This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Consumers’ banking habits have changed radically since the pandemic was first declared in March. Not only are many account holders visiting brick-and-mortar branches less often than they did before the pandemic, but many are also more reliant on digitalbanking channels — particularly mobile banking apps — than they have ever been.

Digitalbanking solution provider Alkami has announced it will acquire account opening solution provider MANTL for $400 million. Ron Shevlin’s Whats Going On in Banking research shows deposit gathering is still the #1 challenge for banks while new member growth (requiring deposit accounts) is the #1 challenge for credit unions.

I’ve talked about open sourcing banking and finance by converting everything to components (APIs) that can be plug and played into any front-end user experience (UX) through apps and devices, supported by data analytics, cloud and blockchain to reduce and automate the back office.

The Landscape According to Forbes Advisor: 2022 DigitalBanking Survey , as of 2022, 78% of adults in the U.S. prefer to bank via a mobile app or website. That’s a whole lot of consumers, all of whom come with unique expectations, needs, and data.

Fiserv acquiring First Data Corporation is a huge deal in the fintech world. Twenty-two billion dollars is a monster-size deal, but at 2X First Data’s annual revenue, the price is a way lower revenue multiple than the growth-oriented digital mashups lining up in the market. Maybe some of those First Data experiences will help.

Banks and credit unions are certainly not on their way out, even as they face more pressure from challenger banks, FinTechs and Big Tech in the coming decade. Google’s expertise is in UX design,” he noted. “By Banks are never going to become obsolete,” VB said, “but they could end up becoming stored value accounts.

Last year we published a highly successful The 11 Commandments of DigitalBanking eBook that introduced the 11 commandments: Digital lift-and-shift is not a strategy! Respect the data. Digital Lift-and-Shift Is Not a DigitalBanking Strategy. Friction – not inherently good or evil.

But what we see in our data over and over is that it is the experience of when, where and how it is [that] products are presented to the consumer that they actually become a lot more successful. Narayan said that partly means using some of the best user experience (UX) innovation that tech players have brought to the space.

Following the highly successful The 11 Commandments of DigitalBanking eBook , we are kicking off a series of 5 deeper dive blog posts that group the 11 Commandments below into common themes. Digital lift-and-shift is not a strategy! Respect the data. Respect the Data. Customer-level data (i.e.,

There are many lenses through which to consider promoting accessibility, such as location and physical accessibility, financial accessibility, data accessibility, and language accessibility. It is an entirely online bank but has customer service representatives who members can call and email when they need or want to talk to a human.

FinTech firms like Bottomline have invested in user experience (UX), user interface (UI), usability and, of course, data management. Intelligent systems can learn about users, and can then integrate more sources of data and translate that data into actionable insights. “We And the corporates themselves?

In a digital world, UX is key to winning loyalty. Banks and credit unions need to avoid pitfalls and create captivating experiences. The post 3 Ways to Create DigitalBanking User Experiences that Build Loyalty appeared first on The Financial Brand.

The Payments GonzoBankers have just returned from the PSCU member forum and the biggest announcement (among many) was the launch of Lumin Digital , a new digitalbanking platform that is currently available only to credit unions. PSCU is touting the solution as truly member first, not digital first. Member Impact.

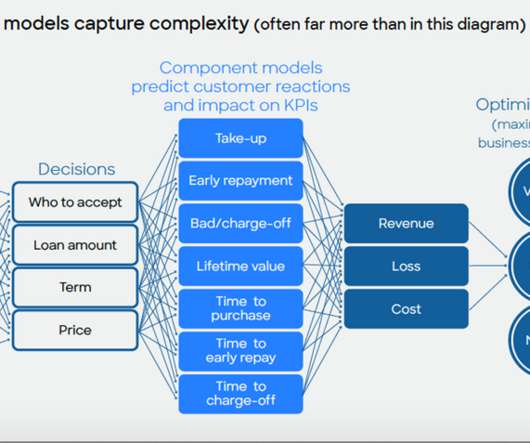

Home Blog FICO Top 5 Customer Development Posts of 2022: DigitalBanking and Pricing Opti The most popular posts in our Customer Development category dealt with digitalbanking, optimizing credit line increases, loan pricing and machine learning for credit risk models. Use location data to say “Good Morning!”

