This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

How to prevent internal fraud at your bank or credit union Of the many fraud risks banks and credit unions face, one of the most costly comes from within the institution itself. ACFE reported that 5% of an organizations revenue is lost to internal fraud each year, with an estimated $3.1 billion in total losses.

Transaction monitoring ensures more than just compliance Without reliable client and transactional data coming into your monitoring system, either manually or automatically, you could miss crucial suspicious activity. Staying on top of fraud is a full-time job. This could put your institution at regulatory and reputational risk.

Can your AML/CFT and fraud staff recognize these fraud typologies? The technology used to perpetrate financial crimes may be changing, but these common fraud typologies aren't going anywhere. This is a nearly 10% increase in complaints received and a 22% increase in losses and thats just fraud that was offically reported.

Evaluating the FRAML approach For years, financial institutions have debated the merits of combining fraud and anti-money laundering (AML) functions into a single department in what's known as a FRAML approach. With such heightened scrutiny on fraud, keeping AML and fraud teams siloed may not be sustainable.

Artificial intelligence (AI) is transforming fraud prevention AI offers financial institutions a way to reduce false positives, detect fraud faster, and improve suspicious activity monitoring. Staying on top of fraud is a full-time job. Let our Advisory Services team help when you need it.

Data fuels the engine of the digital economy. Connected experiences, in the context of the customer relationship, are driven by a robust data set that confidently presents integrated, diverse data to enable actionable insights that can be automated across the customer’s journey. by the middle of the 2020s.

We are witnessing the integration of AI, the rise of hyper-personalization, and the adoption of advanced digital platforms, all of which are revolutionizing operations and client interactions. Advancements in data analytics, AI, and machine learning, enable financial institutions to offer highly personalized services.

A couple of weeks ago, we delved into the origination and operating costs of manufacturing commercial loans ( HERE ). We will use their data and methods for this analysis. In addition, this cost segment includes the cost of pursuing fraud and negative balance management. From the above data, several conclusions can be drawn.

Digital transformation will remain a powerful force, with advancements in AI and machine learning enabling unparalleled operational efficiencies and hyper-personalized customer experiences. In 2025, banks will face a more complex regulatory environment, with new rules focused on data privacy, cybersecurity, and sustainability.

This brings a longstanding challenge to the fore: Healthcare organizations have long struggled with fraud, waste and abuse (FWA), costing the United States healthcare sector more than $200 billion annually by some estimates. Moreover, the benefit cited by the greatest proportion of healthcare firms (65.6

Payment system types, trends, and fraud risks Understanding how payment systems function, the different types in use, and the associated risks is critical for financial institutions to be able to balance innovation with security. Need short-term fraud or AML staffing relief? trillion in 2021, according to the latest data from the Fed.

Those new avenues of fraud have leveraged hallmarks of the current pandemic — fears over public health and concerns about stimulus checks issued by the government — to snare unwitting victims. . . According to some estimates, as many as 22 percent of Americans have been impacted by COVID-related fraud. . .

A massive spike in fraud of all kinds has taken businesses by surprise and left them scrambling for solutions, Trulioo Chief Operating Officer Zac Cohen told Karen Webster in a recent conversation. Unfortunately, those firms are finding that they’re surrounded by fraud sharks eager to take a bite out of their business.

Harnessing consumers’ digital information is critical to the success of any business, and data analytics and artificial intelligence (AI) can be especially powerful tools. Fast-food giant McDonald’s was not interested in using AI or data analytics until it noticed that many of its competitors were benefiting from the technologies.

The economic risks of AI to the financial systems include everything from the potential for consumer and institutional fraud to algorithmic discrimination and AI-enabled cybersecurity risks. By continuously improving and adapting over time, AI-driven credit scoring ensures a fairer assessment and broader availability of credit.

