This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The rising trend of digitization in commerce and the increased occurrence of card-not-present fraud were not created by the COVID-19 pandemic. Those dynamics have made the dangers of fraud far less abstract to consumers. Fraud, he said, is occurring at an unprecedented rate and scale and it was far from a small issue before.

With digital transactions and eCommerce soaring during the pandemic, the rate of increasingly sophisticated fraud has also risen. Unlike the crypto markets, Wingert said the banking and payments industries continue to be slow to adapt to the challenges of KYC and fraud prevention. In fact, a recent GeoGuard survey found that U.S.

One recent study estimated that roughly 44 million Americans would tap food delivery apps by the end of this year, up from 38 million in 2019, and another survey predicted that the number of smartphone delivery app users will climb 25.2 It also analyzes how focusing on the customerexperience can help prevent such fraud in the first place.

Forty-four percent of 200 millennials surveyed last year stated they were wholly responsible for making purchasing decisions at the B2B companies at which they worked, and an additional 33 percent played some role in this process. trillion by 2020, but new sales channels also invite emerging fraud forms. Detecting Fraudsters.

The number of real-time payments has risen dramatically in recent years, and APP fraud has grown alongside it. Bad actors typically perpetrate APP fraud in several ways. APP Fraud Ramps Up. Instances of APP fraud around the globe have continued to rise as real-time payment rails extend their reach.

The prevalence of online commerce opens new doors for digital fraud, however, both from career fraudsters and opportunistic customers. Phishing scams were on the rise all year, while a survey of online shoppers found that 40.3 Developments F rom The World Of Digital Fraud. Developments F rom The World Of Digital Fraud.

Popular use cases include request for payments using the instant payment rails (above), loan payments and transaction verification to prevent fraud. Marketing and Promotions : Banks can create visually appealing and engaging promotional content, including videos and images, to capture customer attention and drive engagement.

A two-headed monster of rising churn and rampant fraud is menacing the growing subscription space, and many companies are spending big bucks to roll out innovative fraud-busting technologies to combat it. Placing Big Bets on Customer Knowledge .

A new survey has found that the biggest obstacles hindering online retailers from doing business abroad is fraud prevention, and currency and payment processing. In fact, North America’s top 1000 eRetailers have sold $143 billion worth of goods to customers outside the U.S.,

Consumers are using mobile apps’ order-ahead features and loyalty perks more often during the COVID-19 pandemic, yet chargeback fraud — also known as friendly fraud — is unfortunately also rising. Chargebacks were originally instituted as a last resort for customers, but they have gained popularity alongside digital commerce.

When it comes to deploying corporate resources in the battle against online fraud and account takeovers (ATOs), all too often, guiding principles fail to spot what’s really happening to a business in real time. The rule of thumb here is that after committing account takeover fraud, those fraudsters lie in wait before using the stolen account.

Banks are increasingly embracing new channels to offer seamless omnichannel services to their customers, but doing so often creates silos that handle large amounts of collected data. Fraud orchestration can help solve this issue as it allows banks to build holistic fraud prevention defense systems and gain 360-degree views of their customers.

The last few years have thrown up many challenges for banks and card providers as everything has shifted online, one of the primary challenges being fraud scams. But the online shift has also created opportunities for financial institutions to demonstrate their strong fraud controls in the digital space.

Banks’ use of such innovations is predicted to expand, too, with 60 percent of FIs saying they aim to gain customers and improve customerexperiences using digital channels. This increased digital presence also brings a greater risk of digital fraud, however. The Fraud Threats Facing Digital-First Banks.

Digital fraud prevention company Kount is rolling out a complete solution to protect companies from criminal and friendly fraud, the firm announced in a press release on Monday (Oct. Kount’s digital fraud prevention uses artificial intelligence (AI) that mimics a fraud analyst.

Those include an anticipated wave of chargebacks from friendly fraud, and more serious cybercrime intrusions that also come with the sudden expansion of digital commerce. In another survey, 39 percent of consumers said they had utilized curbside pickup after the pandemic began — an increase from the 28 percent who did so previously.

ChatGPT is a powerful language model that can understand a variety of languages, including emojis, that can assist banks with increasing the productivity of bankers, improving their customerexperience, automating repetitive tasks, and providing personalized financial advice to customers.

Since the coronavirus outbreak, almost half of banking customers have reported changing how they interact with their financial institutions, leveraging new channels like online and mobile banking, according to an FIS survey. These findings are true among all generations surveyed. Fraud Prevention. learn more. Learn More.

