This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The reality is that banks don’t think from the customer’s perspective enough. The customerexperience is horrible for many bank processes. Not understanding your customer can lead to a brand and products misaligned with the customer’s needs resulting in an erosion of a bank’s competitive position.

The reality is that banks don’t think from the customer’s perspective enough. The customerexperience is horrible for many bank processes. Not understanding your customer can lead to a brand and products misaligned with the customer’s needs resulting in an erosion of a bank’s competitive position.

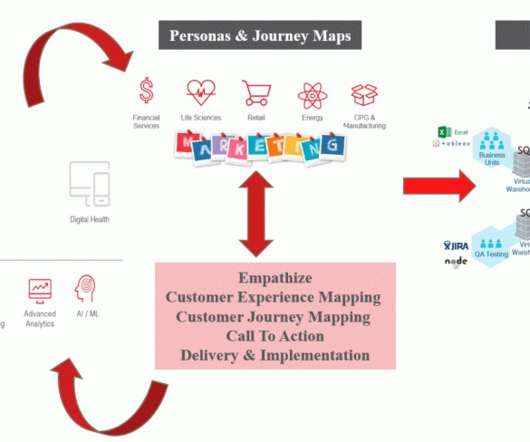

It affects decision making on everyday basis which does not let these enterprises provide value to their customers in an efficient manner. We at Perficient leverage CustomerExperience Mapping the most. What is Phase 0 in terms of CustomerExperience Mapping for our customers? Training and Enablement.

Additionally, training staff to effectively use RCS can incur additional expenses. Tutorials and guided tours can help customers navigate online banking platforms on the go. Conclusion As marketing technology continues to evolve, banks are constantly seeking innovative ways to enhance customer communication.

The financial services industry has made major strides in amping up its overall customerexperience game; however, there is still a deficit in the personalization and accessibility of products and services for many Americans. Interested in discussing how you can improve your financial institution’s customerexperience?

When done correctly, chatbots increase efficiency while also delivering better customerexperiences. While there are OEM-to-dealer complexities to consider, this AI advancement can help solve challenges automotive companies and their customers face every day. Online Purchase Completion.

Materials, training, and fraud also contribute to bank expenses. Manage Active Declines Debit card transactions that are declined ends up hurting the customerexperience and costing the bank valuable time in managing. Not having sufficient funds is the largest reason for card declines (about 35% of all declines).

As Walmart aims to grow profits at its online shopping business and cut discord between units, the retailer is bringing together its store and eCommerce product-buying teams, The Wall Street Journal reported. Walmart has long had different store and online shopping teams. web and store businesses. web and store businesses.

As COVID-19 continues to modify ideas around how we shop and pay, consumers and B2B buyers are also making choices about where to shop: online or in-store? Retailers in this environment must do more to imbue in-store shopping experiences with the sense of control, convenience and safety consumers have come to expect when purchasing online.”.

While a very real glass ceiling might be under assault in the political field, online-only brands that eschewed traditional methods of starting up are seeing themselves approach a limiting barrier of their own kind. Rather than be held back, though, more than a few brands are proving strong enough to break through. ”

ChatGPT is a powerful language model that can understand a variety of languages, including emojis, that can assist banks with increasing the productivity of bankers, improving their customerexperience, automating repetitive tasks, and providing personalized financial advice to customers.

At 19%, community banks ranked only above credit unions in delivering customers that were “extremely satisfied with the outcome of their problems and a whopping 35% that were “not satisfied.”. Why Customer Problem Resolution Matters. Solving problems is central to customer service.

Online Rising. Well, it’s not really a surprise: online shopping. household spent $5,200 online last year, an increase of nearly 50 percent from five years earlier. And the report added that online shopping is expected to make up 25 percent of retail sales, with around 16 percent of overall sales made online.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Ultimately, customers want to be known and valued.

Does the Bank Technology Improve the CustomerExperience Across the Bank’s Platform? To answer the question above, ask yourself – “How does the product scale across the bank’s platform to various customer segments?” On a macro-level, it’s about managing your channels and your customer segments.

In that context, Julia Li, director at Baidu Research Institute USA , told Karen Webster, the part for artificial intelligence (AI) to play is obvious: Make the customerexperience much smoother and easier than before by stitching all of those discrete actions into something that is a smoother, “one-click” journey.

While these rules were derived from improving time-on-task, they can enhance bank performance no matter what metrics a bank uses for customer, employee, or total experience (the combination of employee and customerexperience). Design or pick the fastest customerexperience. The result?

But as the pandemic-driven digital shift gains traction, retailers have to be wondering if consumers will use websites to comparison shop for brick-and-mortar retail (webrooming) or whether they’ll go back to shopping retail to order online (showrooming). For the record, webrooming was beating showrooming in a survey conducted in late 2019.

It’s the trade-off between financial institutions (FIs) easing the consumer’s journey across banking and transactions done online, and the need to prevent fraud during new customer onboarding. Those predictors are then fed into trained models.” The models then return scores to the Socure/Alloy FI customers.

Retail banks need creative ways to excite their workforce and train them for the new banking experience Retail Banking Financial Trends Technology Customers Human Resources Feature Management Feature3 Fintech Mobile Online Tech Management Community Banking.

