This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Artificial intelligence (AI) is poised to affect every aspect of the world economy and play a significant role in the global financial system, leading financial regulators around the world to take various steps to address the impact of AI on their areas of responsibility.

“That’s probably the worst experience in terms of false positives today: the customer experiencing that embarrassment. That insight provides the opportunity to start working with digital customers over a couple of statement cycles and trying out myriad treatments so they can provide the best possible customerexperience.

The reality is that banks don’t think from the customer’s perspective enough. The customerexperience is horrible for many bank processes. Bankers often think from the bank’s perspective or from the regulator’s perspective. What are the top three complaints from customers?

The reality is that banks don’t think from the customer’s perspective enough. The customerexperience is horrible for many bank processes. Bankers often think from the bank’s perspective or from the regulator’s perspective. What are the top three complaints from customers?

Finally, views are sought for compliance with applicable laws and regulations, including those related to consumer protection. Personalization of Customer Services. AI technologies, such as voice recognition and natural language processing (NLP), are being used to improve customerexperience and to gain operational efficiencies.

Our engagements range from implementing Drupal websites and portals to strategizing personalization and customer journeys, including clients in regulated industries like healthcare and financial services. We’ve enhanced upon the Acquia Drupal Cloud to provide ideal experiences in healthcare that meet HIPAA requirements.”.

Digital transformation will remain a powerful force, with advancements in AI and machine learning enabling unparalleled operational efficiencies and hyper-personalized customerexperiences. By ensuring compliance with regulations, banks mitigate risks and maintain trust with customers and regulatory authorities.

Generative AI ingests data and understands guidelines incredibly well; therefore, businesses across industries are jumping to take advantage of all the possible ways the tool can help save them money and create elevated, uber-personalized customerexperiences.

This means banks must make security an engaging part of their customerexperiences rather than a clunky friction point, and many are doing so by turning to AI and biometric authentication tools. While passwords are often arbitrary and static, biometric authentication methods are based on customers’ personal data.

In less than 60 days, the CFPB Regulation F requirements take effect. In simple terms, it means collectors can: Make seven call attempts within a seven-day period. Make one call within a week of speaking with the “right party.”.

EST, Bank Innovation will host a Zoom meeting for subscribers titled “Regulators’ and Financial Institutions’ Pandemic Responses: What Do We Know, What Can We Know, and When Can We Know It?” On Tuesday at 12 p.m.

In the new world of digital payments, many technology developments are driven by customerexperiences. Banks are investing heavily in technological innovations and Fintech relationships to provide better payments experiences to their customers. Read the full report.

In the new world of digital payments, many technology developments are driven by customerexperiences. Banks are investing heavily in technological innovations and Fintech relationships to provide better payments experiences to their customers. Read the full report.

A convergence of new customer behaviors, technologies, competitors and regulations will require issuers, acquirers and processors to review their overall card strategy to align the customer. Every executive can see the extent to which digital is changing the card business. Read more.

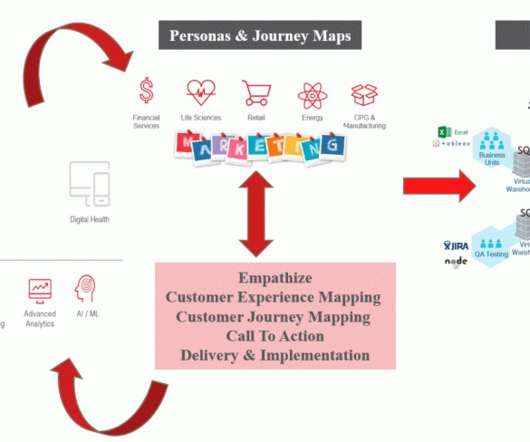

It affects decision making on everyday basis which does not let these enterprises provide value to their customers in an efficient manner. We at Perficient leverage CustomerExperience Mapping the most. What is Phase 0 in terms of CustomerExperience Mapping for our customers?

The Bank CustomerExperience Summit held in Charlotte, North Carolina from Sept. 9 to 11 will look at this topic in depth during a panel entitled, "How to meet banking regulations while delivering impactful CX."

The industry faces numerous challenges, including protecting sensitive data, navigating evolving regulations, and outdated legacy systems. To harness AIs potential effectively, its essential to develop a strategy that considers payment regulations to ensure consumer protection , data privacy , and ethical use of AI.

With the start of the new year, banks and fintech companies that do business in California will need to grapple with the new California Consumer Privacy Act (CCPA), which goes into effect Wednesday.

Regulation has undoubtedly acted as a catalyst to major financial services trends in areas like small business (SMB) lending, faster payments and, most recently, open banking and collaboration with FinTechs. According to the results, banks argue that innovation, not just regulation, is behind the wheel of progress. Optimism Up.

This integration not only enhances customerexperience but also opens new revenue streams and market opportunities for financial institutions. Investing in advanced technologies will help identify potential risks and ensure compliance with evolving regulations.

So, how does an insurance provider respond to this trend and the increasing number of regulations around data privacy (think GDPR or CCPA)? Customers have demonstrated a willingness to share data in return for mutual benefit, but firms must manage data carefully to avoid turning this asset into a liability. by the middle of the 2020s.

