This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Here are my headlines: 76% of millennials are looking for new forms of banking 40% of people in their twenties have downloaded a money management app 80% of millennials … The post The future of money (research report) appeared first on Chris Skinner's blog.

In late June, the Monetary Authority of Singapore (MAS) sent a ripple through the global financial services ecosystem with the announcement of its intention to issue five digitalbank licenses to eligible applicants. Only two of the licenses will full digitalbanking licenses, while the other three will be wholesale banking licenses.

for assistance with its “Digital 2x” initiative. The program aims to accelerate the integration and deployment of digitalbanking technologies and to improve member experiences. Further collaborations could be possible if credit unions and community banks can work better together, according to J. The good news?

Banks today are familiar with the challenges of supporting digital platforms as an increasing number of customers turn to online-only solutions. One study found more than 45 percent of millennial users, for example, have at least considered leaving their FIs and signing up with fully digitalbanks.

When you talk to the co-founder and CEO of a mobile-first digitalbank account offering, you are likely to hear that millennials, to put it lightly, are not fond of big banks. And that’s where digitalbanking options like Chime (a mobile-first digitalbank account, for those of you playing at home) enter the picture.

Our findings also indicate FIs that offer innovative options such as interactive and contextually relevant video content stand to improve engagement and customer experiences, especially among younger generations like bridge millennials and millennials.

A lot of fuss is made over millennials and their proclivities toward things being easy. So, when it comes to something like digitalbanking , it’s not so much about finding what’s easy as it is about finding what service best meets millennials’ needs. Millennials to big banks: No thanks ….

As banking becomes more digital, more financial institutions are turning to technological solutions to bring more customers on board. Several banks are rolling out banking solutions that are specifically focused on winning over millennial customers as they come of age and join the marketplace as adults.

I am half Gen X and half Millennial in my habits. I am notorious for downloading the app for every restaurant, gas station, movie theatre, hotel, airline, etc. And yes, I have an app for each of my credit cards and my bank. I like to see how a company represents itself digitally. OK … let me begin by identifying myself.

percent of national banks, versus 77.5 percent of local and regional banks, according to respondents. Overall, national banks offer 6.9 separate app features on average, while digitalbanks offer seven and local and regional offer 6.6. Another popular feature — reporting cards lost or stolen — is offered by 86.2

But, while closing physical bank branches might appear to be a wise cost-saving measure, the move comes with risks that could hurt banks’ relations with new millennial customers. For Bank of the West, this has meant trying to get in front of expectations rather than perpetually attempting to catch up.

The alternate payment company said the offering is available through its app, which users can download from the Google Play Store or App Store. Affirm said that millennials and Generation Z comprise more than half of Affirm’s user base and are “especially suspicious of the fine print and hidden fees linked with traditional banking services.”

One way that banks or ambitious social media platforms will win this combat for customers is through the use of mobile credit and debit cards, with a highly configurable nature and full range of card and spend management controls to please the most vacillating of customers. What is changing are the card habits of demographic groups.

June’s PYMNTS DigitalBanking Tracker™ looks at the latest trends in the digitalbanking space, including efforts by banks and FinTechs to give consumers new insights into their finances and the latest developments on the path toward Open Banking. About The Tracker.

New digitalbanking solutions are creating new options for these citizens to make a difference in the world through their consumer purchases. The Right Tool for Millennial Shoppers? This is especially true of millennial consumers who are more likely to consider a store’s values when making a purchase than other generations.

The December edition of the DigitalBanking Tracker™ details how financial institutions are working to help their consumers stay in good fiscal shape next year. Meanwhile, FinGo and eWise are also offering a new app to help millennial customers manage multiple bank accounts from a single screen. About The Tracker .

From selfie authentication to finance tools that respond to emojis to computer-generated avatars that look and act like real people, new technological tools are giving digitalbanking a makeover. The April PYMNTS DigitalBanking Tracker™ looks at the various ways technology is changing the digitalbanking landscape.

Nearly 44 percent of respondents said they would be “very” or “extremely” interested in downloading it. The rate rises to 60 percent among bridge millennials, those between the ages of 30 and 40. . The results? Such an app could potentially involve as much as $2 trillion in card spending. .

This is especially true for Generation X and millennial consumers, at 37 percent and 36 percent, respectively. For more insights, download the report. We also found that there is good reason for card issuers to provide location sharing-based fraud protection. These are just a few of the findings illuminated by our research.

According to Chris Britt, CEO of mobile-first banking platform Chime, consumers are getting frustrated with larger, traditional financial institutions. And this frustration has created an opening for digitalbanking newcomers like Chime to swoop in and address these consumers’ concerns. The millennial advantage.

According to recently released research from the American Bankers Association, mobile banking is becoming increasingly popular among consumers of young ages. Members told us they had been using other voice technologies, like the Alexas or Siris of the world, and they wanted to use the voice command to do their banking,” Advani explained.

Consumers are downloadingbanking apps in record numbers, but they’re not always blown away by what they’re getting. percent) think bank apps should be easier to use. Six Sides of the Bank App Persona. Control vs. Chaos? That’s a painful disconnect for a connected economy (like the one we’re in now). Fair enough.

Fintech is often associated with digital tools targeted at tech-savvy millennials. Download the free report to find out how fintech is shaping the future of wealth management and investing. Download the free report for all the details. Estate planning gets a digital makeover . The outlook for Baby Boomer fintech.

Mobile banking apps are designed to make digitalbanking more convenient for customers, yet 21.7 To learn more about what consumers want from their banking apps, download the Playbook. percent of consumers who use these apps are dissatisfied with them.

In an effort to better serve millennial business owners, Sandia Laboratory Federal Credit Union partnered with Alkami Technology to offer more digitalbanking solutions, including bill pay, personal finance management tools and P2P services. Some of these partnerships were specifically aimed at helping SMBs. About the Tracker .

