This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

FinTech LendingClub is purchasing Radius Bancorp for $185 million in cash and stock, according to a report by CNBC. The bank is one of a few smaller lenders that has teamed up with FinTechs who need services only an FDIC-regulated institution can provide. This is the first time a FinTech has purchased an actual bank.

On the heels of digitalbanking startup Varo Money applying for a banking license with the Federal Deposit Insurance Corporation (FDIC) earlier this month, another fintech firm with its toes in charter waters seems poised to jump in.

Where once the marquee names in tech (and no shortage of FinTechs) jockeyed for primary banking services relationships, an increasing number of partnerships are now taking shape. To that end, BBVA was one of six banks that said on Monday (Aug. To that end, BBVA was one of six banks that said on Monday (Aug.

Yet demand for contactless payments and digital, automated financial solutions means FinTech funding may not take as hard of a hit as other startup segments. however, funding for FinTechs actually increased to $3.7 B2B FinTech investments appear to be relatively strong, too. As an FDIC insured bank in the U.S.,

And according to five observers across the spectrum of traditional financial institutions (FIs), payment networks and digital-only banks, opportunities are there for digital-first and hybrid models alike to succeed — so long as they harbor a relentless focus on identifying and solving customer problems.

Community financial institution (FI) Cross River Bank is acquiring Seed , a small business (SMB) digitalbanking company, reports in Reuters said on Monday (June 24). Cross River Bank has partnered with a range of FinTech startups since its 2008 launch, including collaborations with Stripe , Coinbase and Affirm , reports said.

To move toward retirement, and to have the money in place to get there, millennials need to make the leap from bare bones banking — checking and savings — into investing. Asked about regulation, Ganu said that the firm works with an FDIC insured partner bank and a SIPC partner broker dealer, Apex Clearing Corp.,

The ongoing struggle, supposedly existential in nature, that pits upstart, relatively young FinTech firms against arrogantly complacent banks for supremacy in this new and growing world of digital payments and commerce. Trust in Banks. And that is a bank – one with FDIC insurance and safeguards that keep their money safe.

households unbanked or underbanked according to data from the FDIC, fintechs have long promised better financial access, whether through online lending that looks beyond traditional credit underwriting or digitalbanking startups with fewer fees. With more than one-quarter of U.S.

households unbanked or underbanked according to data from the FDIC, fintechs have long promised better financial access, whether through online lending that looks beyond traditional credit underwriting or digitalbanking startups with fewer fees. With more than one-quarter of U.S.

The FinTech partnered with Metropolitan Commercial Bank for FDIC backing of deposits up to $250,000. “As Revolut is one of the few FinTechs to break even so quickly, but it did see a 40 percent dip in revenues amid the initial coronavirus outbreak. In March, Revolut launched in the U.S. to meet demand, the company said.

Digitalbanking startups are popular in Europe, dangling low fees and mobile apps to attract more customers. Challenger banks have raised $100 million worldwide in the second quarter and are the fastest-growing FinTechs, Lindsay Davis, a senior intelligence analyst at CB Insights, told the FT. .

The Tracker also examines how mobile and instant disbursement tools could be essential to making sure these individuals are still able to participate and transact within the digitalbanking world. percent in 2019, its lowest rate in a decade since the FDIC first began tracking this statistic in 2009.

But as of 2020, it is a subject upon which seasoned experts can disagree, in a world where traditional banks and FinTechs are operating in parallel in the market – and, in many cases, are offering similar services for consumers. But the FinTechs, Baird noted, are adapting and innovating around that issue. Baird said. “As

In the continued linkups between banks and FinTech upstarts, new markets beckon across various borders. Among the latest examples, N26 , which is a digital-only bank based in Europe, has entered the US market through partnership with Axos Bank in order to offer FDIC insured accounts.

All the capital flowing into the digitalfintech space is helping to solve banking industry challenges. As the industry’s appetite for digital technology grows, the capital that’s been flowing into mostly digital-focused fintech is solving real industry challenges right now. SoFi/Galileo: This $1.2

Like other FinTechs, Betterment will partner with FDIC-insured institutions since it doesn’t have a bank charter. Although traditional financial institutions largely don’t consider FinTech firms as competition, both established and emerging FinTechs are well-positioned to capture traditional banking customers.

