This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

4 Reasons better check fraud prevention is a good investment Check fraud is on the rise. Learn how you can save time and money in the long run by updating check fraud prevention capabilities today. At the same time, check fraud is increasing dramatically. At the same time, check fraud is increasing dramatically.

The prevalence of online commerce opens new doors for digital fraud, however, both from career fraudsters and opportunistic customers. Developments F rom The World Of Digital Fraud. Developments F rom The World Of Digital Fraud. For more on these and other digital fraud news items, download this month’s Tracker.

Digital fraud is a long-running problem for merchants, retailers, banks and businesses of all types. Account takeovers and shipping fraud increased by 347 percent and 391 percent, respectively, between 2018 and 2019, and the pandemic has only exacerbated these issues. Developments From The World Of Digital Fraud.

Synthetic ID fraud is growing quickly and hurts FIs and customers Knowing the schemes associated with synthetic identity fraud and how criminals avoid detection can help minimize losses. Takeaway 1 Synthetic identity fraud is a growing form of identity theft in which an individual is impersonated by using stolen information.

Takeaway 1 Implementing the FedNow Service can help reduce interbank obligations, expand market reach, and enhance customerexperiences. Essential components for connection include: Front-end services: Provide customers with online or app-based options to send and receive payments.

While the fraud-fighting technology available six years ago didn’t stand a chance of protecting HiGear, the current car-sharing market , which is projected to be worth $16.5 billion by 2024, continues to experience similar fraud attacks. As machine learning has evolved over the years, so has the level and type of fraud.

ACI Worldwide advises that, as the world moves toward immediate payment ecosystems, a holistic view of the transaction, with layered controls from origination to the application of real-time rules, is the only way to push the pedal to the metal on faster payments and put the brakes on fraud. million in 2007 to £52.5

Widely publicized data breaches and hacks have made today’s consumers especially concerned about fraud. Cautious shoppers may find comfort in debit, with fraud losses associated with the payment method declining over the past several years. Card fraud is an ever-present threat. A Big-Picture Approach To Thwarting Debit Fraud.

While the holiday retail rush meant big gains for some retailers, it also came with an influx of fraud, both in-store and online, as fraudsters took advantage of a high-pace, high-volume period of transactions. In fact, over 5 percent of online retail revenue is now lost to fraud. Around The Digital Fraud World.

The last few years have thrown up many challenges for banks and card providers as everything has shifted online, one of the primary challenges being fraud scams. But the online shift has also created opportunities for financial institutions to demonstrate their strong fraud controls in the digital space.

When it comes to fraud, are people worried about the wrong things? New data suggest that people are concerned about fraud, but one of the biggest threats seems to be flying under the radar, at least for consumers. That threat is fraud scams – tactics and techniques that fraudsters are using to trick people into giving away their money.

Better Pinpoint Your Risk(s): Predictive analytics to better target risks, artificial intelligence to identify fraud, and intelligent automation to improve operational efficiency are at the heart of insurance digital transformation moving forward.

At the same time, fraud remains a pressing and persistent problem. banks are losing more than $31 billion every year to fraud, including account takeover and new account application fraud. Expanding on the use of Trojans, he said banking Trojans disguise themselves as a legitimate app or software that users download and install.

Such investments in digital technology are expected to increase return on investment (ROI) and improve the overall customerexperience. They are also designed to reduce fraud and chargebacks while shrinking labor costs with self-ordering capabilities via tablets and kiosks. To get the full story, download the Tracker.

PYMNTS recently spoke with Luis Rojas, vice president of product management for Guardian Analytics , an online banking security firm, about the effect of a faster processing environment, the potential for increased fraud and how to mitigate that risk. The Mountain View, Calif.-based People are bracing for a similar spike here,” he added.

Maybe one day, quick-service restaurant ( QSR ) operators will look back upon 2019 as their cramming experience when it comes to digital security and fraud prevention. In fact, missteps in digital fraud prevention can, as Stuppy said, “put the entire digital investment at risk.” Fraud Prevention Optimism.

For more on these and other CU news items, download this month’s Tracker. How Balancing Members’ Needs Improves End-To-End ATM Experiences. Deep Dive: Offering An End-To-End CustomerExperience Through ATMs.

Providing a unique customerexperience to subscribers is crucial, according to Robin Reodica, product management executive director for Bank of America Merchant Services — especially with more eTailers unveiling their own subscription plans. About The Tracker.