The bank opted to pilot the technology in its student app, he said, because millennials are known early adopters. To download the May edition of the DigitalBanking Tracker™, click the button below. The app that we launched it in is an app for students,” he said. “We You may want to try asking Siri.

According to the PYMNTS Bridging The Gap: Mobile Card App Adoption report indicates that nearly two-thirds of consumers use their digitalbanking app at least twice a week, over 90 percent of Gen Z consumers have downloaded mobile card management apps and 70 percent of consumers report the mobile app is their preferred tool for card management.

PYMNTS recently caught up with Matthew Lehman, KeyBank’s SVP, Head of Online and Mobile, to discuss the evolution of digitalbanking and how a full-service bank is embracing digital and evolving along with its customers. Digital adoption – no longer solely a millennial-focused play.

Bank of America, for one, saw profits drop 16% year-over-year (YoY) in Q3’20 to $4.9B. The pandemic has also accelerated recent trends in banking, especially among the millennial demographic, which tends to favor digitalbanking and online brands over traditional banks. First name. Company Name. First name.

Home Blog FICO Top 5 Customer Development Posts of 2022: DigitalBanking and Pricing Opti The most popular posts in our Customer Development category dealt with digitalbanking, optimizing credit line increases, loan pricing and machine learning for credit risk models. What can financial institutions learn from TikTok?

Top 5 Surprises from FICO’s Fraud and DigitalBanking Survey. Financial Institutions, such as banks, have expended great effort to improve digital security, yet bad actors are multiplying and attacks have increased in scope and frequency. Download the white paper on this survey. FICO Admin. by Sarah Rutherford.

By contrast, digitally savvy FIs that had already been boosting their mobile capabilities are seeing more than a 360 percent increase. OnDot has seen the open rate on FIs’ downloaded mobile apps more than double, from about 35 percent in the pre-COVID-19 era to 79.06 It’s not just about digital self-service.

Nine years after the introduction of the iPhone to the market — and the subsequent great mobile leap forward — the verdict is pretty much in on mobile banking applications: Consumers like it, verging on loving it, and are eager for more of it. Double-Edged DigitalBanking Sword. The other half offers something very out-of-date.

But how far are they willing to go to do their banking on small mobile devices? A consensus says that the future banking customer relationships—particularly for millennial consumers—will orbit to one degree or another around mobile technology. s entry into the payments business with Apple Pay. Ed Bachelder, payments consultant.

In terms of more targeted offerings, banks that are looking to reach the 35-and-older demographic, for example, are integrating a large amount of lending functionality, while those that want to service the millennial end of the consumer spectrum are doing so with offerings related to instant cash access and instant transfers.

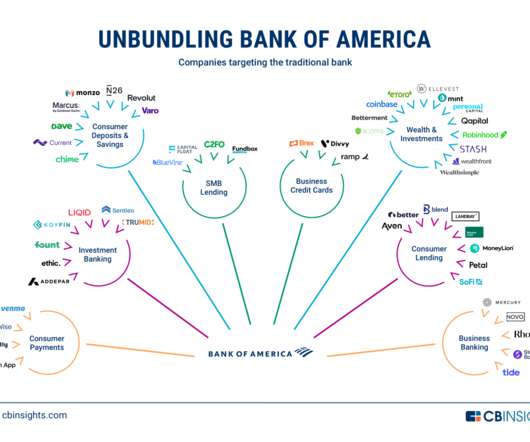

What these startups share is the goal of creating customer-centric banking products that target underserved individuals and businesses. DOWNLOAD THE 61-PAGE consumer banking REPORT. See which startups are helping JPMorgan, Bank of America, and Citi build the digitalbanking platforms of the future.

alone will be using mobile banking. Consumers are hungry for new ways to make their banking easier and more efficient. Proactive banks have an opportunity to transform consumer behavior, win millennial customers and satisfy existing customers by taking advantage of the unique differentiation opportunity of mobile.

get the building the bank of the future report. Download the free report to find out about the rise of digitalbanking, challenger bank strategies and how incumbents are fighting back. As a result, consumer adoption is at an all-time high. Business model transparency with competitive pricing and fees.

Available only via mobile app, imaginBank is a new initiative by Spanish bank, Caixabank targeting millennials. CaixaBank CEO Gonzalo Gortázar said the new mobile-only bank was part of a “commitment to providing new services that perfectly complement the more traditional banking model.” CaixaBank serves 2.9

Instead of physically going to a bank, 69 percent of mobile media customers are accessing banking accounts and transferring funds from the convenience and flexibility of their phones. The switch to digitalbanking has been a relatively recent change, and mobile banking has only just emerged as a viable option for customers.

Download the free report to find out how Asia’s internet giants are creating the playbook for fintech super apps. WeBank , a Tencent-backed digitalbank that is reportedly valued at $21B, is also expanding credit to China’s small businesses. learn about asia internet giants’ fintech playbooks.

Econiq’s Conversation Hub uses color-coded conversations to help bank and insurer frontline staff, operational management and executives avoid disconnected customer conversations in branches and contact centers. The platform uses instant video chat and guided browsing with no downloads or installations.

Backbase will talk about its DigitalBanking Platform and its Open Banking Marketplace. Fueled by a strong, open API strategy, Backbase’s platform gives FI’s the ultimate freedom and flexibility to work with any core and third party vendor, to create a best-of-breed digitalbanking offering for their clients.

I’ve heard that financial planners are having a hard time getting Millennials thinking about retirement but instead focus on short-term financial goals – homes, vacations, etc. Specializes in digitalbanking platform. Download: 10 Reasons Why Fintech Startups Fail White Paper. As always, how does this company make money?

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content