This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Digital transformation will remain a powerful force, with advancements in AI and machine learning enabling unparalleled operational efficiencies and hyper-personalized customerexperiences. Banks will look to transform the way they do business by moving beyond their walls with the maturing of open banking and embedded finance.

It’s one of a banker’s worst nightmares: the digitalbanking conversion that was designed to improve the customerexperience fails – locking users out of their accounts, not showing balances, making wire transfer features inaccessible… It recently happened to a $25 billion bank in the Midwest.

Following the highly successful The 11 Commandments of DigitalBanking eBook , we are kicking off a series of 5 deeper dive blog posts that group the 11 commandments below into common themes. Digital lift-and-shift is not a strategy! Banks must find ways to be personable in these impersonal channels. Respect the data.

According to a survey conducted last year by the Global Association of Risk Professionals (GARP), 88 percent of bank executives believe AI and ML adoption could provide “a foundational change” for riskmanagement. contact-form-7]. . About The Tracker.

In a recent conversation with PYMNTS, Diehl noted that FinTechs are in a unique position to compete against traditional lenders, and the pandemic doesn’t take away from their ability to provide what is often a more favorable customerexperience than that of a traditional lender. “On They, too, experience tough challenges.”.

Our recognition as the #3 community bank in the state by GOBankingRates in 2025 reflects our commitment to Growing, Together with the communities we serve. Yet, the banking industry is at a turning point. Customers increasingly demand seamless digital experiences91% of U.S.

Executives should embrace technology partners as a means of growing and enhancing their customer value proposition. To do this, banks can leverage their competencies in payments, lending, operations, and riskmanagement while using the earnings generated from BaaS to transform their core business.

The catalyst was likely a panel led by the CEO of Taktile (AI Underwriting), a Partner from Bain Capital, a partner for Andreessen Horowitz, the chief data scientist from Branch International (digitalbanking fintech for India and Africa), and a tech correspondent for CNBC.

This movement — core to cloud — is essential for banks seeking to modernize their legacy systems and become agile and flexible. This is especially true if they’re going to compete with new digitalbanks and platform companies that are unhindered by the legacy applications and infrastructure. This is essential.

Sure, we know it’s cliche to point out the merits of this direct banking powerhouse, but the plain fact is that USAA nails every variable in building a Smarter Bank. The bank’s strategy is laser-focused. Its Baldrige-winning tenacity on customerexperience is legendary and consistent. Might be time to.

Trust acquired 100,000 customers in just ten days after it launched in September 2022 and exceeded 450,000, equivalent to 9 percent of the Singapore market, within just five months. We combine riskmanagement fundamentals with data science and customer segmentation to help us arrive at optimum risk outcomes,” said Lohia.

Acme Bank has a mission of “Helping Clients Succeed Today and Tomorrow,” but this organization is mostly steeped in discussions regarding products, competitors and quarterly production. There are no visible managerial processes tied to customerexperience and learning. We have to reshape Acme Bank quickly for the future.

Home Blog FICO Top 5 Customer Development Posts of 2022: DigitalBanking and Pricing Opti The most popular posts in our Customer Development category dealt with digitalbanking, optimizing credit line increases, loan pricing and machine learning for credit risk models.

As he noted, the experience and documents required often mean that users must wrestle with desktops, paper IDs or files — crossing channels, in effect — just to get on board. The question for FIs, he said, is: “How do you bring technology and customerexperience together to create a user-centric journey?”. The Challenger Banks.

There have been many come-and-go digitalbanks. For a digitalbank, Axos has a net interest margin twice that of Wells and BoA with an expense ratio under 2% – that helps drive a 15.5% It’s great to see Axos continue to hone its strategies and maintain the margins/credit quality that the market is rewarding.

The speed at which digitalbanking is being transformed by new technologies is rapidly increasing. From behavioral biometrics to new selfie technology, financial institutions are being presented with even more ways to distribute their services across digital channels to meet customers where they want to interact.

A lover of picking bank stocks and playing piano who served our country in the U.S. which provides digitalbanking videos and user guides to help FIs increase their customers/members’ digital adoption. Paul wrote the “ Online Banking for Dummies ” book in the late ’80s. He passed away in January 2023.

In this blog – the second in this two-part series – I’ll look at how banks should respond to the shifts happening within trade and supply chain finance due to market forces and COVID-19. The post Global trade’s new normal: how banks can react appeared first on Accenture Banking Blog.

If running the capital plan numbers indicates that growth needs to slow, banks will need new tactics to drive profitability, and a major focus will return around operating efficiencies. Digitalbanking uptime, the speed and accuracy of moving money, and the ability to talk to informed bankers are vital right now.

The bank was looking for a modern, digitalbanking solution that would help it transform customer engagement through the delivery of contextual experiences. Furthering the government’s vision of moving operations and infrastructure to the cloud, BDB wanted to host the entire core banking platform on a public cloud.

Consider: Digitalbanking/channel migration plan – The institution’s digitalbanking plan involves every line of business that touches customers. Risk plan – Operational riskmanagement is a company-wide discipline that has become the focus of regulators, boards, and the “C” level.