To understand the statistics for the individual countries surveyed download the infographics: Brazil. In my following research findings blog, I will look at how consumers view the methods financial institutions use to authenticate their identities and secure their accounts. Philippines. www.fico.com/identity. by Sarah Rutherford.

This spans from the use of virtual assistants that can help insurance companies quickly train agents to artificial intelligence (AI)-powered chat aimed at making up for workforce shortages, as well as a variety of new data handling and fraud prevention solutions. For the full story, download the tracker. Around The Call Center World.

Just beneath the smartphone glass, brainy new tech is powering payments in ways that emphasize security and speed, while keeping one eye fixed on customerexperience. consumers, the latest Mobile Card App Adoption Report finds that over 40 percent of American shoppers have downloaded a payment app onto their phone.

Many enterprises have succumbed to the inclination to digitize everything, which by default leads to cold, clinical experiences. It’s difficult, but embracing new technology means that we have the opportunity – nay, the imperative – to focus on humanizing the customerexperience. Omnichannel is customer-led.

“It’s also increasingly where the cool customerexperiences are happening and where customers want to interact online. In the past several years, we’ve really seen a merger of safety and customerexperience that’s predominantly happening because of the usage of mobile devices.”.

Maybe one day, quick-service restaurant ( QSR ) operators will look back upon 2019 as their cramming experience when it comes to digital security and fraud prevention. In fact, missteps in digital fraud prevention can, as Stuppy said, “put the entire digital investment at risk.” Fraud Prevention Optimism.

As goes digital commerce, so goes fraud. The right platform will allow them to combine layers of security — like tokenization, biometric authentication, PINs and back-end fraud management — to achieve the right balance of security and usability. Fewer checkouts also mean staff can be redeployed in-store to support customers.”.

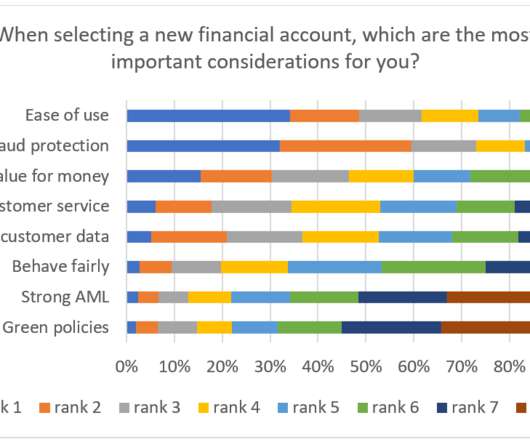

Biometric Security Crucial for Fraud Protection and CX. Because customers value ease of use and good fraud protection most, FIs must balance scam protection with making things easy for good customers – but not TOO easy. Customers Prefer Easy & Safe. Customers Prefer Biometric Security. FICO Admin.

Both fintech firms and traditional enterprises are on the brink of significant disruption as companies leverage the rapid insights generated by AI in banking to drive demonstrable outcomes in customerexperience, risk management and cost efficiency. Customer service in finance is also getting an overhaul thanks to cognitive solutions.

DOWNLOAD Takeaway 1 With generative AI technology improving by the day, the question is not if the banking industry will utilize it, but when. Takeaway 2 AI can lead to more accurate and consistent outputs or predictions, better risk management, and improved customerexperiences.

I’ve been writing recently about the results of our recent global consumer fraud survey. But like most things, it’s not as simple as it sounds, as large customer groups are likely to switch banks if they are dissatisfied with their response to a fraud management incident (more on that in a moment).

Application Fraud – Does Canada Need a New Approach? FICO’s Fraud, Identity and Digital Banking Survey 2022 shows that customers in Canada want slick onboarding processes, where fraud controls work but don’t delay account opening. And what does that mean for the future of your fraud management solutions?

When it comes to fraud, are people worried about the wrong things? New data suggest that people are concerned about fraud, but one of the biggest threats seems to be flying under the radar, at least for consumers. That threat is fraud scams – tactics and techniques that fraudsters are using to trick people into giving away their money.