In this emerging landscape, financial institutions, often community banks, frequently “rent” their charter to financial technology firms (fintechs) that serve a specific consumer group as a means to grow non-interest income. More importantly, BaaS banks will need an I.T. This cannot be the extra credit work of a traditional bank I.T.

Traditional financial institutions have long known that trust is an asset, whether it’s trust to keep money safe or trust to keep data secure. ” The question is: do challenger banks need traditional institutions? Challenger institutions have been an important part of the banking ecosystem.

One of the biggest trends in fintech today is the rise of digitalbanking products like mobile checking accounts and new debit cards. From Square to Paypal, a host of fintechs are creating products that let consumers spend money directly out of digital accounts using a physical card. ux to help target existing clients.

Use of Red Hat Linux as a platform for Oracle RDMS and DNA has, for the most part, replaced the use of UNIX (HP-UX, etc.) From an operational perspective, running Oracle and DNA from the cloud is very similar (identical, really) to running it from a remote or co-located data center. Red Hat knowledge is common among Linux-savvy users.

One of the paradoxes of the early digitalbanking era (1995 to 2007) was why Capital One was a laggard? The new company (spun out from Signet Bank in 1994) was widely revered as a data analytics and marketing master. As recently as 2010 they were the last major bank to launch a native mobile banking app.

get the building the bank of the future report. Download the free report to find out about the rise of digitalbanking, challenger bank strategies and how incumbents are fighting back. Product engagement and maintaining a clean UX/UI. As a result, consumer adoption is at an all-time high.

That’s the driving factor behind Innofis , a company that furnishes a suite of digitalbanking tools providing a beautiful user experience for both bankers and their customers. In 2012, the company saw an opportunity in offering digitalbanking services. >3 million digital end customers (retail & corporate).

As of this publication, LinkedIn showed active listings for a UX design alchemist at Critical TechWorks and a product and solutions development alchemist at Together Abroad. The Tumblr team uses the data collected by Brennan’s team to better understand the unique communities, languages, and relationships that emerge on the platform.

STRANDS develops innovative software solutions that enable banks to offer personalized digitalbanking experiences by applying machine learning algorithms within big data ecosystems. Features: Intuitively transforms complex bankdata into key customer insights. Presenters. Marc Torrens, CIO.

Small business owners often have a love/hate relationship with their banks and financial providers. When I looked for data to support that claim, I was surprised to see the JD Powers research that concluded small businesses were pretty happy with their banks last year. Online DigitalBanks for Small Businesses (SMB) July 2022.

That’s a tradeoff HMBradley will likely accept since the bank will still have data on the customers paycheck along with customer’s attention every few weeks. Bottom line : Overall, I really like how HMBradley’s approach aligns the interest of the bank with its customers. DigitalBanks for Small Businesses.

Chuck Purvis, Coastal Community – Purvis waved the flag of innovation in the credit union industry, helping Coastal become famous for its usage of interactive teller machines (ITMs) and launching the Constellation DigitalBanking platform. The Smarter BankData Award. The Calm Before the Storm Award. Goes to CSI.

Mike Lawson chats to Rhonda Sheets from Support EXP about credit unions and the all-important customer journey. 5 critical challenges facing credit unions around the ‘customer journey’ on BankNXT.

Legacy banks need not apply. Sure, we know it’s cliche to point out the merits of this direct banking powerhouse, but the plain fact is that USAA nails every variable in building a Smarter Bank. The bank’s strategy is laser-focused. It was the original data junkie. It is an innovator with tech (e.g.,

And CNBC notes that, conversely, the KBW Bank Index is down by roughly a third. For a model significantly predicated on transaction fees and debit spending, there are signs that consumer spending may be hampered by a falloff in stimulus checks , and as worries over the economy persist (August’s data was muted).

And CNBC notes that, conversely, the KBW Bank Index is down by roughly a third. For a model significantly predicated on transaction fees and debit spending, there are signs that consumer spending may be hampered by a falloff in stimulus checks , and as worries over the economy persist (August’s data was muted).

New Data: FIs’ Most Underutilized Asset: Their Apps. In the Consumer-Centric Authentication Playbook: The Path To Banking App Adoption Edition, PYMNTS asked 2,835 consumers to better understand how FIs can enhance their apps’ UX to boost engagement. Business Models Drive Integrated Payments Innovation.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content