This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Digital transformation will remain a powerful force, with advancements in AI and machine learning enabling unparalleled operational efficiencies and hyper-personalized customerexperiences. Banks will look to transform the way they do business by moving beyond their walls with the maturing of open banking and embedded finance.

FinTechs are helping banks focus on the customerexperience through accounts payable (AP) automation. told PYMNTS in an interview that banks foundationally value “the relationship they have with the customer” and “they understand the customer.”

This means banks must make security an engaging part of their customerexperiences rather than a clunky friction point, and many are doing so by turning to AI and biometric authentication tools. While passwords are often arbitrary and static, biometric authentication methods are based on customers’ personal data.

Banks lost about $4 billion to account takeover (ATO) fraud attempts last year and fraudsters have been reluctant to abandon the scheme as this year progresses. Arou nd the DigitalBanking World. Banks in other regions are also dealing with data breaches of their own, such as U.K. digitalbank Monzo.

Banks are increasingly embracing new channels to offer seamless omnichannel services to their customers, but doing so often creates silos that handle large amounts of collected data. Omnichannel Fraud Protection. Banks Bet On DigitalBanking . consumers now use mobile banking.

In one of the signs of where we are and where we are headed in the warp-speed transformation of digitalbanking, consider the internet meme that poses a multiple-choice question and series of answers. Who led the digital transformation of your company? A) CEO B) CFO C) COVID-19.”.

Many financial institutions are achieving this state of vigilance by investing in artificial intelligence (AI) and machine learning (ML) solutions as part of their anti-fraud efforts. . But as Jeremy Balkin, head of innovation for Swiss bank HSBC , recently told PYMNTS, even AI and ML need assistance sometimes — from humans. .

Banks’ use of such innovations is predicted to expand, too, with 60 percent of FIs saying they aim to gain customers and improve customerexperiences using digital channels. This increased digital presence also brings a greater risk of digitalfraud, however. How Authentication Prevents Fraud.

As we explored in the first part of this two-part guide, digitalbankingfraud is an escalating threat to financial institutions and their customers. Digitalbankingfraud can take many forms, such as identity fraud and account takeover , which are becoming increasingly common. million in 2016.

This can lead to consumers contacting their banks, which could incur costs and waste time with unnecessary chargebacks. Mastercard, through its collaborative fraud and dispute resolution technology Ethoca , will now offer a new version of online statements with added logos and clear business names for each transaction.

The last few years have thrown up many challenges for banks and card providers as everything has shifted online, one of the primary challenges being fraud scams. But the online shift has also created opportunities for financial institutions to demonstrate their strong fraud controls in the digital space.

Risk looms large with rampant growth in fraud, however, and financial institutions (FIs) must stay guarded to prevent cybercrime. The question becomes how you use those strengths and capabilities, and that’s really up to each individual bank.”. Reducing Risk By Fighting Fraud. The financial services industry is booming.

Last year we published a highly successful The 11 Commandments of DigitalBanking eBook that introduced the 11 commandments: Digital lift-and-shift is not a strategy! In addition to a new blog post that will be published monthly over 5 months, we are also excited to launch the following event: LinkedIn Live on DigitalBanking.

With fraud attempts continually on the rise around the world, financial institutions have their work cut out for them. They must remain fully compliant with regulatory standards and combat fast-learning fraudsters while maintaining a frictionless customerexperience. AI and the Future of Fraud Protection.

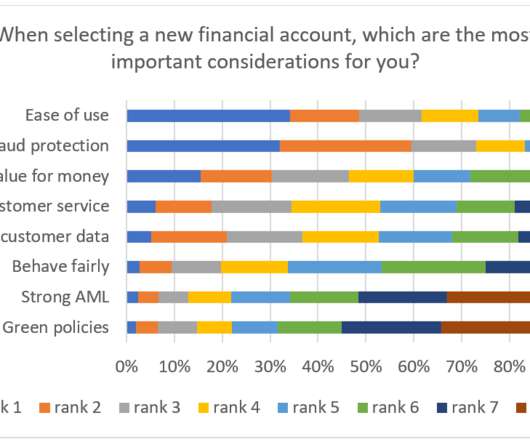

To understand customers’ perceptions of what matters in digitalbanking including account openings, FICO recently commissioned an independent consumer survey of nearly 5,000 people across ten countries including: Brazil. Not Meeting DigitalBanking Needs - Could Lead to Loss of New Business. Philippines.

And increasingly, those services are being leveraged in verticals such as online sports betting, where location must be verified at the time of the wager (to make sure the activity is in a legally permissible area) to help banks comply with international Know Your Customers (KYC) rules. Not all data are created equal, of course.

Among the keys to a successful customer life cycle is the act of opening an account — and a smooth experience can make or break a relationship at inception. An online customerexperience is the key metric that drives new customer acquisition and retention. “We and acquire more customers.

The ATM has emerged as one of CUs’ most important tools in this member engagement effort, in fact, with many investing in digitally-enabled ATM kiosks that provide members with on-demand videoconference consultations and a full range of digitalbanking services. Deep Dive: Offering An End-To-End CustomerExperience Through ATMs.

High fees, poor customerexperiences, and archaic technology have historically blocked many from accessing financial services. . get the state of challenger banks report. Below, we dive into how the Covid-19 pandemic has accelerated the shift to digitalbanking among these populations. Source: PwC. Globally, 1.7B

Both of these channels are thus perfect targets for fraud, with cybercriminals posing as restaurants on social media and attempting to scam customers of their personal data, and fake reviews driving customers away from restaurants.”. Successful attacks are often the result of inadequate digital defenses meeting these methods.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. 2019 website.