While there are no specific technical requirements, the Department of Justice states, “…The absence of a specific regulation does not serve as a basis for noncompliance with a statute’s requirements”. In lieu of a specific regulation, adoption of the WCAG has become a best practice in ensuring accessible web sites.

The expanded format provides more opportunity to run astray of regulations. Customer Adoption: Convincing customers to switch from SMS to RCS can be challenging, as it requires changes in user behavior and preferences. Rich communication services will serve banks well by dramatically boosting engagement.

Lior Cohen, senior director of cloud security products and solutions at cybersecurity firm Fortinet , recently told PYMNTS why the digitization initiatives many payment service providers undergo in the name of better customerexperience can exacerbate security risks. Greater Security Without Compromising UX.

Fraud protection specialist Kount and Philadelphia-based payments platform FreedomPay are teaming up to offer “an integrated, complete solution to enable international expansion with fraud-free payments and frictionless customer” experiences. Before, they were limited to one or two areas. Today, they’re pretty much everywhere.”.

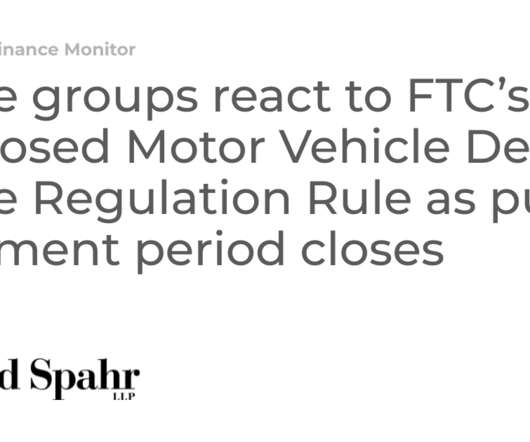

The public comment period for the notice of proposed rulemaking (“NPRM”) regarding the Motor Vehicle Dealers Trade Regulation Rule (the “Rule”) closed on September 15, 2022 after the FTC declined in August to extend it.

The pandemic shift to digital onboarding that increasingly uses intelligent automation will provide banks with cost savings of over $460 million over five years, and improve customerexperience.

This week, the Consumer Financial Protection Bureau filed suit against Citizens Bank, alleging violations of the Truth in Lending Act (TILA), including implementing Regulation Z and the Credit Card Accountability Responsibility and Disclosure Act.

In 2020, we saw lockdowns, tight regulations, and sadly, business closures. CIO Review states, “Digital transformation trends have been increased by 5.3 years, while experts predict global digital transformation investment will nearly double between now and 2023.”. A lot of progress has been made, especially on a global scale.

Open banking developments were impacting customers’ interactions with their banks before the COVID-19 pandemic. Financial institutions (FIs) and regulators in Singapore, the E.U. The EU’s PSD2 and GDPR regulations were passed in 2018 and designed with a primary focus on interoperability between open banking systems around the world.

While there are a few driving trends he predicts for the new year, they all have one thing in common, he said: customer service. “With the digitization of payments, small business customers of banks are demanding a strong customerexperience. Firstly, regulators driving Open Banking or Open Data (e.g.

We also enable clients to use Writer’s snippets to follow strict compliance regulations and efficiently include disclosures in their Sales and Marketing. Enhance customer trust and minimize potential risks by establishing a centralized and reliable platform for regulatory disclosures, ensuring transparency.

Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA). customers expect from their everyday primary bank account.” . customers expect from their everyday primary bank account.” . British challenger bank Revolut has submitted a banking license application to the U.K. 11) that having a U.K.

Since January, the European Central Bank (ECB), which oversees the biggest European Union lenders, has eased regulations to encourage mergers and reduced the capital requirements for such transactions, the news service reported. Regulators say consolidation in the banking sector would lower costs, improving efficiency and boost profits.

American Express is teaming up with Invoiced to help customers with an exclusive offer for 40 percent off an Invoiced subscription for the first two years. In a press release, American Express said it is committed to helping the digitization of B2B payments, still oft-regulated to paper and which end up being time-consuming and inefficient.

So, if an insurance company does not invest in the customerexperience of the claim, like during the claim flow, that is going to come back to them,” she said. That means firms must make sure that disbursements and all other customerexperiences can be accessed on multiple channels — including mobile.

As new regulations come into play, embedded lending is becoming increasingly prevalent, highlighting the need for banks to leverage data analytics and automation effectively while ensuring compliance with regulatory standards. Offering customized loyalty programs that stand out from competitors.

Without the ability to have face-to-face branch interactions due to the coronavirus, it became imperative for financial institutions to serve customers effectively through digital channels. See how digitization can improve customerexperiences. BSA Rules and Regulation. learn more. Lending & Credit Risk. SBA Lending.

Finastra unveiled Fusion Payments To Go , which the firm says decreases the expense and risk of keeping legacy infrastructure in adherence with regulations and evolving market initiatives. Fusion Reveals Payments Platform Banks. Europe and South Africa.

In this month’s Deep Dive, PYMNTS examines how data can improve customers’ experiences, and how regulations can keep their data safe. Regulators across markets realize the data risks that consumers face, and rules and regulations are in place to ensure that data is handled sensitively. More Data, More Innovation.

This mitigates the risk of customer service representatives providing incorrect information and ensures compliance with regulatory disclosures, ultimately enhancing the overall customerexperience while reducing costs.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content