This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Socialmedia engagement plays a central role in modern restaurants’ daily business, with eateries using platforms like Facebook, Twitter and Instagram to advertise new menu items, interact with customers and drive business to their locations and mobile apps. SocialMedia Schemes.

It can be difficult these days to remember the almost idyllic promise of socialmedia when it first entered the general consumer consciousness. That’s not to tempt one into nostalgia, or to suggest that socialmedia has become marred beyond recognition. Fraud Increases. Digital Evolution. trillion in 2018.

Materials, training, and fraud also contribute to bank expenses. These can come in the form of email, in-app notifications, digital ads, organic content, socialmedia, and digital retargeting campaigns. The loss liability for the consumer is the same ($50) on both debit and credit if debit card fraud is reported within two days.

Fraud protection specialist Kount and Philadelphia-based payments platform FreedomPay are teaming up to offer “an integrated, complete solution to enable international expansion with fraud-free payments and frictionless customer” experiences. Before, they were limited to one or two areas.

Consumers are using mobile apps’ order-ahead features and loyalty perks more often during the COVID-19 pandemic, yet chargeback fraud — also known as friendly fraud — is unfortunately also rising. Chargebacks were originally instituted as a last resort for customers, but they have gained popularity alongside digital commerce.

Fraud attacks’ frequency and complexity will likely continue to rise despite merchants’ best efforts to prevent them. The Latest Fraud Decisioning Developments. The United Kingdom’s RELX , an information and analytics firm, has meanwhile purchased fraud prevention firm Emailage to boost its own anti-fraud efforts.

The latest Payments And The Platform Economy Playbook examines how marketplaces are using technologies like AI to innovate the customerexperience. Much has been written about artificial intelligence (AI)-powered tools for fraud detection and security. What else can it do, though, especially for online marketplaces?

With its new importance as a revenue stream, mobile ordering is driven in part by reviews and the exchange of customer data. Where you find customer data, you also find cybercrooks. A solid fraud prevention solution is a QSR’s first line of defense against card testing attacks.”. Securing Social for the MOA Future.

Can data make all the difference in the fight against payments fraud? The discussion played off the findings of a new whitepaper from the firm titled, “Driving Up Conversion with Effective Fraud Management.”. What works in preventing payments fraud at a large airline or telco system may not be germane for an electronics retailer.

In the August edition of the Payments And The Platform Economy Playbook , PYMNTS examines how marketplaces are using technologies such as artificial intelligence (AI) and mobile payments to innovate the customerexperience. Fraud remains an ever-present challenge, however, and marketplaces worldwide are deploying new defenses.

This is the first in a series of articles in which we tackle some of the most topical fraud issues and decisions facing fraud managers today. Not only is the customerexperience diminished, but in these days of socialmedia, the disgruntled customer may take to Twitter or Facebook to vent their frustrations.

If they have a complaint, for example, they expect to get a response via socialmedia within minutes, while the idea of waiting up to five working days for an application to be processed is completely alien to many. A real-time insight into experience. But what does this mean for the banking sector?

The result is a slew of unstructured data coming in from a variety of sources; financial service providers must try to make sense of it in order to maintain regulatory compliance and mitigate the risk of fraud. A Better Business CustomerExperience. Middesk aims to help these firms streamline and digitize this process.

Fraud protection has never been taken lightly by call centers, but the need for stricter authentication is reaching new levels in the face of automated bot attacks and near-daily account takeover (ATO) attempts. Many customers still like the convenience of KBA tools, however, which is why Lindsay Sacknoff, head of U.S.

Unlike the other public cloud providers, Oracle has top-rated Cloud applications for ERP, Supply Chain Management (SCM), Human Capital Management (HCM) and CustomerExperience (CX). Prebuilt Analytics Leveraging Oracle Cloud SaaS Applications – this is a differentiator between Oracle and the other public cloud providers.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Opportunity #2: When customer satisfaction is on the line.

As we explored in the first part of this two-part guide, digital banking fraud is an escalating threat to financial institutions and their customers. Digital banking fraud can take many forms, such as identity fraud and account takeover , which are becoming increasingly common. million in 2016. million in 2016.

billion due to fraud in 2016, and a significant portion of that stems from chargeback fraud. According to LexisNexis , chargeback fraud accounts for 28 percent of all fraud that occurs at an eCommerce company, tied for first place with “ friendly fraud.” Compromise Security For CustomerExperience.

Synthetic ID fraud can be especially hard to spot. Using real credentials lends authenticity to these schemes and allows them to elude many fraud detection systems, and cybercriminals can avoid tipping off victims by not using pilfered identities wholesale. Reducing false positives thus requires FIs to dig deeper for more insights.

Banks must enable fast and seamless onboarding experiences, but these processes should also be secure. New account fraud is a significant problem for FIs, with 48 percent of values generated from fraud attempts coming from accounts that have only been open for one day, according to a recent report.

Data holds the key to helping modern enterprises develop effective anti-fraud strategies. Many businesses are sitting on massive troves of it, but they are also facing down the three “V’s” of data complexity — velocity, variety and volume — which can make tackling fraud even harder. . Structured Versus Unstructured Data.

As Bise pointed out, not only does this strategy aid in improving the overall customerexperience and reducing risk, but it also allows companies to keep pace with the changing customer acquisition landscape.