ANZ , Commonwealth Bank , IBM , Scentre Group and Westpac have announced they are partnering to launch a live pilot for Lygon, a new digital platform using blockchain technology to digitize the bank guarantee process needed for retail property leases. This is IBM’s latest foray into blockchain.

For better authentication, financial institutions (FIs) are experimenting with artificial intelligence (AI) and biometrics, attempting to create security measures that don’t frustrate consumers. In the latest DigitalBanking Tracker™ , PYMNTS examines how banks are innovating to address these security vulnerabilities.

Mobile banking apps have already enjoyed mass adoption, but what are consumers using them for? And, perhaps more importantly, what do they want from digitalbanking apps that they aren’t currently getting? Banks might also benefit from being open with their customers about where mobile banking app fraud liability lies.

As can be seen, the conference largely revolved around payments, artificial intelligence, fintech partnerships/management, regulation, and fraud/identity in its various forms. The discussions were healthier, more compliance-focused, and with little expectations that banks were going to offer crypto to their customers any time soon.

The result is a slew of unstructured data coming in from a variety of sources; financial service providers must try to make sense of it in order to maintain regulatory compliance and mitigate the risk of fraud. Middesk aims to help these firms streamline and digitize this process. A Better Business CustomerExperience.

Our recognition as the #3 community bank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. Yet, the banking industry is at a turning point. Customers increasingly demand seamless digital experiences91% of U.S.

Digitalbanking and eCommerce are making rapid gains in 2020 as consumers turn to online channels to make purchases and avoid potential exposure to COVID-19. Synthetic ID fraud can be especially hard to spot. Long-running synthetic ID schemes have illuminated gaps in FIs’ traditional fraud-fighting measures.

Banks are jostling for space in the market because an expanding number of FinTechs and large-scale technology companies are competing for the same set of consumers. Banks must enable fast and seamless onboarding experiences, but these processes should also be secure. Data and Authentication Frustrations.

Top 5 Surprises from FICO’s Fraud and DigitalBanking Survey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. million consumer fraud and 1.4 FICO Admin. Tue, 07/02/2019 - 02:45. by Sarah Rutherford. expand_less Back To Top.

I will define it here for financial services and regulated companies as the business strategy and processes by which an organization establishes who a customer is and ensures that activity on their accounts is carried out by them. Customer identity management operates today in an unpredictable environment. Customer screening.

Banks must be prepared to help stop scams, including making customers more aware of the danger, all while continuing to ensure an exemplary customerexperience. Survey Findings: Digital Dominates, But CustomerExperience Remains Important. Some Consumers Lack Confidence in Bank Security, Dissatisfied.

Banks must be prepared to help stop scams, including making customers more aware of the danger, all while continuing to ensure an exemplary customerexperience. Survey Findings: Digital Dominates, But CustomerExperience Remains Important. Read below to review some of our key findings.

Account takeovers (ATOs) are a growing source of pain for financial institutions (FIs) and their customers, with losses from these attacks rising 164 percent in 2018. FIs must adopt fraud-fighting measures that are robust but do not create so much friction that legitimate customers find it difficult to access needed services.

Technologically integrated credit union services create more and better data, Stevens said, and the data itself is the secret ingredient to creating better customerexperiences and security protections. Using Data To Build What’s Next.

Pierce said the consumer data shows that 13 percent of credit union members have been a victim of card fraud , and 4 percent have had their identities stolen in the last year alone. Moreover, Lynch told PYMNTS, the fraud is coming across on all channels. So, they are just as covered by fraud liability.

Biometric Security Crucial for Fraud Protection and CX. Because customers value ease of use and good fraud protection most, FIs must balance scam protection with making things easy for good customers – but not TOO easy. Customers Prefer Easy & Safe. Customers Prefer Biometric Security. FICO Admin.

Creating secure banking environments without generating undue customer frictions relies on strong front- and back-end approaches to help FIs spot red flags, create login experiences that are harder for bad actors to crack and guide customers on how they can avoid falling victim to ATOs. Customer-Centric Authentication.

After the pandemic essentially caused in-branch banking to be impossible for many months, banks were forced to revamp their online account opening processes (among other digitalbanking capabilities) so that they could still acquire new customers. Identity and risk profiles for your customers.

In particular, Alacriti said its new Cosmos for RTP “end-to-end solution features ISO 20022 native services, open APIs, integrated fraud detection and monitoring, and connectivity to The Clearing House’s RTP network.”

How is application fraud evolving? And what should fraud leaders be doing to manage fraud risk in a digitally connected world? To answer those questions, we spoke with a man with 25 years of experience in fraud management, Bob Shiflet. How did you liaise with other groups within the business?

Delivering leading AI-driven fraud prevention to a new business model. Conductor, the leading payments and banking-as-a-service platform in Latin America, has increased fraud detection by 25 percent and reduced overall payments fraud by 18 percent. You can read more about this story in the full media release.

Application Fraud – Does Canada Need a New Approach? FICO’s Fraud, Identity and DigitalBanking Survey 2022 shows that customers in Canada want slick onboarding processes, where fraud controls work but don’t delay account opening. And what does that mean for the future of your fraud management solutions?

Owens noted that Elan aims to improve the customerexperience by providing mobile functionality, geolocation, AI-based fraud protection and all forms of digital payments. These are expensive to deliver, which is why we help customers provide these services and capabilities as part of the package,” he said.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content