This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Generative AI ingests data and understands guidelines incredibly well; therefore, businesses across industries are jumping to take advantage of all the possible ways the tool can help save them money and create elevated, uber-personalized customerexperiences.

It is imperative for community financial institutions to adopt innovative technology solutions that protect customer funds without impacting the customerexperience.” Enterprise riskmanagement is a complex process that pays for itself through cost reduction, brand and reputation enhancement, and bottom-line success.

Copilot isnt just another tech add-onits a game-changer that enhances efficiency, empowers staff, and elevates customerexperiences without disrupting our workflows. Faster Responses: In Teams, Copilot drafts replies to customer inquiries, ensuring quick, consistent service. Train staff via Teams and SharePoint.

Does the Bank Technology Improve the CustomerExperience Across the Bank’s Platform? To answer the question above, ask yourself – “How does the product scale across the bank’s platform to various customer segments?” The result is two different customerexperiences that cannot be brought together.

However, for more severe crises, such as a security breach compromising customer data, leadership often the CEO or CISO must take center stage to reassure stakeholders and outline corrective measures. Having a pre-determined spokesperson and media training in place can make a substantial difference in delivering a calm, credible response.

Takeaway 2 AI can lead to more accurate and consistent outputs or predictions, better riskmanagement, and improved customerexperiences. DOWNLOAD Takeaway 1 With generative AI technology improving by the day, the question is not if the banking industry will utilize it, but when.

Draw from your personal, industry, or business experience. What specific technologies would you like to see us pursue for a better customerexperience? This can also improve onboarding and training if your plan involves new staff or technology. Learn to identify emerging CRE credit risk red flags.

With stiff competition from alternative lenders, non-bank financial institutions, and money service businesses who are pushing the boundaries of the traditional lending model, financial institutions can’t afford to deny the efficiencies and convenient customerexperience of digitally enhanced loan systems. Lending & Credit Risk.

Takeaway 2 Use this time to optimize technology investments to increase profitability and improve customerexperiences. Takeaway 3 Pricing models for loans and deposits combat margin pressure and help retain your best customers. Examine user adoption and if necessary, arrange for additional training for staff. Learn More.

Both fintech firms and traditional enterprises are on the brink of significant disruption as companies leverage the rapid insights generated by AI in banking to drive demonstrable outcomes in customerexperience, riskmanagement and cost efficiency. The AI revolution has come to financial services.

That’s the topic of a recent whitepaper by ACI, which advocates that being “immediate” also means adopting a proactive, enterprise mindset towards fraud prevention and a willingness to invest across a number of fronts, from monitoring tools to staff training. This is even more critical in an instant/faster payments environment.

Until recently, the words “customerexperience” and “compliance” didn’t really come up in the same conversation – let alone exist in the same universe. There didn’t seem to be a need to connect this area, governed by rules and regulations, with the “front office” customerexperience. Learn more at ibm.com/RegTech.

Improving customerexperience and gaining efficiencies in the allocation of financial institution resources, such as through the use of voice recognition, natural language processing (NLP), and chatbots. Augmenting riskmanagement and control practices. Comments on the RFI must be received by June 1, 2021. Uses of AI.

It’s one of a banker’s worst nightmares: the digital banking conversion that was designed to improve the customerexperience fails – locking users out of their accounts, not showing balances, making wire transfer features inaccessible… It recently happened to a $25 billion bank in the Midwest. Communicate to users.

Other use cases abound, particularly in riskmanagement and sales. Use cases like service agents that can answer customer questions about treasury management 24/7/365 and quickly elevate to a human banker should it be asked or required. Agents can follow up with leads, qualify them, and hand them off to bankers.

Other use cases abound, particularly in riskmanagement and sales. Use cases like service agents that can answer customer questions about treasury management 24/7/365 and quickly elevate to a human banker should it be asked or required. Agents can follow up with leads, qualify them, and hand them off to bankers.

CustomerExperience – With customers jumpy and nervous, banks cannot afford to allow service lapses or information mistakes that could set off another wave of panic. Reaching out to large depositors with white glove service should also be included in the customer playbook.

So far, bankers have taken comfort in the soundbite that “this crisis is different” because of the strong capital levels and riskmanagement rigor that has developed since the Great Recession. The problem today is that most banks are not applying a true product management discipline to the debit and credit business.

It will interface with technology offerings from TCS’ partners for CRM, sales, riskmanagement and other enterprise functions. Further, it can leverage TCS’ fintech partner ecosystem to accelerate innovation and create superior and contextual experiences for its customers. “We

It is an active risk program integrated across the bank where owners take charge of their assigned riskmanagement activities. #5: A robust vendor performance management system also leverages proprietary benchmark data to ensure negotiated costs are competitive and aligned with the bank’s future growth plans.

CIP/BSA/AML/SAR /CTR Systemic tracking of activities across channels and branches, auto-filled forms, integrated risk ranking and easily accessible reporting. Training Requirements Calendar of training across the organization supported by virtual delivery and electronically captured confirmation. BBQ/JK/LOL/IDK/???

A part of the Tata group, India’s largest industrial conglomerate, TCS has over 385,000 of the world’s best-trained consultants in 46 countries. Ashvini Saxena, Head – Americas for TCS BaNCS said, “The successful deployment of TCS BaNCS at Zions is testimony to the commitment from both Zions and TCS to make this happen.