When it comes to fraud, are people worried about the wrong things? New data suggest that people are concerned about fraud, but one of the biggest threats seems to be flying under the radar, at least for consumers. That threat is fraud scams – tactics and techniques that fraudsters are using to trick people into giving away their money.

ACI Worldwide advises that, as the world moves toward immediate payment ecosystems, a holistic view of the transaction, with layered controls from origination to the application of real-time rules, is the only way to push the pedal to the metal on faster payments and put the brakes on fraud. million in 2007 to £52.5

percent of FIs believe AI is an effective tool for stopping fraud before it happens, and 80 percent of AI-using fraud specialists believe the technology could reduce payments fraud. percent of banks in our survey equipped with genuine AI systems. Take just a few data points: 63.6 AI can also help to spot credit risk.

Banks must be prepared to help stop scams, including making customers more aware of the danger, all while continuing to ensure an exemplary customerexperience. FICO published our 2021 Digital Consumer Banking and FraudSurvey today that emphasizes consumer perspectives on customerexperience and fraud prevention management.

Banks must be prepared to help stop scams, including making customers more aware of the danger, all while continuing to ensure an exemplary customerexperience. FICO published our 2021 Digital Consumer Banking and FraudSurvey today that emphasizes consumer perspectives on customerexperience and fraud prevention management.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Ultimately, customers want to be known and valued.

Since the coronavirus outbreak, almost half of banking customers have reported changing how they interact with their financial institutions, leveraging new channels like online and mobile banking, according to an FIS survey. These findings are true among all generations surveyed. Fraud Prevention. learn more. Learn More.

Top 5 Surprises from FICO’s Fraud and Digital Banking Survey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. million consumer fraud and 1.4 FICO Admin. Tue, 07/02/2019 - 02:45. by Sarah Rutherford. expand_less Back To Top.

According to a recent survey , 90 percent of businesses now expect real-time payments – but, as with many innovations, there is a gap between expectations and reality. percent of surveyed AP professionals paid invoices via paper check. FIs do see the benefits, according to a survey by Citizens Commercial Banking.

Account takeovers (ATOs) are a growing source of pain for financial institutions (FIs) and their customers, with losses from these attacks rising 164 percent in 2018. FIs must adopt fraud-fighting measures that are robust but do not create so much friction that legitimate customers find it difficult to access needed services.

PYMNTS recently spoke with Luis Rojas, vice president of product management for Guardian Analytics , an online banking security firm, about the effect of a faster processing environment, the potential for increased fraud and how to mitigate that risk. The Mountain View, Calif.-based People are bracing for a similar spike here,” he added.

And for all the brilliant modeling, artificial intelligence (AI) and machine learning (ML) technology we have to throw at the problem of fraud, he said, the good guys are operating at something of a disadvantage when it comes to detecting the scams that are to come. It takes that long to get feedback from consumers on credit card fraud.

Creating more efficient operations and improving customerexperiences are the goals driving technology strategies and investments at many U.S. financial institutions, according to Bank Director magazine’s latest survey of CEOs, executives and directors for its 2019 Technology Survey. Fraud Prevention. Learn More.

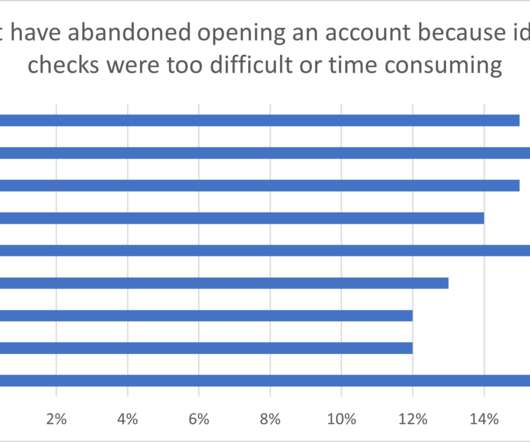

These customers want to be able to complete their transactions as quickly as possible, meaning the onboarding process must be swift and seamless to ensure they do not abandon it for faster competitors.

The new push notification functionality enables payment providers to effectively engage their cardholders with relevant and up-to-date account information strengthening the overall customerexperience.”. TSYS Alerts for Fraud also sends alerts about potentially fraudulent transactions and unauthorized usage.

billion due to fraud in 2016, and a significant portion of that stems from chargeback fraud. According to LexisNexis , chargeback fraud accounts for 28 percent of all fraud that occurs at an eCommerce company, tied for first place with “ friendly fraud.” Compromise Security For CustomerExperience.

