This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Turns out millennials are not the different-kind-of-banking-breed some had thought. In a survey held from the end of June into early July and conducted by SurveyMonkey , the web-based survey firm queried more than 1,000 adults above the age of 18, 290 of which were defined as 18- to 34-year-olds: millennials.

But one thing is clear: Americans would be willing to dispense with their local bank and make Amazon , Apple or Google their primary payment account provider if those 21 st -century accounts allowed them to more easily manage and spend their money. A PYMNTS survey of 3,000 U.S. The results?

For years, we’ve heard people proclaiming the demise of the bricks-and-mortar bank branch, supposedly swept away by customers’ mass-migration to online and—increasingly—mobile alternatives. But as our latest UK banking consumer survey— Beyond Banking —confirms, there’s still plenty of life in the bank branch.

Banks must now consider how to best expand remote services and emphasize these channels once consumers can safely visit branches again. This month’s Deep Dive examines how consumers are approaching digitalbanking and how FIs are leveraging online and mobile channels to prevent service gaps during the pandemic.

The latest Expectations & Experiences consumer trends survey from Fiserv , a leading global provider of financial services technology solutions, finds that consumers are paying more bills from mobile devices while slowly starting to venture into digital wallets.

Our findings also indicate FIs that offer innovative options such as interactive and contextually relevant video content stand to improve engagement and customer experiences, especially among younger generations like bridge millennials and millennials.

The latest Entersekt Consumer-Centric Authentication Playbook , the third in the series, has the subtheme “The Path to Banking App Adoption.” Digital and Mobile App Banking Drivers. The report dives into what keeps people using digital and mobile banking apps in the first place. Our survey shows that 92.4

More than half of all consumers say that having a physical branch is important for a bank to be considered their primary bank. That finding is also relatively consistent across income and demographic profiles, even for bridge millennials (the largely affluent 30- to 40-year-old crowd) and Gen Z respondents.

As banking becomes more digital, more financial institutions are turning to technological solutions to bring more customers on board. Several banks are rolling out banking solutions that are specifically focused on winning over millennial customers as they come of age and join the marketplace as adults. In the U.K.,

That simply won’t fly in the digital-first decade. Researchers found that FIs offering “innovative options such as interactive and contextually relevant video content stand to improve engagement and customer experience, especially among younger generations like bridge millennials and millennials.”.

But, while closing physical bank branches might appear to be a wise cost-saving measure, the move comes with risks that could hurt banks’ relations with new millennial customers. Results also noted this generation is less likely to open a bank account if physical bank locations are not available in their communities.

How can conventional banks stay relevant and stand out in this shifting digital landscape? This series, based on a survey of 3,000 cardholding U.S. consumers, seeks to better understand how spending and banking preferences are changing in the digital age. percent of national banks, versus 77.5

Today, millennials are the largest generation in the United States – and their levels of entrepreneurship are unprecedented. Millennials are starting more businesses than previous generations, and they’re starting them at a younger age than their predecessors. The result? More data security. More productive employees.

New digitalbanking solutions are creating new options for these citizens to make a difference in the world through their consumer purchases. Nearly a third of consumers today make purchases from brands that reflect their social and environmental values, according to a recent survey. The Right Tool for Millennial Shoppers?

One way that banks or ambitious social media platforms will win this combat for customers is through the use of mobile credit and debit cards, with a highly configurable nature and full range of card and spend management controls to please the most vacillating of customers. And in surveys at least, they don’t exhibit much loyalty to FIs.

In my first blog of this series on our latest UK banking consumer survey— Beyond Digital —I explained why there’s still plenty of life in the bank branch, since even younger customers still value human interaction. Figure 4: What do you value most in speaking to a human representative of a bank?

Pepper, the mobile banking app by Israeli Bank Leumi, is aiming to lure millennials to the service by teaming up with Playbuzz, the digital authoring platform. Another survey showed close to three-quarters of survey respondents have savings or investments and try to set aside 20 percent of their monthly earnings.

It’s one of the themes explored in the February 2020 Digital-First Banking Tracker® , done in collaboration with NCR Corporation. We’ve all heard that millennials, for example, think of bank branches as a vestiges of another century with little relevance to their financial lives. Is that what people really want?

