This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

When it comes to deploying corporate resources in the battle against online fraud and account takeovers (ATOs), all too often, guiding principles fail to spot what’s really happening to a business in real time. The rule of thumb here is that after committing account takeover fraud, those fraudsters lie in wait before using the stolen account.

Among the highest ideals for digital payments – driving innovation in transactions and customerexperience – is, of course, the concept of seamlessness. The rule change is the subject of a recent whitepaper published by GIACT. That implies an ease of use while giving up nothing when it comes to security. New NACHA Rule.

But the global adoption of such schemes, alongside the problems suffered by early adopters, has turned the focus to real-time payments fraud. As discussed in my earlier post , real-time payments make multiple types of fraud more attractive and enable the fast movement and laundering of criminal proceeds. Who Is Liable?

As my colleague TJ Horan says in his post , the worlds of fraud and compliance are moving closer together. A critical meeting point for these disciplines is the identity proofing of customers, particularly using digital channels. This comes at a cost to customerexperience that means lost business and poor customer satisfaction scores.

Biometric Security Crucial for Fraud Protection and CX. Because customers value ease of use and good fraud protection most, FIs must balance scam protection with making things easy for good customers – but not TOO easy. Customers Prefer Easy & Safe. Customers Prefer Biometric Security. FICO Admin.

Before getting started, CSPs should determine who “own”’ and is accountable for subscription fraud. Is it the fraud team? Also, is there a clear and agreed fraud risk appetite that has exec sponsorship and is agreed by all stakeholders? In part, this is due to the ever-changing nature of fraud. Credit risk?

Real-time decisions come with many benefits – with enhanced customerexperience and improved business functions among them – but getting there isn’t easy. “As Innovation through analytics drives business performance, growth, customer satisfaction and bottom-line results.”. BYPASSING THE REAL-TIME ROADBLOCKS. contact-form-7].

What Is First-Party Fraud? From banks to telcos to debt collection agencies, what looks like unrecoverable bad debt may in fact be first-party fraud. For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. by Matt Cox.

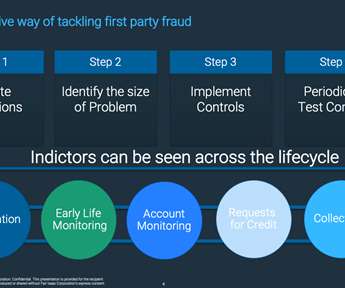

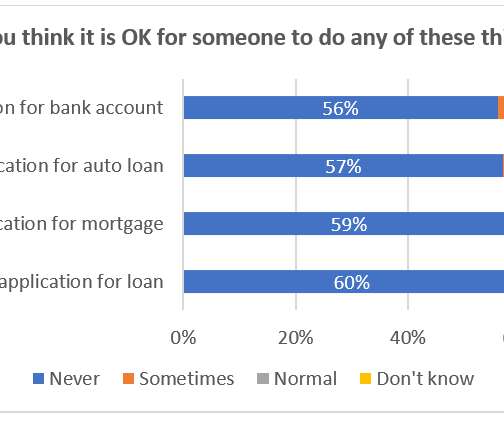

First-Party Fraud Must Be Stopped Across the Customer Lifecycle. Financial institutions face first-party risks “inside the wire” - 14% of customers worldwide think it is normal to exaggerate income on a mortgage application. Another data point demonstrates how customers view the commission of similar types of fraud differently.

For many people, the word “fraud” evokes images of shadowy criminals using stolen identities and purloined credit card information to commit financial crimes. Perhaps surprisingly, consumers sometimes use their own personal information to commit fraud. Both of these crimes are first-party fraud.

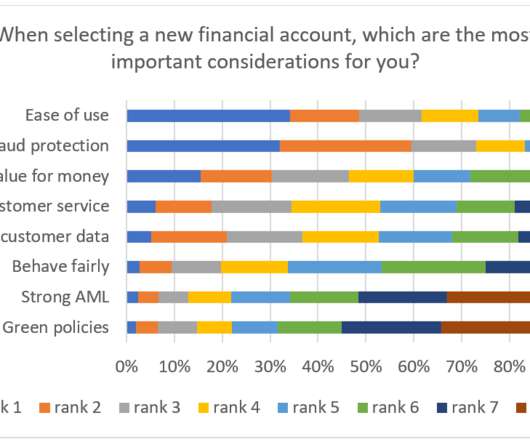

Top 5 Surprises from FICO’s Fraud and Digital Banking Survey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. A report released by the FTC in February 2022 indicates a 71% increase in fraud in 2021, which cost consumers roughly $5.8

The reduction of onboarding timelines from days to minutes is only the start of the benefits, those additional benefits including: Increased accuracy in detecting merchant fraud and default. Improved the customerexperience, resulting in accelerated business growth. Reduced portfolio risk and lower costs.

They offer chat bots for customer support, with the ability to create custom bots. One use case is to use a bot, via text messaging, to help customers when they have potential credit card fraud. They use Natural Language Processing algorithms for the customer interaction. Qumram – @QumramAG – [link].

From my understanding of their offering they let mid to large financial planners/consultants utilize state-of-the-art data tools in real time coupled with NLQ AI for a better customerexperience, allowing a financial planner to do a better job for more clients in less time. This is a very sophisticated fraud detection technology! ^SR.

Transforming the CustomerExperience: Telecommunications. Telecommunication providers have access to massive amounts of customer data, which can be leveraged by analytics to drive smarter, more personal customer decisions and offers,” noted Tim VanTassel. Here are our top 5 posts from 2020. #1.

I like the idea but I am a bit concerned about the potential for fraud from both companies and investors. Addresses compliance, fraudexperience and customerexperience analytics. Customers want self-service capabilities but regulation and risk is top of mind that get in the way of digital interactions.

Started talking about the challenge of having to change credit cards all the time (due to fraud). We are the global leaders in identity solutions while protecting FI’s and providers from compliance and fraud.” Download our latest whitepaper that discusses what it really takes to develop a successful Fintech startup.

03:04 pm Experian Fraud & Identity – https://www.experian.com/decision-analytics/identity-and-fraud/fraud-and-identity.html – @Experian – Adam Fingersh – GM and SVP, Fraud and Identity Solutions & John Sarreal. Also a pretty good customerexperience. Demo: Bank application form.

Note for you damn haters: yes, it’s down from a frothy high of $66,0000, but look at the normalized return over the past 15 years since Satoshi Nakamoto’s whitepaper.) The Smarter Bank – CustomerExperience Award – goes to Synovus Bank. The laser eyes are shining brighter going into 2024.

Companies are turning to accelerators, funds, and labs to try to find the next big thing that will reduce fraud, speed up transaction times, and catch on with consumers. The lab aims to improve banking through better uses of technology and has a serious focus on customer participation as the best way to find solutions. Founded: 2010.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content