This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

San Francisco-based Empower Finance, a mobile banking app aimed at helping millennials save wealth, has raised $20 million in a Series A funding round led by Defy Ventures and Icon Ventures, according to a report. The digitalbanking field is fraught with competition. billion after recently closing a financing round.

More than half of all consumers say that having a physical branch is important for a bank to be considered their primary bank. That finding is also relatively consistent across income and demographic profiles, even for bridge millennials (the largely affluent 30- to 40-year-old crowd) and Gen Z respondents.

There are interesting characteristics both in the new entrants and in the more established digitalbanks. Some of the most important elements mentioned by analysts and professionals can be divided into four models: Digitalbank brands: Many established, full-service banks find it difficult to appeal to millennials.

Banks continue their digital transformation journey to create new business models to satisfy today’s demanding customers. How do banks prepare for this new reality? For Bradesco, a large Brazilian bank, NEXT is the answer. Next is a digitalbank, completely disassociated from the Bradesco brand.

The new surge in demand is putting financial institutions’ (FIs’) online and mobile offerings to the test and allowing FIs to show off their digital investments and know-how to assure customers that they are in good hands. The Path to DigitalBanking’s Popularity. Digitalbanking has had a long evolution in the U.S.,

As banking becomes more digital, more financial institutions are turning to technological solutions to bring more customers on board. Several banks are rolling out banking solutions that are specifically focused on winning over millennial customers as they come of age and join the marketplace as adults.

Exhibit A: EQ Bank , at the beginning of 2016, took its place as Canada’s first digital-born bank, and has now reached $2 billion in deposits. The concept is a bit different than might be seen with other digitalbanking models. Such a meteoric pace indicates a key question for banks considering the digital route.

All banks are aware of the importance of catering to the needs of the millennial generation. This tech-savvy cohort is set to dictate the direction the banking industry will take over the coming years and decades. It requires banks to develop a strong understanding of what motivates and matters to their customers.

How to meet those preferences profitably has become the focus for both commerce and financial services. And [that] opens the question around: ‘How long does it take for your relatively young customer base to catch up?’”.

That number climbs to 38 percent among baby boomers, 74 percent for Generation Xers and 85 percent for millennials and Generation Z consumers. Kikkeri said this is the highest penetration that mobile banking has ever seen among consumers. But an opportunity is only as good as the bank’s ability to pursue it.

Citizens Bank's largely millennial student loan applicants were not responding to email and phone communications. So it created a messaging service that mimics the social media they know and love.

Give a deep and welcoming hello to the newest form of window shopping — a consumer behavior that will help to shape retail in 2019 and beyond, and a trend that stands as an increasing part of shopping, one that promises to impact brick-and-mortar merchants as they decide how to innovate. DigitalBanking.

Marketers must understand mobile banking consumers’ lucrative potential: More than 90% of banking households in the U.S. use digital channels to access their banks. This is a huge percentage that marketers need to pay attention to when thinking about how to attract and retain consumers. What have you been reading?

Debit has been riding a wave of popularity for years as credit-averse millennials and their cohorts became big spenders, but didn’t want to end up like their overextended parents did in 2008. It’s a powerful statement on payments preference. People crave familiarity in tough times, and what’s more familiar than one’s own loot?

The December edition of the DigitalBanking Tracker™ details how financial institutions are working to help their consumers stay in good fiscal shape next year. Meanwhile, FinGo and eWise are also offering a new app to help millennial customers manage multiple bank accounts from a single screen.

percent of consumers noted they would switch financial institutions (FIs) for a better financial app, a number that jumps up to 41 percent among bridge millennials. Their questions aren’t so much about why they should be doing this, and much more about how to get started. Meanwhile, 28.5

As of this week, Bank of America formally announced that a little over one year in, its AI-powered voice assistant has logged 7 million users and 50 million client requests, and the firm is avidly looking at what’s next and how to keep the growth alive. Several months later, by October 2018, Erica had surpassed 3.5

The financial world has become more and more entrenched in digital channels, much to customers’ delight — 59 percent of FI consumers want to open banking accounts online rather than do so at a branch. That number is higher among millennial and Generation X respondents, at 77 percent and 63 percent, respectively.

A new survey from banking data firm RateWatch is bad news for banks looking to entice SME customers with new mobile offerings. Small businesses aren’t impressed by mobile banking, the report , released Thursday (Mar. More than two-thirds said they don’t have a positive perception of mobile banking services currently offered.

Following the highly successful The 11 Commandments of DigitalBanking eBook , we are kicking off a series of 5 deeper dive blog posts that group the 11 commandments below into common themes. Digital lift-and-shift is not a strategy! Banks must find ways to be personable in these impersonal channels. Respect the data.

How are CUs utilizing videoconferencing capabilities on interactive teller machines (ITMs) to maintain their branch operations during the pandemic, and how is biometric technology helping them offer more secure, quicker and touchless ATM services? How To Keep Fraudsters From Scamming Banks Across Every Nook And Channel .

Using credit cards (aka spending the bank’s money instead of your own) seemed so cool — until it suddenly wasn’t nearly as cool anymore. Then, just when everyone was really making money again, along comes COVID-19, wiping out the economy yet again, and within recent living memory no less. Easier said than done, but everyone’s trying like mad.

By the numbers, digitalbanking is — and is not — extremely popular with consumers of all stripes. According to the latest edition of the PYMNTS DigitalBanking Tracker, when it comes to some tasks, consumers are clearly comfortable with leaving the physical world behind and making the digital conversion.

In addition, with the emerging pull toward contactless cards, it is possible that consumers may decide there isn’t enough additional convenience or benefit to the phone as a physical payment form factor — and that the real focus of mobile digital transactions will be in app-based payments.