To understand customers’ perceptions of what matters in digital banking including account openings, FICO recently commissioned an independent consumer survey of nearly 5,000 people across ten countries including: Brazil. To understand the statistics for the individual countries surveyed download the infographics: Brazil.

In recent years there has been much talk of the fraud and financial crime departments at banks working together more closely. FICO commissioned research and analyst company Ovum to carry out an independent research survey to uncover the main concerns and issues banks face when fighting fraud and complying with financial crime legislation.

Start with a survey and pre-planning meetings. The following steps can help narrow it down and focus your goals: Send out a simple, future-oriented survey to the board and executive management (read on for sample questions) to determine strengths, weaknesses, opportunities, and threats to your financial institution. Where are you now?

Does this extend to conumser experiences and perceptions around vehicle finacing? To answer that question (and more), FICO has released the findings from our second annual global consumer survey on vehicle finance perceptions. Close any customerexperience gaps. Keep doing what’s working.

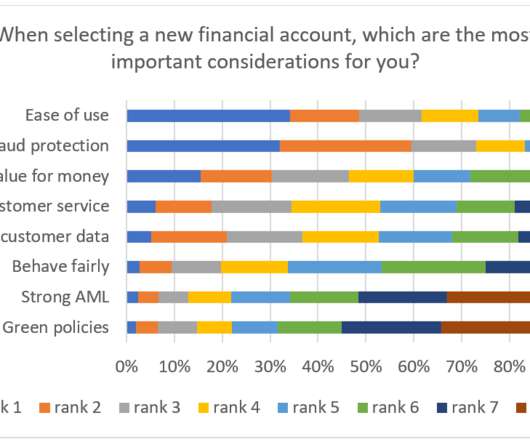

Biometric Security Crucial for Fraud Protection and CX. Because customers value ease of use and good fraud protection most, FIs must balance scam protection with making things easy for good customers – but not TOO easy. Customers Prefer Easy & Safe. Customers Resist Friction. FICO Admin. by Sarah Rutherford.

19) released a report, dubbed “Millennial Study: Privacy vs. CustomerExperience,” which charts the digital consumer preferences and behaviors of millennials in seven global markets — the U.S., ” said Kimberly Little Sutherland, senior director of fraud management at LexisNexis Risk Solutions.

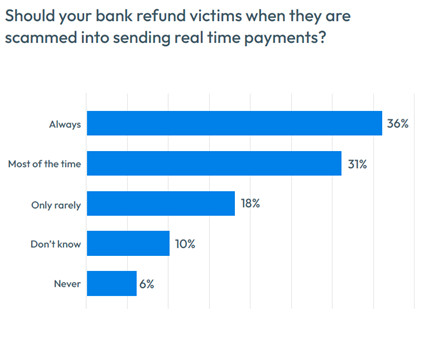

Home Blog FICO Survey: Do Customers Think Banks Are Fair to Scam Victims? According to the 2023 FICO Global Scams Survey , 51% of consumers worldwide believe their friends or family members have been victims of similar scams. In most cases, customers feel that banks should reimburse them when scams occur.

In surveying mobile card app usage for the December 2019 Bridging the Gap: Mobile Card App Adoption Report , PYMNTS found a vibrant, growing payments ecosystem. Just beneath the smartphone glass, brainy new tech is powering payments in ways that emphasize security and speed, while keeping one eye fixed on customerexperience.

Application Fraud – Does Canada Need a New Approach? FICO’s Fraud, Identity and Digital Banking Survey 2022 shows that customers in Canada want slick onboarding processes, where fraud controls work but don’t delay account opening. And what does that mean for the future of your fraud management solutions?

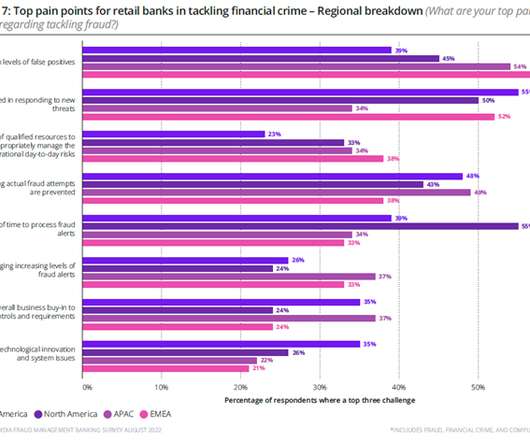

Enterprise Fraud Solution Buyers Want More Agility, More Data. Our recent global survey reveals the investment priorities and functionality requirements for enterprise-level fraud solution buyers. In August 2022, we commissioned a survey of 156 global executives and managers from retail banks and retail financial institutions.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content