Our next-gen governance, risk, and compliance portfolio includes significant enhancements to IBM’s award-winning OpenPages 8.0 with Watson, which transforms the way risk and compliance professionals work. By providing a holistic view of risk and regulatory responsibilities, OpenPages 8.0 Financial Risk . OpenPages 8.0

For example, staff can build a BI environment that collects data, measures and teaches the bank where customer pain points are. This gets Lending, Retail, HR, Marketing, Finance and RiskManagement all involved. Everyone brings their functional lens to the table, but with the same idea of making it easier for the customer.

Product teams, business models and customer development strategy were all challenged in the last year as adaptation became the name of the game. The most popular posts in our Customer Development category dealt with digital banking, optimizing credit line increases, loan pricing and machine learning for credit risk models.

While Nvidia GPUs were initially targeted at the gaming industry, they have showed promising results in artificial intelligence, and are now widely used in training deep neural networks. Innovation in microprocessors — particularly Nvidia’s graphic processing units (GPUs) — have played a large role. led to a new age for AI. NEWS AND MEDIA.

Don’t you remember when you were building your business case for implementing mobile deposit, and your Chief RiskManagement Officer almost fell off her chair with the sheer thought of the amount of fraud that was going to occur? For example, AI has made it possible for mobile check deposits. Efficiency Ratio. Net Income.

The major themes of fraud, artificial intelligence (AI), expansion of instant payments, open banking, and regulation were particularly relevant to your roles as executives, riskmanagers, compliance officers, and technology leaders. How Banks Can Better Work with Law Enforcement Less than 0.5%

While a product like a certificate of deposit might only have a part-time product manager, a product like treasury management will likely have many. In addition to assembling the team, the product manager needs to take responsibility for the continued training around the problems, the environment, and related solutions.

At Cornerstone, our six components of a Smarter Bank are as follows : Strategy – focus strategy on crucial bets tied to a distinct business model Data – leverage data for breakthrough performance Experience – engineer customerexperience to drive revenue growth Technology – make tech a top-down discipline from the C-suites Ecosystem – actively manage (..)

Its Baldrige-winning tenacity on customerexperience is legendary and consistent. If you think of teams that take early system adoption risk, manage it well and get an edge on the competition as a result, you probably don’t think first of a $1 billion credit union in Kalamazoo. The bank’s strategy is laser-focused.

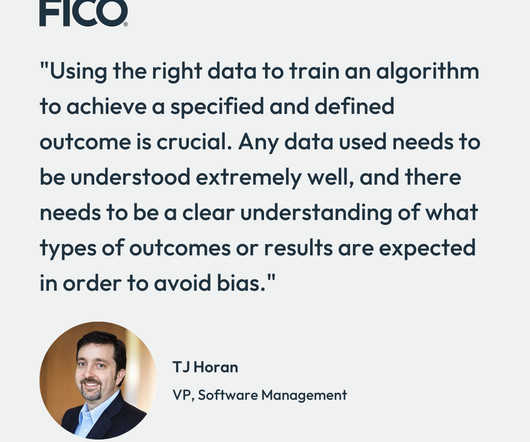

Unexplainable AI When we hear stories about generative AI systems that declare love or a desire to die, we’re often quick to equate it with a sentient being crying for help , rather than a mathematical model or algorithm regurgitating information from the data used to train it.

Thankfully for bank and credit union executives, lenders, riskmanagers, and Bank Secrecy Act (BSA) Officers, banking podcasts and podcasts for credit unions are plentiful, and options are growing. Lending & Credit Risk. Portfolio Risk & CECL. BSA Training. Asset/Liability. CECL Models. Stress Testing.

Many enterprises have succumbed to the inclination to digitize everything, which by default leads to cold, clinical experiences. It’s difficult, but embracing new technology means that we have the opportunity – nay, the imperative – to focus on humanizing the customerexperience. Omnichannel is customer-led.

Whether its retail, commercial, mortgage or wealth management, CIOs must understand major products and processes and how their bank seeks to differentiate itself competitively. Enterprise Resource Manager.

Seeing generative AI use cases can help bankers, riskmanagers, and financial crime professionals better understand it. They can more easily consider how to harness genAI's power to enhance their operations, compliance, riskmanagement, and member or customerexperience.

“There’s been times that I thought I couldn’t last for long. But now, I think I’m able to carry on.” ” Sam Cooke Gonzo Nation, 2024 went by so fast that nobody had a chance to stop and think about what in the world was going on. Let us pause and reflect. In retrospect, this was a funny year.

Along with giving consumers the ability to purchase tickets online, the train service also made the shift to accepting digital tickets. Of course, adopting new technology also means taking on a whole new set of risks. And almost overnight, we grew from primarily point of sale to an eCommerce [business],” Ziolkowski explained.

According to a recent survey by Gartner, Revenue growth, margin improvement and better riskmanagement are the top three functional objectives, in order, for next year. Whereas last year, banks focused on receiving payments, 2025 will focus on sending payments and allowing customers to request a payment.

Banks with enough scale want the ability to customize mobile apps and meld them into their work flows and customerexperience. Big c aveat emptor: developing custom apps means having the architecture, development talent and lifecycle discipline to stay out of trouble. V: “On the training extranet.”.

Banks with enough scale want the ability to customize mobile apps and meld them into their work flows and customerexperience. Big c aveat emptor: developing custom apps means having the architecture, development talent and lifecycle discipline to stay out of trouble. V: “On the training extranet.”.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content