Robinhood , the FinTech that garnered a lot of attention last week after announcing a checking and savings product with 3 percent interest, has retreated from that, removing any mention of checking and savings from the product.

Without a regulatory mandate, many in the financial services and FinTech space believe that competition will — and already has — nudged the industry toward embracing data integrations across platforms and service providers in the name of better banking experiences. Bank participation is key to promoting open banking in the U.S.,

Payments processing and digitalbanking tech firm i2c has partnered with business payment services provider CashFlows to benefit payment card issuers across Europe, i2c announced on Tuesday (Jan. The partnership enabled Evolve to offer its FinTech clients a way to develop customized banking and payment products.

Payments processing and digitalbanking tech firm i2c has partnered with business payment services provider CashFlows to benefit payment card issuers across Europe, i2c announced on Wednesday (Jan. The partnership enabled Evolve to offer its FinTech clients a way to develop customized banking and payment products.

In the past few years, the burgeoning popularity of digitalbanks has only underscored the severity of these problems, with upstarts like Chime and SoFi offering cheaper, faster, and more convenient banking experiences. . get the state of challenger banks report. Source: FDIC. Source: PwC. The unbanked/underbanked.

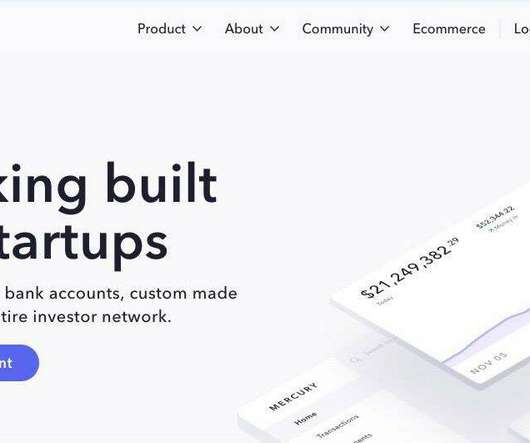

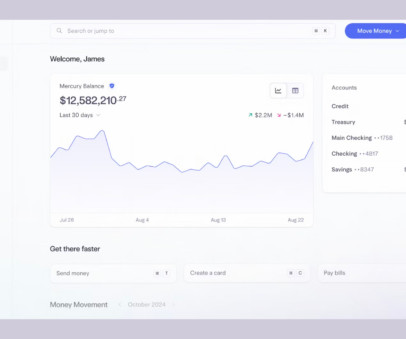

Mercury , a fintech company, has raised $120M in a Series B. California-based Mercury is an online banking platform that offers a suite of financial services such as FDIC-insured bank accounts, physical and virtual cards, and cash management for startups, e-commerce stores, and angel investors, among others.

The FinTech partnered with Metropolitan Commercial Bank for FDIC backing of deposits up to $250,000. “As Revolut is one of the few FinTechs to break even so quickly, but it did see a 40 percent dip in revenues amid the initial coronavirus outbreak. In March, Revolut launched in the U.S. to meet demand, the company said.

In today’s top news in digital-first banking, California FinTech Green Dot is rolling out the GO2bank mobile banking to help cash-strapped individuals, while stimulus checks are reportedly posing challenges for some users of H&R Block and TurboTax. Green Dot Introduces GO2bank To Help Cash-Strapped Consumers.

Chase, Wells Fargo, Bank of America and Citi, to name a few, all scaled back their physical bank branch locations between 2012 and 2016, according to the Federal Deposit Insurance Corporation (FDIC). Additionally, if recent trends are any indication, physical bank branches stand to lose a lot of ground in the near future.

