This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The most significant problem with bank innovation is that bankers see or hear about a sexy piece of technology at a conference or at another bank and then acquire it. The new piece of technology ends up solving a known problem but, in the process, creates more problems, and risks, than it solves.

For example, in the next year, does the bank want to focus on making its employees more productive or enhancing customerexperience. This use case not only has a direct impact on employee time savings and an easily calculated return on investment, but it allows employees to get comfortable with the technology.

is staking its consumer-banking strategy on digital technology. Three of the group’s top leaders — the chief executive officer, the head of digital technology and the chief of digital customerexperience — have moved to new roles or […]. JPMorgan Chase & Co.

based bank with $273 million in assets, is using ‘cash sweep’ technology to gain large deposits from public funds without having to put up its own assets as collateral. Bank of Franklin County, a Washington, Mo.-based

As banks continue to explore best practices around handling customer data, insight from core technology provider Fiserv suggests open banking can help banks compete with fintechs and large incumbents alike. “By

Smiley Technologies, a core banking provider focused on community banks, is trying to help its bank clients secure larger deposits by partnering with deposit technology company Reich & Tang.

For TD, it has meant turning its cybersecurity centers into technology “war rooms” to handle the rapidly changing needs of customers facing a new reality.? The coronavirus pandemic has forced many bankers and bank processes to pivot in unexpected ways.

The program has 10 courses in topics including business finance, digital marketing, and innovationstrategy. Gender diversity is an essential component of delivering elevated business strategies. As part of the initiative, Goldman Sachs developed a free online business education program available to women globally.

Banks are accelerating their technology projects in light of the coronavirus pandemic. Whether its Happy State Bank pushing out video teller machines or TSB Bank launching a virtual assistant in five days, banks are trying to find new ways to connect with customers during times of social distancing. Legacy banks in the U.S.

Great Southern Bank is using lending technology from the cloud banking vendor nCino to increase efficiency for commercial and retail loan officers. “We

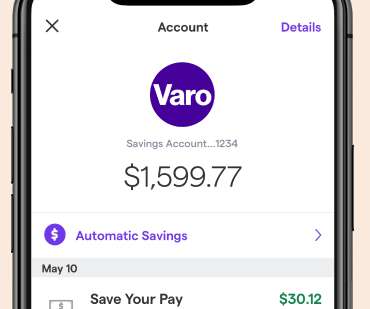

As Moven begins shutting down its consumer-facing businesses, the digital banking platform is funneling its customers to Varo Money.? We are excited to welcome their customers and deliver on the types of technology and features they have grown to love,” said […].

With the novel coronavirus forcing employees to work from home, banking technology and security infrastructures are being put to the test.? Today, if you are not a frontline employee, you are working from home,” said Jason Shields, vice president and loan operations manager at Gulf Coast Bank, which is based in New Orleans.

Nova Credit, a startup whose technology helps banks underwrite immigrants, is growing its auto finance and mortgage offerings. The San Francisco-based company, which partners with such large institutions like American Express, allows institutions to pull foreign credit data to develop U.S.-equivalent

Earnest, a student loan startup that was acquired by the student loan servicing company Navient in 2017, is turning to industry associations to boost customer acquisition.

Banking technology company Finastra is enhancing the rollout of its customer data strategy as clients face new competition. Her mandate is to help client banks and institutions use customer data more effectively, allowing them to build […].

WWS solves major industry challenges such as improving self-service security or enhancing the retail banking customerexperience of digital self-service banking. Q: What can organisations do to improve the security of the ATM ecosystem and enhance the user experience at ATMs?

The eight-year-old company is working with banking technology giant FIS to reach new financial institutions. While third-party personal finance apps have garnered attention through direct-to-consumer offerings, HT Mobile Apps is looking to reach more users by offering savings and financial literacy tools to partner institutions.

Bank Innovation has hand-selected 10 companies to participate in its DEMOvation Challenge at Bank Innovation Ignite, which runs from March 2-3 in Seattle. The companies focus on a variety of use cases including customer acquisition, loan underwriting technology, conversational AI, fraud prevention, and other digital capabilities.

Depending on where you look, the chasm yawns wide when it comes to innovating with new technologies or features. In a PYMNTS interview with Karen Webster, Joe DeRosa, EVP of Global Sales at i2c , discussed the findings of the July 2019 Innovation Readiness Playbook , subtitled “Leveling the Playing Field for Different-Sized FIs.”