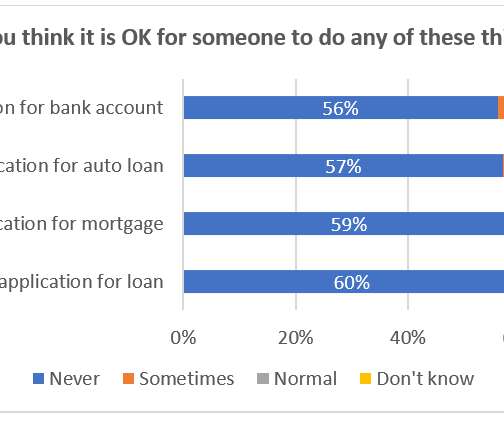

First-Party Fraud Must Be Stopped Across the Customer Lifecycle. Financial institutions face first-party risks “inside the wire” - 14% of customers worldwide think it is normal to exaggerate income on a mortgage application. Another data point demonstrates how customers view the commission of similar types of fraud differently.

Top 5 Surprises from FICO’s Fraud and Digital Banking Survey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. A report released by the FTC in February 2022 indicates a 71% increase in fraud in 2021, which cost consumers roughly $5.8

The firm’s gMobile solution, which helps authenticate users and delivers real-time risk analysis across mobile channels, debuted late last year, and McAlear said that the platform “enables delivery of a frictionless customerexperience, requiring no additional customer input, scripting or burdensome software downloads.”

And to be truly successful, bankers and designers need to create a religion around conversion rates and understand what drives them. The Most Important Conversion Rates (online loan example): Application Rate – The number of people who visit your website or download your mobile app vs. the number of people who apply.

For more on these and other CU news items, download this month’s Tracker. Keeping customers engaged is the primary goal of any business, and CUs are no exception. AI-based tools and programs are becoming commonplace in the financial industry, employed in everything from fraud detection to risk evaluation.

For example, ISO 20022 provides a set of messages (you can download HERE ) to handle ATM transactions, fraud, account names, and time periods. Enhanced CustomerExperience: With its rich data capabilities, banks can offer better services to their customers.

To adapt, let alone thrive, businesses with store locations must embrace EMV, the latest in payments security and authentication, especially considering the retailers themselves have taken on more responsibility for fraud after 2015’s liability shift. The challenge for the last year has just been educating our customer base.

Payments is never boring these days, and that holds especially true as a new decade looms, new regulations are kicking in and merchants, card brands and payment services providers race to build more secure and efficient customerexperiences. All those changes can be a lot to take in. Ekata (@EkataGlobal) October 29, 2019.

It’s much harder to get it back or stop or fix a fraud attack after it’s happened.”. In order for both the bank and its customers to feel comfortable with real-time transfers, Vancini and his team have worked to offer new security methods. “One For now, the answer’s inherently elusive, because it’s mobile.

In the 2023 FICO Global Scams Survey , we asked consumers worldwide what they think banks could do better to combat scams and create a better customerexperience for victims. Their top five responses provide a blueprint of customer-friendly steps banks can take to counter RTP scams and improve customerexperiences when scams occur.

High fees, poor customerexperiences, and archaic technology have historically blocked many from accessing financial services. . Download the free report to find out what it will take for challenger banks to develop a meaningful share of the banking market. get the state of challenger banks report. First name. Company Name.

The conference holds an impressive line up of education and activities for financial leaders focused on developing a strategic point of view and prospective roadmap to lead their organizations into the future: Reshaping the customerexperience with new business models supporting an integrated ecosystem-based marketplace.

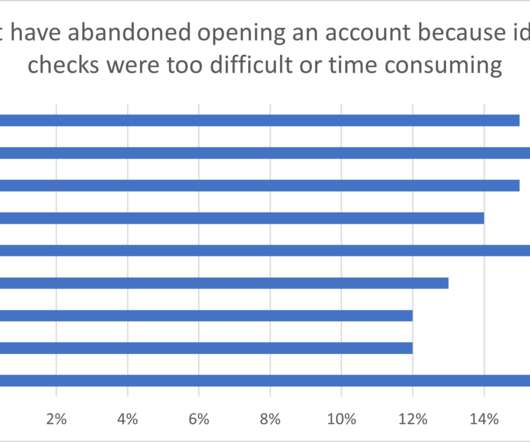

Delays in the account opening process are often caused by fraud and security considerations. Either the checks needed to set up an account introduce friction, or suspicion of fraud stops the process while additional checks are made. Customer Protection vs. CustomerExperience. Failure to Launch.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content