This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

There are interesting characteristics both in the new entrants and in the more established digitalbanks. Some of the most important elements mentioned by analysts and professionals can be divided into four models: Digitalbank brands: Many established, full-service banks find it difficult to appeal to millennials.

is a rally cry that would perk the ears of many millennials, but how about “ Mastercard , assemble?”. Assemble for millennials is a toolkit that issuers, corporations and IBCUs can use to enable digital financial solutions, in this case targeting millennials, using a single-access digital prepaid product.

And the findings will certainly give banks pause for thought as they plan out future strategies for their physical branch networks. The answer, as Figure 5 shows, is a blend of physical and digital channels—a proposition they find much more attractive than a pure digitalbank with no branches.

In late June, the Monetary Authority of Singapore (MAS) sent a ripple through the global financial services ecosystem with the announcement of its intention to issue five digitalbank licenses to eligible applicants. Only two of the licenses will full digitalbanking licenses, while the other three will be wholesale banking licenses.

When you talk to the co-founder and CEO of a mobile-first digitalbank account offering, you are likely to hear that millennials, to put it lightly, are not fond of big banks. And that’s where digitalbanking options like Chime (a mobile-first digitalbank account, for those of you playing at home) enter the picture.

These banks must also make sure they are providing the tools that primarily digital customers need to complete their personal banking needs. Banks today are familiar with the challenges of supporting digital platforms as an increasing number of customers turn to online-only solutions.

That’s according to financial services vet and Varo Money CEO and Cofounder Colin Walsh, who told Karen Webster recently that the future of banking, for millennials in particular, lies not in branches but in bots who become money coaches. With AI … we can help them manage spending and build savings.”.

We have a deep dive into Colorado’s digital driver’s license effort and news on Alphabet’s new CEO, as well as data on millennial Black Friday spending. UK DigitalBank Monzo Taps Visa Exec as US CEO. Monzo , London’s digital unicorn, has appointed TS Anil to head U.S. Top News . operations. Curing the $2.4T

Exhibit A: EQ Bank , at the beginning of 2016, took its place as Canada’s first digital-born bank, and has now reached $2 billion in deposits. The concept is a bit different than might be seen with other digitalbanking models. Such a meteoric pace indicates a key question for banks considering the digital route.

All banks are aware of the importance of catering to the needs of the millennial generation. This tech-savvy cohort is set to dictate the direction the banking industry will take over the coming years and decades. It requires banks to develop a strong understanding of what motivates and matters to their customers.

But, while closing physical bank branches might appear to be a wise cost-saving measure, the move comes with risks that could hurt banks’ relations with new millennial customers. Armistead also spoke to the lesson the bank is learning from smartphone apps to better serve its customers online and in brick-and-mortar locations.

Today, millennials are the largest generation in the United States – and their levels of entrepreneurship are unprecedented. Millennials are starting more businesses than previous generations, and they’re starting them at a younger age than their predecessors. This year alone, the Internet of Things will connect 8.4

Community banks and credit unions are feeling the pressure to boost their digital card services or risk losing customers to megabanks and digital challengers, Ondot Systems ’ Chief Strategy Officer Todd Lesher told PYMNTS in a recent discussion. It’s a story told by the data itself, Lesher said. Square announced $1.3

Banks across the world are continuing to invest heavily in robo-advisery services, seeing them as a way to deliver personally tailored financial information and guidance at high scale and relatively low marginal cost. Figure 4: What do you value most in speaking to a human representative of a bank?

To further cultivate an innovative mindset at your institution, your bank or credit union may look to add new talent – younger talent, in particular. I’ve found that attracting younger, millennial talent is almost like attracting clients,” said McBay. Technology, like banking, isn’t “one-size-fits-all.”

consumers don’t exactly love the paper check — roughly 38 percent report that they’ve stopped using them entirely, and that shoots up to almost 50 percent when talking about millennials. It’s one thing to have a limited electronic option available — that’s quite different than having a strong digitalstrategy.”.

Competition for customers — especially millennials — from larger banks and FIs has long required credit unions to keep pace with their more innovative counterparts. This often means providing digital solutions and convenient banking options despite smaller technology and innovation budgets, however.

Though banks want to bring customers into the digital fold (it saves time and money, and, after all, 58 percent of consumers prefer digitalbanking to other methods), there will always be a need to serve them across physical locations, too. The goal for financial services, then, is a unified service model.

According to a recent study , all four of the leading banks are among the ten least-loved brands by Gen Y, and one in three millennials revealed they’re open to switching financial institutions in the next 90 days. Millennials don’t like traditional banks and don’t see any stark differences between them.

The financial world has become more and more entrenched in digital channels, much to customers’ delight — 59 percent of FI consumers want to open banking accounts online rather than do so at a branch. That number is higher among millennial and Generation X respondents, at 77 percent and 63 percent, respectively.

Banks across the world are continuing to invest heavily in robo-advisery services, seeing them as a way to deliver personally tailored financial information and guidance at high scale and relatively low marginal cost. Figure 4: What do you value most in speaking to a human representative of a bank?

Wealthfront founder, Andy Rachleff, reveals strategies that will continue to evolve to enable them to serve the needs of Millennials with investable assets. The post Wealthfront: A Digital Solution In The Battle For Millennial Deposits appeared first on The Financial Brand.

Consumers demand easy, digitalbanking, but this pressure for banks to deliver is also coming from corporate clients. Take mobile banking, which has propelled the introduction of mobile-only banks to meet demand for better services on smaller screens. According to Glover, that means banks in the U.S.

While the pandemic, as well as the rapid response, were not scenarios many were prepared for, it has provided a glimpse into what we can expect from our banking relationships moving forward. COVID-19: A springboard to digitalbanking. So, what does “working harder” mean, exactly?

