This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

One of these aspects that almost always comes into play is userexperience, and for good reason. It’s been shown that customers will pay more for a quality experience , and this mindset also applies to ecommerce and the userexperience you are presenting to your customer base. Data Analytics.

A functional, seamless userexperience is critical for businesses operating in digital spaces. In this case, the site operator may choose a proactive metric measurement approach, such as prompting users to complete a short survey. A site that’s aligned to both your business and user needs is important.

Whether you’re checking your bank balance, getting an oil change, or enjoying another curbside pickup for Taco Tuesday, everyone loves a great customerexperience. And if you’re on the other side of that exchange, everyone wants to make their customers happy and coming back for more.

Marketing and Promotions : Banks can create visually appealing and engaging promotional content, including videos and images, to capture customer attention and drive engagement. This can lead to inconsistent userexperiences and limit its reach. RCSs power in the ability to deliver 1:1 marketing and customer support.

Businesses that combine advanced technologies with low-tech weapons like strong customer relationships will better position themselves to not just survive, but thrive in this increasingly competitive market. Preventing Hiccups in the UserExperience. Placing Big Bets on Customer Knowledge . billion in 2019 to $4.1

In fact, in a survey conducted by MagnifyMoney , 42% of respondents (notably, 48% of women and 35% of men surveyed) indicated they believe financial advisors are “only for wealthy people,” and 25% of respondents indicated they don’t see the need for a financial advisor for those younger than middle-aged.

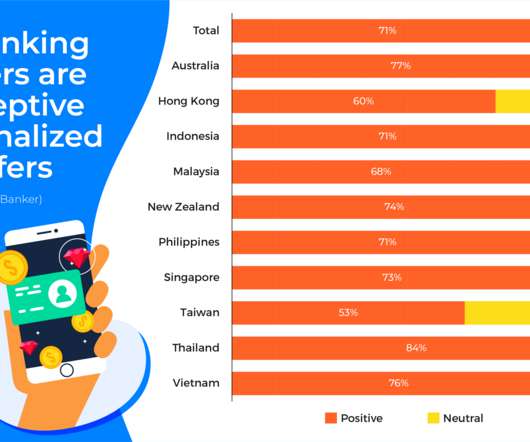

While mobile has long been a part of the carrier offering – pay a bill, get an ID card, file a claim – this survey reflects the evolution of insurers from transactional into personalized servicing. 1) Know Me – Data & Analytics Relevant to the Customer. 3) Tell Me – Authentic, Relevant Brand Messages and Experiences.

IN THE SAME WAY THAT AMAZON IS RELIGIOUS ABOUT THEIR CUSTOMEREXPERIENCE. TENCENT IS RELIGIOUS ABOUT THEIR USEREXPERIENCE. WECHAT USER NUMBERS & ENGAGMENT MOST INTERESTING STATISTIC FROM WECHAT’S LAST DATA REPORT WAS… “ONLY 1% OF WECHAT USERS ARE ABOVE THE AGE OF 55.”

With the landscape shifting rapidly for the financial services industry – thanks to the rise of digital and changing consumer expectations – being able to provide a strong customerexperience (CX) can be a key differentiator that helps banks stand out in a crowded and increasingly competitive market.

What does offering top-notch customerexperience mean in the digital age? As recent research from PYMNTS reveals, the most innovative FIs know that providing exceptional service to their consumer base comes down to focusing on three key components: userexperience, digital technology and data analytics.

But when it comes to the digital customerexperience, retailers are playing catch-up. But a new survey shows a new urgency. Eighty percent said providing a positive digital customerexperience (CX) was a “challenge” as a result of the pandemic. The customerexperience online has dozens of critical elements.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Ultimately, customers want to be known and valued.

In fact, a recent GeoGuard survey found that U.S. We’ve seen that people will share important information if they know that it will be used responsibly and to their benefit,” he said, “so when customers recognize the benefits of sharing location, they do.”.

More than ever – millennials seek customizedexperiences without a corresponding increase in prices. Cognitive systems are pivotally helping banks enhance customerexperiences, uncover new insights, and improve speed and quality of decisions. Interact using natural language, context and reason.

Luxury goods shoppers are notoriously finicky when it comes to customerexperience, and many luxury labels have a less than stellar track record when it comes to online userexperience, with fashion brands frequently sacrificing user-friendliness or functionality for style.

Josh Glover, EVP of the Americas at banking technology provider nCino, said that when it comes to corporate banking and lending, the end-userexperience is just as much of a focus for traditional banks engaging in digital transformation as it is in the consumer banking market.