So far, bankers have taken comfort in the soundbite that “this crisis is different” because of the strong capital levels and riskmanagement rigor that has developed since the Great Recession. The problem today is that most banks are not applying a true product management discipline to the debit and credit business.

But, taken too far, having too many controls makes for a frustrating experience that can drive customers away. How can banks deliver unified experiences across multiple channels, with the right amount of friction, to navigate the fine line between fraud reduction and customerexperience?

Barbican’s Cyber Business Group Leader, Graeme King, explained, “Risk and IT can be disconnected in respect of to cyber insurance. There can sometimes be miscommunication between the IT function, which controls the items introducing risks, and the riskmanagement group, which buys insurance cover to protect against these risks.

It enables banks to trade high volumes of treasury and complex derivatives and options through an open platform which, via open APIs and datasets, unlocks the power of collaboration and innovation. The Co-operative Bank also uses Fusion Risk for treasury credit riskmanagement and Finastra’s banking technology for payments services. “By

The FICO Advisors team of consultants has just published our third COVID-19 bulletin to help banks adapt and thrive in these unprecedented conditions. Here are our five recommendations for credit riskmanagers. Consider all your customerrisk segments. Want to learn more? by Daniel Melo.

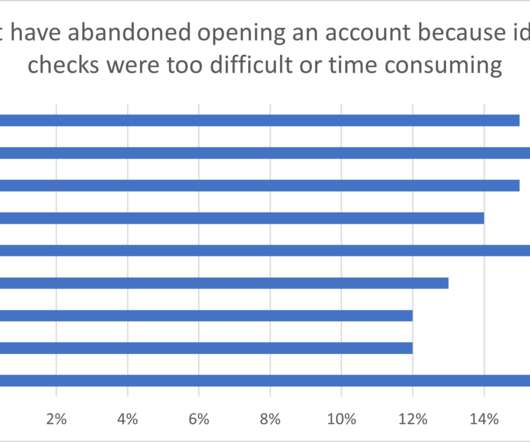

FICO’s Fraud, Identity and DigitalBanking Survey 2022 shows that customers in Canada want slick onboarding processes, where fraud controls work but don’t delay account opening. Processes that Balance CustomerExperience and Fraud Protection. Application Fraud – Does Canada Need a New Approach? FICO Admin.

Since worries about regional bank struggles and an uncertain stock market are driving people with cash to look for safe havens and good interest rates, it pays to be very careful about security as well as who is behind the friendly new banking brand. TJ holds a B.S. in computer science and a M.S.

Cost is a big reason why – the less folks get cash from ATMs, the more costly it is per transaction to serve customers. This is simply the natural evolution as people rely more and more on digitalbanking using their device of choice. With fewer ATMs, the availability of cash is decreasing. TJ holds a B.S.

Note: A version of this blog post originally appeared in the Center for Financial Inclusion blog. As a financial industry veteran, I have dedicated a lot of time and energy to researching, analyzing and implementing strategies to grow financial businesses. But until last year, I spent very little time thinking about financial inclusion.

Our Actionable Intelligence Management solutions help banks and mortgage companies streamline and automate manual processes, seize new business opportunities and manage compliance, all while transforming the customerexperience. Key Partnerships & Customers. Key Advisory Board Members.

Avoka’s digital commerce platform helps banks, insurance and wealth management institutions overcome the challenge of “selling” financial products by offering a frictionless, omni-channel customerexperience.

ID Analytics is a leader in consumer riskmanagement with patented analytics, proven expertise, and real-time insight into consumer behavior. IDmission provides a cloud-based platform enabling identity initiated customer onboarding and engagement for financial services companies.

The operational world of cash, checks, deposit slips, passbooks, and teller terminals used to dominate bank tech budgets. Those were the days of green screen cores and server-based ancillary applications, and digitalbanking was a Star Trek thing of the future. Enterprise Resource Manager.

Simultaneously the bank invested in Paladin Fraud, Trabian Technology, and Chartwell Compliance to provide compliance and riskmanagement solutions in the complex and connected web of fintech partnerships. The CustomerExperience Award – Goes to Capital One for moving fleet-footed to react to the new realities of retail banking.

While technology budgets are always difficult to compare, banks are expected to spend 4.7% According to a recent survey by Gartner, Revenue growth, margin improvement and better riskmanagement are the top three functional objectives, in order, for next year. Bank marketing has become significantly more effective and efficient.

The click_here_this_is_not_a_phishing_email award goes to the fraud and digitalbanking team at Security Financial Bank in Durand, Wis. Security Financial Banks home page starts off with fraud education for its customers and it actively maintains and updates its Facebook page with common fraud scenarios.

However, we’ve gone from spotty Siri performance and playing with Amazon Alexa with our stereo system to Bank of America predicting its chatbot, Erica, will become customers’ new financial advisor. Most Important Tech Challenge of 2017 – The urgent need to meld digitalbanking with digital marketing.

However, we’ve gone from spotty Siri performance and playing with Amazon Alexa with our stereo system to Bank of America predicting its chatbot, Erica, will become customers’ new financial advisor. Most Important Tech Challenge of 2017 – The urgent need to meld digitalbanking with digital marketing.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content