Mobile ordering apps are largely responsible for keeping the industry above water, but fraud still plagues the sector. And while promising news regarding COVID-19 vaccines may have put the end of the pandemic in sight, the restaurant industry’s growing fraud concerns will not cease as abruptly.

The industry faces numerous challenges, including protecting sensitive data, navigating evolving regulations, and outdated legacy systems. To harness AIs potential effectively, its essential to develop a strategy that considers payment regulations to ensure consumer protection , data privacy , and ethical use of AI.

The economic risks of AI to the financial systems include everything from the potential for consumer and institutional fraud to algorithmic discrimination and AI-enabled cybersecurity risks. Fraud screening.

With digital transactions and eCommerce soaring during the pandemic, the rate of increasingly sophisticated fraud has also risen. Accurate and reliable data is a critical piece of modernizing the AML regimen,” he said. consumers were increasingly likely to share their location with banks in order to protect them from fraud.

Compliance with investment accounting and reporting requirements plays a central role in ensuring operational efficiency and regulatory adherence. Investment accounting compliance not only minimizes operational risks but also reduces regulatory scrutiny. WATCH Investment accounting compliance risks U.S.

Merchants are adapting quickly to a rapidly digitizing environment, caught between trying to build a smooth, seamless experience for their good customers and trying to prevent fraud of all sorts as attacks increase in both number and activity level. There’s no single lock-off point to which all fraud can be defended against.

Increasing efficiency of compliant AML investigations To boost AML program productivity and keep pace with evolving compliance demands, financial institutions should focus on strategic operational improvements paired with the smart use of technology. Enhance staffing strategies with data-driven assessments. What’s a leader to do?

Microsoft’s Azure Integration Services , a suite of tools designed to seamlessly connect applications, data, and processes, is emerging as a game-changer for the financial services industry. This connectivity enhances interoperability, allowing for streamlined operations and improved data flow across various platforms.

To support debit card operations, a bank gets charged a myriad of transaction charges and maintenance fees from the card rails (Visa, Mastercard, Discover, etc.), Materials, training, and fraud also contribute to bank expenses. the network (Interlink, Pulse, Shazam, etc.) and the bank’s processor (usually their core).

The applications of artificial intelligence (AI) are manifold, and many feel that perhaps its most meaningful uses are in the healthcare field, where data can be a matter of life and death. Better fraud detection also reduces false positives, erroneous judgments that block legitimate transactions. Fraud, Waste and Abuse (FWA).

Mari Anne Bayliss , senior director of solution management at CyberSource , told Karen Webster that simply relying on machine learning as a weapon against fraud is not enough — not in an age where managing fraud risk during the great digital shift (and unprecedented transaction volumes) is so challenging. . Human Touch .

Kount , which works in digital fraud protection and identity trust, announced today (Dec. 1) that it is working with data cloud provider Snowflake to provide enhanced, artificial intelligence- (AI) driven insights into customer behavior, according to an emailed press release.

The prevalence of online commerce opens new doors for digital fraud, however, both from career fraudsters and opportunistic customers. Developments F rom The World Of Digital Fraud. Developments F rom The World Of Digital Fraud. For more on these and other digital fraud news items, download this month’s Tracker.

Telecommunications companies face a number of challenges in their day-to-day operations, however. Onboarding these customers can be a tedious challenge prone to fraud and consumer frustrations, and the industry faces the ever-looming threat of SIM swap fraud. SIM Swap Fraud Plagues Smartphone Users.

The growth in digital transactions is also spurring a boost in friendly fraud, which occurs when legitimate customers either knowingly or unwittingly claim that they did not make legitimate purchases and seek reimbursement for them. It also analyzes how focusing on the customer experience can help prevent such fraud in the first place.

of Americans are considered “fully banked,” many opportunities exist for financial services institutions to take advantage of the vast amount of customer data they possess. Here are three ways financial services institutions can reap the benefits of a data-driven mindset. market trend data, economic data, etc.)