They see that allowing members or customers to quickly open and fund accounts online: Creates a bridge to new commercial and consumer relationships and Offers a moat around existing relationships to protect them from competition Online account opening more than doubled at most banks between 2019 and 2020, according to the ABA Banking Journal.

According to the GTNews 2016 Transaction Banking Survey Report, 91% of North American corporates are evaluating their cash management partners. Clearly, these responses are evidence that large numbers of corporate clients are less than satisfied with the channel tools and the overall digital client experience being offered.

You might also like this resource, Abrigo's "2022 Loan Review Benchmark Survey Results." As 2023 winds down, community banks and credit unions have worked hard to attract new customers and members and retain existing ones by streamlining processes and improving the end-userexperience.

In retail banking, it’s clear customerexperience matters, and the stakes have never been higher. Study after study confirms the importance of providing personalized, integrated experiences for satisfaction and retention of financial services customers. Ultimately, customers want to be known and valued.

NUMBER26 , a digital banking startup based in Germany, did just that, taking cues from companies that have found success online and in the app store to build a simple and enjoyable userexperience. As a result, Stalf said he believes that his offering has a leg up when it comes to customer satisfaction.

FUEL CYCLE equips businesses to engage with customers through gamification and gamified rewards, surveys, group discussions, live chats, etc. The data collected through these online communities gives brands the insights they need to make real-time decisions that serve the commerce king: the customer. PYMNTS: What’s next?

Financial institutions are implementing technology throughout the customerexperience, including account opening, servicing and even transactions, but banks also need to know if clients are having problems navigating digital offerings.

As technology and userexperiences have evolved and competition has increased over the last decade, clients now have much more control, significantly influencing how product and offering teams go to market. In wealth management, this could mean creating advisory panels, pilot programs and surveys to elicit feedback.

It is well known that silos have long prevented banks from achieving the ideal customerexperience, because they create a fragmented userexperience. Banks are already their customers’ channel of choice in many ways, but they need to evolve to better meet consumer preferences as these mini-silos suggest.

Not only will it help improve the customerexperience, but it also promises to provide greater visibility whenever a consumer goes to make a purchase. More customers. Offering instant issuance can help attract customers – especially if other banks in the area aren’t doing the same. Greater purchase volume.

With face to face interactions limited due to the impact of Covid-19 the financial services sector can now look to grow their businesses using their websites and apps – but what will their customers think? FICO carried out a survey earlier this year with 500 Malaysian adults to find out. eKYC Malaysia – digital transformation success.

With a recent Billtrust survey finding that approximately 50 percent of businesses have not implemented a solution for sending electronic invoices, the time for a digital change is here. The CustomerExperience. According to Billtrust’s survey data, nearly 49.5 percent noting it is very important.

Biometrics technology creates a better userexperience because authentication is faster and easier than remembering countless user names and passwords or going through the motions of answering KBA questions. The good news is that consumers are warming to the idea in other areas of their lives (i.e.

Many businesses don't properly detail the ‘unhappy’ path sufficiently, assuming (or rather hoping) most customers will follow the 'happy' path. A poor customerexperience can negatively impact customer retention and seem them switch to a competitor that offers a more sophisticated, streamlined approach.

Organizations are looking for the next innovation that will transform the way they interact with customers. In the financial services industry, remote deposit capture first entered the market in the early 2000s, and now according to a recent survey by the American Bankers Association, one in seven Americans use mobile check deposit.

Technology has the power to significantly improve compliance efficiency, reduce costs, add brand value, and increase the customerexperience. In a recent survey of 100 banks across 10 countries conducted by Ovum, the majority of banks across all regions surveyed said they plan to converge their fraud and financial crime operations.

. “At BNP Paribas, we’re extremely interested in these new technologies; they are an integral part of our innovation policy, and we firmly intend to draw on them in order to create groundbreaking services designed to further streamline the customer journey and improve the overall customerexperience,” he added.

In the same vein, Centralized Decisioning delivers omnidirectional real-time insights and suggested actions in response to (or anticipation of) changes in a customer’s situation or macro-market developments. To your customer, it offers and immersive, high-personalized, and contextually responsive userexperience.

Why it’s a must-see: For banks: FIs can get an open platform that is truly able to deliver a superior customerexperience, while at the same time offering full control to manage and maintain; they’re not locked into any vendor. Lleida.net’s Connectaclick is a customized solution for electronic contracting.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content