryptocurrency exchanges are frantically looking for ways to regulate and prevent the laundering of stolen money through cryptocurrencies, with some methods showing more promise than others. Enforcing AML/KYC Compliance At Cryptocurrency Exchanges. Cryptocurrency-related crimes totaled $4.3 or the U.S.,

Finally, views are sought for compliance with applicable laws and regulations, including those related to consumer protection. Applications include analysis of regulations, news flow, earnings reports, consumer complaints, analyst ratings changes, and legal documents. Cybersecurity.

All broker-dealers who are FINRA member firms have an obligation to report transactions in TRACE-eligible securities under an SEC-approved set of rules. TRACE time reporting requirements have numerous intricacies based on the security, the issuance status of the security, and the time of day reporting occurs.

We’re putting this into practice and offering our predictions concerning what regulations may arise once the dust has settled. The Tier 1 leverage capital ratio of the firm was 8.11%, more than twice the 4.00% required by regulators. But the fault is the regulators’, right? Securities 4a. Possible Causes of Failure 1.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content