Legal Obligations and Regulatory Frameworks It is well-known that financial institutions operate within a complex web of laws and regulations. Operational Efficiency and Effectiveness Adopting regulatory risk and compliance practices is not merely a box-ticking exercise. This ensures a seamless and compliant global operation.

Prevent fraud when adopting FedNow Credit unions can prevent fraud as they connect to FedNow. Use this guide to understand available tools and the steps AML and fraud teams should take. You might also like this FedNow implementation guide with details on appropriate AML/CFT and fraud considerations.

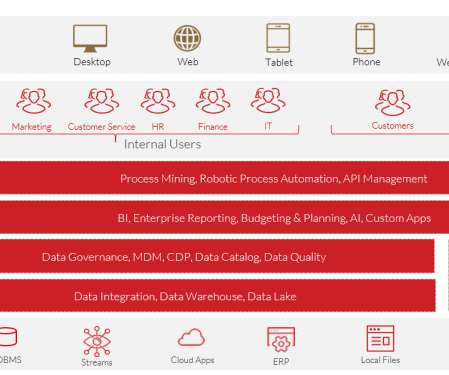

The world of modern data and analytics continues to evolve and is very exciting. The change really began in earnest about 10 years ago with the introduction of Hadoop and big data processing. While this explosion of data use cases started on premises, it is most certainly migrating to the Cloud as the primary platform.

When it comes to fraud threats, no company — large or small — is immune. In this week’s Data Digest, PYMNTS rounds up the latest cases and research into how corporates are being targeted with crimes like the business email compromise (BEC) scam, as well as how they’re fighting back.

This means that thanks to recent Apple upgrades in their operating system, most phones are now capable of receiving Rich Communication Services (RCS) messages in addition to traditional SMS. Popular use cases include request for payments using the instant payment rails (above), loan payments and transaction verification to prevent fraud.

As merchants accelerate their digitization roadmaps, the volume of data they’re able to work with increases. But data in payment transactions provides an often-untapped opportunity for merchants to optimize their payment operations and grow their businesses, Tony Wimmer , head of data analytics for J.P.

Open banking’s impact on small- to medium-sized businesses (SMBs) continues to proliferate as traditional financial institutions (FIs) embrace the opportunity to unlock data for third-party platforms. Unlocking data also means an easier bank-switching process for SMBs in search of improved borrowing processes. In the U.K.,

Mobile banking is under constant attack from fraudsters, however, who are targeting both customers’ funds and personal data, such as account numbers, Social Security numbers, payment card data and login credentials. ATMs are common avenues for fraud, however, especially those that are running outdated software. billion by 2024.

With this regulatory risk and associated operational complexities, there is plenty for financial institutions to consider before diving into cannabis lending. According to FinCEN suspicious activity report (SAR) data , over 800 financial institutions have decided yes, at least to banking deposit services for CRBs.

Adhering to Payments Card Industry (PCI) Data Security Standards (DSS) is an unavoidable requirement for any and all eTailers that accept card payments, but a surprising number of firms are not up to speed on these standards. Either way, firms that do not comply with these industry standards risk leaving their customers’ data exposed.

Court case: Credit union held liable for ACH fraud losses A construction company argued the financial institution "failed to establish a reasonable routine" for monitoring suspicious activity alerts tied to ACH. Takeaway 3 Remember that ACH fraud risk also occurs in the placement stage of a fraudulent or money laundering scheme.

He and Nitendra Rajput , Mastercard’s vice president of product development and head of the company’s “AI Garage,” said that in many cases, AI is the only way to scale up sufficiently to meet the challenges the company faces with fraud and other business issues. “It Fighting Fraud in a Post-Pandemic World.

The currency exchange company continues in the grips of a ransomware attack that has crippled its operations, as well as the foreign currency operations of its corporate clients, including HSBC and Barclays. The scam reportedly lasted about five years, and the former bookkeeper has now been charged with felony theft.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content