Fintech is often associated with digital tools targeted at tech-savvy millennials. While many Boomers and senior citizens may not be aware of the wide variety of fintech services available to them, such as digitalbanking, a number of tools exist that aim to raise awareness. . get the REPORT on next generation investors.

Using credit cards (aka spending the bank’s money instead of your own) seemed so cool — until it suddenly wasn’t nearly as cool anymore. This has pushed credit card sales 20 percent lower than they were at the same time last year, Jeff Chernivec , senior vice president of strategy at payment solution provider Elan, told PYMNTS.

Even if they are a shrinking part of a bank’s base, these consumers remain too numerous to be ignored. Assuming that everyone will naturally make the transition to digitalbanking at their own pace will be a mistake, and may see banks lose customers as people turn to financial institutions who they feel can better cater to their needs.

Digitalbanks are no longer in the ‘money’ business but rather, in the ‘value’ business. Unlike in the past, when more than two products from one bank made a customer loyal, customer behavior is fleeting and their expectations for digitalbanking is increasing every day, because technology is giving them numerous choices and control.

Banking’s Hard Fork. The “hard fork” is an apt analogy for what the banking industry is facing. Banking’s hard fork will require financial institutions to create new strategies. The Holy Trinity of Strategy. This is an oversimplification, but a bank’sstrategy can be boiled down to: Who does it sell/deliver to?

Skyrocketing adoption of fintech is not only changing the way consumers bank, it’s changing how they live, think, and interact with money. The post Millennials Now Trust Fintechs as Much as Banks appeared first on The Financial Brand - Banking Trends, Analysis & Insights.

With tech evolution shaping customer expectations, regulatory changes creating new compliance demands and industry competition increasing all the time, banks need to get their strategy planning and execution right in order to succeed. Digital demands. Image: mdgomes via iStock.

imagin from CaixaBank is a lifestyle platform that supports a community of Millennial customers where engagement extends beyond banking services. The post CaixaBank Introduces Lifestyle Platform Targeted To Millennials appeared first on The Financial Brand.

PYMNTS has found that 55 percent of millennials say they would switch to an FI that uses geodata to enhance the security of users’ accounts. That number is even higher for those individuals who earn higher wages – and taken together, higher earners and younger demographics are the sweet spot of banks’ customer bases. The Disconnect.

A digital-loving millennial, John, searches our website to find the type of account he wants and chooses to open it online,” Vas Nunes said. “As From a strategy standpoint, this lets us understand their needs and preferences,” Vas Nunes added. A Data-Driven Approach To Improving Members’ Experiences.

Clydesdale Bank, Yorkshire Bank and digitalbanking service B began supporting Apple Pay for U.K. While Snapchat is popular among Millennials, Facebook is steadfastly a Baby-Boomer favorite , so it looks like Apple is maximizing target market opportunity. Similar risk strategies have seen a 50/50 success rate.

And by all accounts, this digital migration is driven by consumer preference — according to the same study, 91 percent of mobile banking users prefer accessing their app over going to a physical branch, and 68 percent of mobile bankingmillennials believe their smartphones will eventually replace their physical wallet.

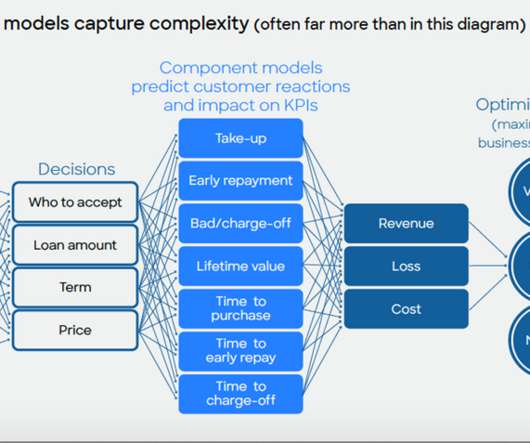

Home Blog FICO Top 5 Customer Development Posts of 2022: DigitalBanking and Pricing Opti The most popular posts in our Customer Development category dealt with digitalbanking, optimizing credit line increases, loan pricing and machine learning for credit risk models. What can financial institutions learn from TikTok?

How do traditional banks approach the challenge of adapting to the ever-evolving digital landscape and serving their customer needs? There obviously isn’t one perspective or strategy, but focusing on the customer first seems like as good a starting point as any. Digital adoption – no longer solely a millennial-focused play.

Without the resources to build out their own digital SMB lending platforms, the natural next step is to collaborate with FinTechs, a strategy that today has become commonplace for financial institutions big and small.

It’s not a “Millennial thing.” Smart banks are holding these new talents, tool vendors and fintechs accountable to specific revenue-driving projects instead of treating them as cost centers. Excerpted from Sam’s contribution to How banks can follow Amazon’s strategy of constant connection , Independent Banker, March 1, 2019.

DIGITALBANKING TRACKER. The DigitalBanking Tracker looks at how old ways of banking are evolving with the advent of faster technology that allows customers to get real-time updates on their accounts, share money with ease among contacts and even open accounts with a selfie.

Much like a bank that over-concentrates itself on commercial real estate lending, banks that rely too heavily on physical channels for consumer and business customers risk attrition, lost revenue and increased expenses. Consider these numbers from PwC’s 2017 DigitalBanking Consumer Survey : ? Aligned and Future-Ready.

The Millennial Challenge. Among the greatest opportunities for CUs lie some significant challenges, too — namely, tapping into and serving the financial needs of millennials. PSCU’s partnerships with Visa, Mastercard and Fiserv will shape strategy as the faster payments landscape continues to evolve, he said.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content