Reports have appeared all over socialmedia, particularly via Reddit and Twitter , about Chipotle user accounts being pirated, with hundreds of dollars’ worth of food ordered to customer cards that those customers never saw. Are the customers wrong? So, what’s going on? Is Chipotle? Multiple Weak Points.

Some financial institutions have recently converted core systems, but they haven’t seen material improvements to their customerexperience or efficiency. In addition, with socialmedia users ready to expose any impact to customers, financial institutions are anxious about taking undue risks in a core systems project.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Opportunity #2: When customer satisfaction is on the line.

While these rules were derived from improving time-on-task, they can enhance bank performance no matter what metrics a bank uses for customer, employee, or total experience (the combination of employee and customerexperience). Design or pick the fastest customerexperience.

The latest Payments and the Platform Economy study examines how marketplaces are responding to the counterfeit threat as well as how they are continuing to innovate the customerexperience. trillion by 2020, which has prompted some online marketplaces to work on resolving fraud repercussions. SocialMedia.

Top 5 Surprises from FICO’s Fraud and Digital Banking Survey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. A report released by the FTC in February 2022 indicates a 71% increase in fraud in 2021, which cost consumers roughly $5.8

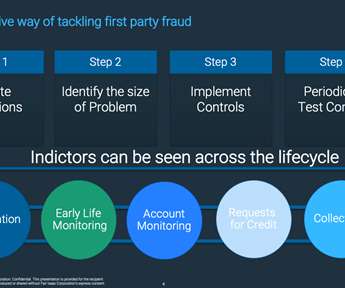

What Is First-Party Fraud? From banks to telcos to debt collection agencies, what looks like unrecoverable bad debt may in fact be first-party fraud. For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. by Matt Cox.

The firm’s gMobile solution, which helps authenticate users and delivers real-time risk analysis across mobile channels, debuted late last year, and McAlear said that the platform “enables delivery of a frictionless customerexperience, requiring no additional customer input, scripting or burdensome software downloads.”

The study came up with Reputation Scores, measured on a scale of 100 to 1,000, based on online reviews, accurate listings, socialmedia, search results and customer engagement. Samy also explained how mobile is the key in creating an omnichannel banking experience. banks, the banking industry was found to be lacking.

For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. Perhaps surprisingly, consumers sometimes use their own personal information to commit fraud. Both of these crimes are first-party fraud.

Fighting fraud. For the banking sector, one of the most appealing promises big data holds is its ability to transform their fraud detection and prevention activities. Enhancing the customerexperience. But careful considerations will need to be made about the ethics of this. ” The changing regulations. .”

Sure, trust generally revolves around concepts of security, privacy and fraud prevention — of trusting a merchant or payment services provider to not allow the theft of one’s personal data. But trust is so much more in this new age of omnichannel experience, according to what Parsons told Webster during the PYMNTS webinar.

It’s much harder to get it back or stop or fix a fraud attack after it’s happened.”. In order for both the bank and its customers to feel comfortable with real-time transfers, Vancini and his team have worked to offer new security methods. And, Vancini said, being plugged in is a good thing, at least as far as security is concerned.

To adapt, let alone thrive, businesses with store locations must embrace EMV, the latest in payments security and authentication, especially considering the retailers themselves have taken on more responsibility for fraud after 2015’s liability shift. The challenge for the last year has just been educating our customer base.

Indeed, a recent survey by Accenture found that in the UK, the likes of online retailers, tech firms and socialmedia companies have a lot of work to do if they are to convince customers to share their details.

5 Ways Digital Payments Will Change FIs and Fraud in 2023. Financial institutions (FIs) are not letting fraud trends like scams fade into background noise, but fraud awareness is rising among customers and both the banks and customers are eager to mitigate as much as possible. FICO Admin. Tue, 07/02/2019 - 02:45.

In 2015, the financial industry made a point to enhance the customerexperience by leveraging massive amounts of data from phone calls, emails, mobile apps, ATMs, and websites. For instance, analyzing Twitter comments posted by customers regarding their experience at the branch offers rich data sets. Advanced Analytics.

FedEx CrossBorder , the recently rebranded BONGO business unit, is all about helping merchants make the most of the cross-border opportunity – and to enable payment for goods purchased while staying on the right side of fraud, risk, tax, and regulatory and legal compliance. How FedEx CrossBorder Works.

It is an appropriate way to describe the nirvana of the commerce experience, one in which consumers and merchants make sales without friction, and remove fraud and risk without introducing friction at checkout. For good reason, too. The Commerce Journey In Context.

According to recent reports: One in three UK adults - and half of 18-24 year olds - said they checked their phones in the middle of the night, with instant messaging and socialmedia the most popular activities. The last thing you want is for your fraud alerts to be hijacked. appeared first on FICO.

In the 2023 FICO Global Scams Survey , we asked consumers worldwide what they think banks could do better to combat scams and create a better customerexperience for victims. Their top five responses provide a blueprint of customer-friendly steps banks can take to counter RTP scams and improve customerexperiences when scams occur.

The conference holds an impressive line up of education and activities for financial leaders focused on developing a strategic point of view and prospective roadmap to lead their organizations into the future: Reshaping the customerexperience with new business models supporting an integrated ecosystem-based marketplace. Get social.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content