Banks need to embrace new customer acquisition models or risk falling behind, a recent Accenture report argued. The report, titled 5 Big Bets in Retail Payments in North America, examined how banks risk losing payments revenue to technology startups and other non-bank competitors.

In today’s post pandemic world, the need for innovation at pace and scale is leading to the growing adoption and expansion of partner ecosystems to support the delivery of innovations to both customerexperiences and process improvements. Cisco in the evolving ecosystem.

This year, Fiserv is nominated for yet another PYMNTS Innovation Project award, this time for the NACHA Best Innovation in ACH Award. “We’re at a really exciting time in financial services, where there are so many examples of fantastic innovation around the market,” he recently told PYMNTS.

When you think of technologies that are changing the way the banking industry conducts business, is your first thought chatbots? Helping keep these memories blissfully distant is conversational computing technology. How well does the product vision align with its buyers’ need to win, serve, and retain customers?

The post 4 Ways to Improve Bank and Credit Union CX Without Technology appeared first on The Financial Brand. Digital transformation is not solely a tech and data challenge. Retail bankers must first address the essentials, including journey mapping.

The company told Bank Innovation it wants to eliminate cost as a barrier for smaller banks and credit unions to sign up for the service. Barwick Bank, meanwhile, is using technology from Finastra to create brand new digital channels. The bank currently […].

The tech-focused market research company Forrester recently reported in “The New Unstable Normal: How COVID-19 Will Change Business and Technology Forever,” that the effects of the pandemic could be permanent. As the COVID-19 pandemic alters the world, financial services are reacting in turn. In the short term: 1.

Digital banking engagement leads to more customer data and better customerexperiences, which leads to greater loyalty and higher profits. The post The Future of Loyalty in Banking is at Risk appeared first on The Financial Brand - Banking Trends, Analysis & Insights.

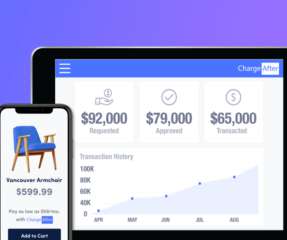

Visa and point-of-sale lending technology startup ChargeAfter announced yesterday a pilot of their installment loan solution for select merchants in the United States.

The former investment banker and fund manager has set up 1fs:Wealth, a London-based technology firm that aims to help family offices and rich individuals manage their assets. Bobby Console-Verma isn’t letting the pandemic slow down his business plans. He plans […].

Financial services ranked 11th out of 15 industries when it comes to emotionally connecting with customers. Citizens Bank, meanwhile, is transforming its technology core through a data-driven personalization engine. This week, MLBM released its 2020 Brand Intimacy Study.

Technology is starting to unlock things that have traditionally sat on the balance sheet of banks and put them into institutional investors’ hands,” said Ed Mallon, […]. Pagaya, a four-year-old fintech that uses AI to guide institutional investing, announced a $102 million Series D today.

Credit unions are rejecting some of the big core providers and instead choosing startups to overhaul their technology. based banking software company Bankjoy has grown its customer base by 50% since the start of the pandemic. Royal Oak, Mich.-based Point-of-sale lending, meanwhile, is continuing its rapid growth trajectory.

The integration of finance and digital technology has resulted in exponential growth of digital banking and fintech solutions. The post Digital Finance Penetration Surpasses That Of Social Media appeared first on The Financial Brand - Banking Trends, Analysis & Insights.

Banks and credit unions must rethink the definition of ‘digital banking’ and prioritize investment in data, technology, people and processes. The post Top Digital Banking Transformation Trends for 2021 appeared first on The Financial Brand.

Technology and evolving consumer views could unravel the business model of financial institutions but also provide new avenues for growth. The post How Partnerships and Societal Changes Are Radically Altering Banking appeared first on The Financial Brand.

Banking industry underestimates the impact of technological changes and increasing customer expectations says Brian Solis. The post Digital Darwinism Puts Banks and Credit Unions at Risk appeared first on The Financial Brand.

Google's abandonment of Plex digital-only banking should not bring comfort to traditional banks that are slow to respond to neobank offerings. The post Traditional Banks Remain Unprepared for Digital-Only Challengers appeared first on The Financial Brand - Banking Trends, Analysis & Insights.

The key to digital banking survival will be the ability to transform to a new digital reality with a foundation of data and analytics. The post 6 Keys to Digital Banking Transformation Success appeared first on The Financial Brand - Banking Trends, Analysis & Insights.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content