FDIC) study found that the number of unbanked U.S. Banks and financial institutions (FIs) have been layering patches and tools on top of outdated core banking systems for so long that it’s become a Frankenstein’s monster of tech entanglement. A recent Federal Deposit Insurance Corp. New approaches are about simplicity.

but it has now moved within a few steps of obtaining what has eluded fintech firms of late: a green light from banking regulators. It was Varo's second try with the Federal Deposit Insurance Corp.,

Fintech's patience paying off as it nears final hurdles, setting stage for major new digitalbanking competitor. The post FDIC Greenlights Mobile-First Fintech Varo Money for Deposit Insurance appeared first on The Financial Brand.

Fintech's patience paying off as it nears final hurdles, setting stage for major new digitalbanking competitor. The post FDIC Greenlights Mobile-First Fintech Varo Money for Deposit Insurance appeared first on The Financial Brand.

Since banks with less than $10 billion in assets continue to struggle in deposit gathering, scale and overall earnings, we wonder how many will not be here in five years? The FDIC Approved This Ad How many times did we hear a speaker admonish the audience to “be sure and sign up for the FDIC notification list.” Five Hundred? (Oh

Or do you want to interact with state-of-the-art digital tools that might prevent all that mess in the first place? With the rise of digitalbanks (also known as neobanks, challenger banks, or fintechs), you now have more options. Or should you go hybrid with accounts of both types?

Weve been obsessed with new fintech products since before the term was invented. This constantly updated article tracks the biggest and most important new products released worldwide by financial technology companies, along with banks, credit unions, investment advisors, insurance companies, credit card issuers and payment providers.

Leading Digital Small Business Banks (United States) ranked by our FAB score (Fintech Attention Barometer**) Rank Company FAB** Reviewed Founded HQ Funding ($M ) Visits (Nov24) 1 Mercury 364 6 Jan 25 2017 SF $152 1,700,000 Ad* Relay 186 6 Jan 25 2018 Toronto $52 820,000 Ad* U.S. including $4.8M including $4.1M including $4.8M

Are we about to see a rush of fintech startups serving the interest-sensitive small business market? Case in point: Just days after the Feds took over SVB, Mercury was in market with its Mercury Vault, offering $5 million in FDIC insurance by distributing balances across 20 insured banks. 95,000 6 Meow * 11 4.3%

Within days of the fall of Silicon Valley Bank, challenger small-business banking provider Mercury , was in market with a timely solution to deposit insurance stress. The post Reacting Quickly to SVB Fallout, Mercury Launches Vault, with $5M FDIC Deposit Insurance first appeared on Fintech Labs SMB Center.

Are we about to see a rush of fintech startups serving the interest-sensitive small business market? But what we will surely see is challenger banks dusting off their sweep features and emphasizing them in their marketing and branding. Maybe, maybe not. 2021 SF $14 12,000 Source: FintechLabs, Crunchbase, SimilarWeb, 26 June 2023 1.

Are we about to see a rush of fintech startups serving the interest-sensitive small business market? But what we will surely see is challenger banks dusting off their sweep features and emphasizing them in their marketing and branding. 3,520 reviews, up 260 since Oct) Not FDIC insured 1. Maybe, maybe not. million (Jan.

Consumers have been banking online for 28 years. And from the very beginning, there have been pure-play digitalbanking startups. The first, online bank Security First Network Bank (SFNB) launched in 1995, just a year after Amazon.com. But unlike ecommerce, digital-only banking was slow to catch on.

MaxMyInterest members gain access to increased FDIC insurance and competitive yields on cash balances courtesy of new partnership with UFB Direct. Bahrain-based Bank ABC goes live with omni-channel digitalbanking service using Backbase’s platform. Around the web.

I’ve been expecting digitalbanking disrupters in the SMB space since the beginning of the online banking era (late-1990s). Security features (account freeze, real-time transaction notifications, FDIC insured). Learn More at Lili all-in-one mobile banking service. But now we have some impressive entrants.

I’ve been expecting digitalbanking disrupters in the SMB space since the beginning of the online banking era (late-1990s). Security features (account freeze, real-time transaction notifications, FDIC insured). Related: Watch 12 Fintech Startups Pitch at Startupbootcamp Amsterdam Demo Day (May 2021 update)).

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content