Our live cloud-based system running our current production digitalbanking system connected into our Fiserv payments system and developed an Alexa skill that connected the Echo into the system to address the most common and valuable and engaging user stories,” explained Scott Hess, VP Innovations Team at Fiserv. “We

PYMNTS recently caught up with Matthew Lehman, KeyBank’s SVP, Head of Online and Mobile, to discuss the evolution of digitalbanking and how a full-service bank is embracing digital and evolving along with its customers. Digital adoption – no longer solely a millennial-focused play.

DIGITALBANKING TRACKER. The DigitalBanking Tracker looks at how old ways of banking are evolving with the advent of faster technology that allows customers to get real-time updates on their accounts, share money with ease among contacts and even open accounts with a selfie.

A digital-loving millennial, John, searches our website to find the type of account he wants and chooses to open it online,” Vas Nunes said. “As As we map out John’s process, we go step by step to examine what he’s trying to accomplish, how easy it is and how he’s feeling.”.

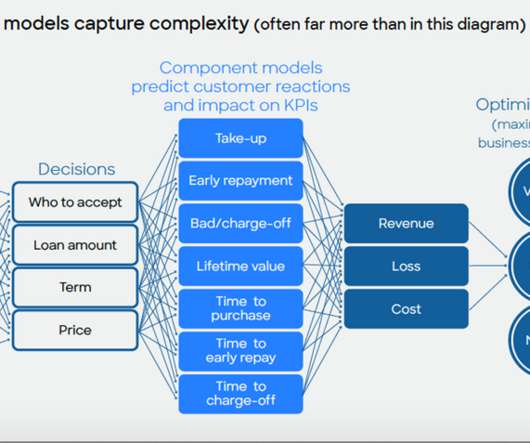

Home Blog FICO Top 5 Customer Development Posts of 2022: DigitalBanking and Pricing Opti The most popular posts in our Customer Development category dealt with digitalbanking, optimizing credit line increases, loan pricing and machine learning for credit risk models. What can financial institutions learn from TikTok?

On top of all this new technology is a core banking system that Together is preparing to deploy in the coming months that will fuel even more advanced innovations. Technology like this is especially important for attracting new members, particularly younger generations like millennials and Generation Z.

In an interview with PYMNTs, Steve Taklalsingh, Amaiz managing director & CFO, said that entrepreneurs are increasingly interested in a mobile-first option for banking as millennials and Gen Zers have grown up with the internet as a major part of their lives. ” The Mobile Banking Advantage.

Millennials are taking a mobile-first approach to banking, driving that transformation. However, older populations — and even millennials — still need the services provided by bank branches. Since smartphones haven’t learned how to print paper money, people still must turn to ATMs for that.

Top 5 Surprises from FICO’s Fraud and DigitalBanking Survey. Financial Institutions, such as banks, have expended great effort to improve digital security, yet bad actors are multiplying and attacks have increased in scope and frequency. FICO Admin. Tue, 07/02/2019 - 02:45. by Sarah Rutherford. expand_less Back To Top.

.” National providers—banks, fintechs (e.g., Paypal, Square) and even merchants—are chipping into (geographically based) community institutions’ payments, lending and banking businesses. 2) Generational changes When baby boomers graduated college, their question was, “Which bank should I open an account with?”

Research and everyday observation show how consumers are increasingly using mobile technologies. But how far are they willing to go to do their banking on small mobile devices? As Epperson says, “Community banks do have a need to appeal to that younger demographic who are managing their lives on their mobile phones.”.

And yes, for now you can still reach profit objectives and meet C/I ratio targets—while investing in more mobile and internet banking capabilities on the side. To ensure success in 2025, however, the focus should be on customers who use newer models in digital channels: Generation Y, Z, and Alpha, too—the children of millennials.

When lifetime value (LTV) is taken into account, digitally acquired customers can prove to be high-value relationships. The post How to Boost Customer Lifetime Value in Banking appeared first on The Financial Brand - Banking Trends, Analysis & Insights.

And really successful businesses these days are figuring out how to give consumers better bundles — not unbundles. The anecdote to the millennial’s so-called hatred of traditional banks hasn’t really taken off as investors envisioned. Even the largest and oldest digitalbanks have only converted a few million customers.

What these startups share is the goal of creating customer-centric banking products that target underserved individuals and businesses. DOWNLOAD THE 61-PAGE consumer banking REPORT. See which startups are helping JPMorgan, Bank of America, and Citi build the digitalbanking platforms of the future. Millennials.

In their efforts to empower branch employees to evolve and support the client’s desire to bank virtually, branch managers need to make sure customer-facing employees are prepared to answer these five basic questions: How do the institution’s Internet banking and mobile products work?

With the reality having set in across the banking industry about four or five years ago that “digital was where every bank needed to be,” says Steggall, today every bank (within reason) has some form of digital presence. – How can it be used to deliver more value to the end user?

Power 2018 survey revelation was that 71% of millennials use a branch an average of 11 times a year. So, there are a couple of ways to interpret these numbers: Interpretation #1: Banks should encourage customers to use digital and branch channels because the use of multiple channels is the thing that makes them happiest.

Statista research states that Millennials were the largest generation group in the U.S. Born between 1981 and 1996, Millennials recently surpassed Baby Boomers as the biggest group, and they will continue to be a major part of the population for many years. in 2019, with an estimated population of 72.1 Time for action / Call to action.

By their very nature, ITMs can help banks and credit unions attract younger customers. Millennials and Gen X appreciate the technology, seeing ITMs as a bridge between walking through the door or settling for a cash-only machine. THE CHALLENGES. Like any business undertaking, there are obstacles to consider. Staff accommodation.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content