Takeaway 1 Implementing the FedNow Service can help reduce interbank obligations, expand market reach, and enhance customerexperiences. Essential components for connection include: Front-end services: Provide customers with online or app-based options to send and receive payments.

It uses a generative pre-trained transformer (GPT) model, a type of neural network trained on a massive dataset of text and code. Arguably the most important function of Data Cloud is that it helps clients unify their data from a variety of sources to segment customers and keep a close eye on their customers’ behaviors.

Another issue is the common “broken rung” women experience when trying to move up from an entry-level role to a managerial role; a woman who holds an entry-level role is far less likely than her male counterpart to be slated into a managerial position.

However, customers recently have come to expect more from businesses in terms of service, forming a landscape that’s saturated with options, and thus hyper-competitive. Many businesses now compete solely on the strength of their customerexperience. Twitter-based customer service increased 250% from 2015 to 2017.

And lastly, the chain offers something Green said he thinks will be critical to all of retail in the pandemic era: a better-curated, personalized experience for consumers. The pandemic pushed Indochino to add virtual shopping guides to its online channel, something the chain’s data revealed customers really wanted.

Takeaway 2 A consumer loan origination system can help FIs offer a fully digital retail lending experience. Takeaway 3 Enhancing the customerexperience means delivering on customer expectations with digital offerings. So, how will your financial institution set itself apart and be the one the customer chooses?

That means, among other tasks, helping to enable in-store retail associates to use the latest mobile technology — and that includes emerging 5G mobile network technology — to better serve consumers and offer a deeper customerexperience. Transforming Retail. It’s a great time to be transforming retail,” Levene said.

Jessica brings forward twenty years of customer service experience and recently received her Personal Training fitness certification. She hopes to use that experience in understanding the customers and client needs and to build products reflecting that expertise. Bright Paths Project: Couponista.

Salesforce Learning Cloud provides tools to help finance teams train and develop their employees. These tools and resources include: Onboarding and training. Salesforce provides a variety of tools and resources to help finance teams onboard and train new employees. Performance management.

Digital channels now allow most banking transactions to occur online anywhere and at any time—and at a much lower cost than face-to-face interactions in branches. Yet despite salesforce transgressions at a few retail banks, a human salesforce remains a critical asset in the fight to attract and retain customers.

Digital channels now allow most banking transactions to occur online anywhere and at any time—and at a much lower cost than face-to-face interactions in branches. Yet despite salesforce transgressions at a few retail banks, a human salesforce remains a critical asset in the fight to attract and retain customers.

At SouthState, our commercial lending teams use an online proposal generator, and we make that same app available to any community bank. Our online proposal generator is an easy-to-use tool that allows lenders to create, save, update, print, and share standard formatted PDF presentations with borrowers. Conclusion.

At SouthState, our commercial lending teams use an online proposal generator, and we make that same app available to any community bank. Our online proposal generator is an easy-to-use tool that allows lenders to create, save, update, print, and share standard formatted PDF presentations with borrowers. Conclusion.

The consumer demand for digitization and customer-centric banking is higher than ever. Despite the challenges that come with adopting new procedures, community financial institutions by their very nature have a notable advantage over online and alternative lenders when it comes to small business lending. Credit Analysis Training.

Simple, we will show, often leads to a better customerexperience, enhanced reliability, better profitability and clearer purpose. We have the mistaken belief in this industry that we should serve the customer in the branch, on the phone, on the computer and on mobile all with equal capabilities. This is a mistake.

The company allows online and offline consumers to purchase products with installation included, and then uses connecting technology to facilitate the assembly with an installation service provider. “It We have an onlinetraining center where they go in, watch videos and take tests.

Bank executives are coming to understand that in today’s world, the customerexperience (CX) is the product, although not all have made a serious commitment to address newfound competition. Experience design is a specific skillset that is needed to steer the execution of a bank’s digital strategy. Why Ownership Matters.

CEO Steve Easterbrook recently noted that the burger giant’s app adoption rates are low, and said that the fast food chain will focus on improving user experience, increasing the technology’s reliability and better training employees before making major attempts to market the service. About the Tracker.

No online database will replace the daily newspaper, no CD-ROM can take the place of a competent teacher and no computer network will change the way government works.”. Up until then, Stoll had made a reputation for himself in the online world for having snuffed out Markus Hess , the guy who’d successfully hacked into a bunch of U.S.,

QSRs have always marketed their fast service, but eCommerce has trained consumers to expect service that’s even faster, effortless and, most importantly, digital. Creating a mobile experience. As more customers start to organize their daily lives online and with their smartphones, QSRs must also make a move toward the internet.

As businesses and consumers become more comfortable using credit cards online, the proportion of US commerce that takes place online has steadily increased over the last 20 years. Specifically, the Collisons aimed to more seamlessly connect online businesses and payment processors, allowing more businesses to accept online payments.

In a world where transactions now take seconds rather than minutes, hours or days to process and approve, the prevention controls must be exercised in real time with intelligence applied across the medium of channels that might be used in today’s digital world, including cards and online banking transactions. million in 2007 to £52.5

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Ultimately, customers want to be known and valued.

Launched earlier this week (May 14), the Mastercard Innovation Engine is a plug-and-play platform that brings together Mastercard assets and FinTech services to provide enhanced customerexperiences. Indeed, that’s the name of the game for much of what’s driving innovation in the wider world of eCommerce and digital payments.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content