This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Banks that focus on the customerexperience have come to learn that it is not the forward-facing customerexperience that matters, but the “total experience” that now counts. Total experience is the business strategy for creating superior customer AND employee experience. Build from there.

Another important 2021 trend will be an increased emphasis on the customerexperience, providing a seamless, easy to manage and personalized journey at every step. To deliver that kind of experience, companies must go beyond the traditional approach to identity, which has been focused on usernames and passwords.

In short, while 2017 was the year of payments disruption, 2018 will be the year of the satisfied customer. The newest PYMNTS eBook is full of expert insight into the future of B2B payments, from commercial cards to accounts receivable. Download and read the full eBook here. That doesn’t just mean consumers either.

The rapid rise of scams and other crimes, as well as the increasingly diverse methods used by fraudsters, has only increased the pressure for banks to protect customers from scammers and detect early signs of fraudulent behaviour. A far more complex and increasing concern for risk and fraud managers, however, is authorised push payment fraud.

However, poor customerexperiences—particularly if they delay deposits—can compel RDC clients to take their business elsewhere. This eBook makes the case for outsourcing RDC operations to a proven managed services partner.

Following the highly successful The 11 Commandments of Digital Banking eBook , we are kicking off a series of 5 deeper dive blog posts that group the 11 commandments below into common themes. Many enterprises have succumbed to the inclination to digitize everything, which by default leads to cold, clinical experiences.

Ryan Frere, executive vice president and general manager of B2B for Flywire , believes that embedded finance in B2B is key to payments optimization in 2021. We are seeing payments become an inextricable and largely invisible part of customers’ experiences with different product or service providers.

In " A Look Forward: What Executives Wish for America and the World in 2021 ," Doug Brown, senior vice president and general manager, NCR Digital Banking , discusses how financial institutions should evolve to remain relevant and build customers' trust. Data and personalization was the key to helping customers in 2020.

Matt Redwood, head of self-service at Diebold Nixdorf , contributed the following piece as part of PYMNTS’ 2018 year-end eBook. As they open new stores, they do so with a complete mentality change and a much more diverse approach to the customerexperience and self-service.

Last year we published a highly successful The 11 Commandments of Digital Banking eBook that introduced the 11 commandments: Digital lift-and-shift is not a strategy! Unintentional or unnecessary friction in the customers’ experience is always bad – however, friction itself is not inherently evil. Respect the data.

Banks must be prepared to help stop scams, including making customers more aware of the danger, all while continuing to ensure an exemplary customerexperience. FICO published our 2021 Digital Consumer Banking and Fraud Survey today that emphasizes consumer perspectives on customerexperience and fraud prevention management.

Banks must be prepared to help stop scams, including making customers more aware of the danger, all while continuing to ensure an exemplary customerexperience. FICO published our 2021 Digital Consumer Banking and Fraud Survey today that emphasizes consumer perspectives on customerexperience and fraud prevention management.

They are also trying to enhance the customerexperience. Younger customers prefer to use a kiosk.”. In 2016, for example, Amazon began running pop-up kiosks for Kindle eBooks in convenience stores around the Seattle area, GeekWire reported. Wendy’s is hardly alone.

Retailers are] seeing it not just as a process to be managed, but as an opportunity. The right platform will allow them to combine layers of security — like tokenization, biometric authentication, PINs and back-end fraud management — to achieve the right balance of security and usability. Want to know the other two? contact-form-7].

Some 82 percent of users said they would cancel if the free two-day shipping were discontinued, according to research released by behavioral marketing platform SmarterHQ — which means fast delivery is more important to subscribers than other ancillary Prime services, including photo storage, music streaming and eBook privileges.

Key to providing acceptable customerexperiences is the way in which banks verify that applicants are who they say they are. Identity verification, required to prevent fraud and meet eKYC regulatory requirements, can also be the one that introduces friction and causes customers to abandon applications.

You can read more about all the UK survey results in our Digital Consumer Banking and Fraud Survey – UK Results Ebook . This is creating a challenge for banks, which need to walk the line between stopping scams and enabling a smooth customerexperience during financial transactions. by Matt Cox.

This is where specialist financial services partners can help their clients by partnering with them to deliver an effective customer communications strategy and ensure they remain competitive. So, what are the problems that require a compelling customer communications strategy, that partner technology providers can help their clients solve?

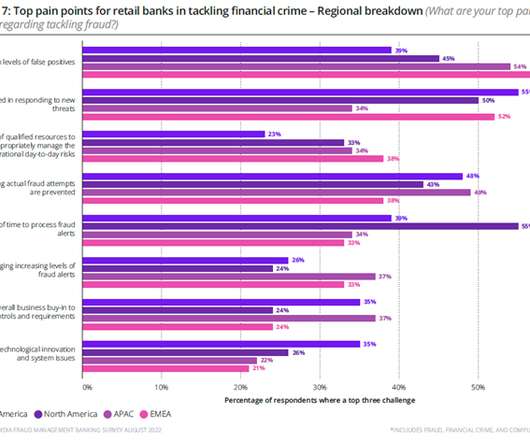

In August 2022, we commissioned a survey of 156 global executives and managers from retail banks and retail financial institutions. One of the key themes that we saw in the results is the continued investment in enterprise fraud management systems. Pain Points in Fraud Management Vary by Region. FICO Admin. by Andrew Manuel.

Product teams, business models and customer development strategy were all challenged in the last year as adaptation became the name of the game. The most popular posts in our Customer Development category dealt with digital banking, optimizing credit line increases, loan pricing and machine learning for credit risk models.

Following the highly successful The 11 Commandments of Digital Banking eBook , we are kicking off a series of 5 deeper dive blog posts that group the 11 Commandments below into common themes. Financial institutions have access to a lot of data – from customers themselves, third-party organizations, meta data, and many other sources.

One of the most interesting takeaways for me is that banks have an opportunity for proactive, personalized customer communication, in the channel of their choice, to provide fraud detection and fraud prevention, as well as to manage fraud cases so that they can be bought to a conclusion more quickly and with a better customerexperience.

Following the highly successful The 11 Commandments of Digital Banking eBook , we are completing our series of 5 deeper dive blog posts that group the 11 Commandments below into common themes: Digital lift-and-shift is not a strategy! Do the work for your customers; don’t pass the work along. Friction – not inherently good or evil.

And finally, operationalizing the insights at scale to create bespoke, “in moment” customerexperiences. It connects, strengthens and binds a bank’s existing data and systems, enabling the consolidation of all streams of customer data into an agile, data-driven framework that produces more personalized and actionable insights.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content