“I’ve found that attracting younger, millennial talent is almost like attracting clients,” said McBay. While young professionals value dynamic, creative work environments, innovation, and professional development, banks rank poorly in these key areas to this demographic, according to Deloitte’s Talent in Bankingsurvey.

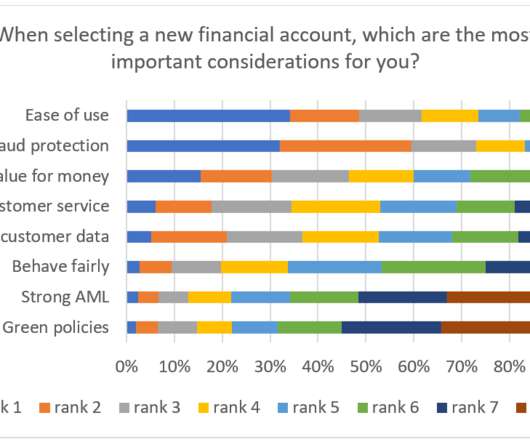

Top 5 Surprises from FICO’s Fraud and DigitalBankingSurvey. Our survey found that good fraud protection is paramount for customers - even though they themselves may exaggerate income or claims. Yet along with digital adoption, FIs are also butting up against entrenched consumer thinking that creates security risks.

Right now, at least as found recently in the PYMNTS/PSCU collaboration , “Credit Union Innovation Playbook: Challenger Banks Edition,” CUs face some competitive pressures. . As the survey of more than 4,000 CU members, CU leaders and FinTech executives showed, 41.4 They acquire a lending product, and then a digitalbanking platform.

And it’s not just millennials who are thinking of jumping ship. So, when it comes to the onboarding and origination journey in this new and evolving digital age—what is important for banks to get right to appeal to the digitally native customer? However, this isn’t just a frustration for your average millennial.

This is one of the many questions we sought to answer in Location, Location, Location: How Location Data Can Help Banks Prevent Online Fraud , a PYMNTS and GeoGuard collaboration. The report surveyed 2,141 U.S. This is especially true for Generation X and millennial consumers, at 37 percent and 36 percent, respectively.

Among the fascinating findings in PYMNTS’ ongoing surveys of Main Street SMBs during the pandemic is this: A majority of small businesses that did not apply for government bailouts simply wished to avoid debt. No matter what. Not even COVID-19 could tempt them. It’s a powerful statement on payments preference. Debit’s Destiny.

A new survey from banking data firm RateWatch is bad news for banks looking to entice SME customers with new mobile offerings. Small businesses aren’t impressed by mobile banking, the report , released Thursday (Mar. 2), concluded.

That could mean plenty of savings for banks in the coming years, according to the latest PYMNTS.com DigitalBanking Tracker. The July edition of the Tracker reports that surveys from both Bank of America and Chase indicate that consumers are planning to make more digital and mobile purchases in the years ahead.

Consumers demand easy, digitalbanking, but this pressure for banks to deliver is also coming from corporate clients. Take mobile banking, which has propelled the introduction of mobile-only banks to meet demand for better services on smaller screens.

In my first blog of this series on our latest UK banking consumer survey— Beyond Digital —I explained why there’s still plenty of life in the bank branch, since even younger customers still value human interaction. Figure 4: What do you value most in speaking to a human representative of a bank?

When it comes to American consumers, many may not be ready to admit how dependent they’ve grown on devices and the impact that’s had on the rapid growth of mobile banking and payments. The data shows there is an ever-growing daily dependence on mobile devices.

On top of all this new technology is a core banking system that Together is preparing to deploy in the coming months that will fuel even more advanced innovations. Technology like this is especially important for attracting new members, particularly younger generations like millennials and Generation Z.

Fintech is often associated with digital tools targeted at tech-savvy millennials. While many Boomers and senior citizens may not be aware of the wide variety of fintech services available to them, such as digitalbanking, a number of tools exist that aim to raise awareness. . get the REPORT on next generation investors.

In online banking, 40 percent abandonment is … intolerable. As many as four in 10 consumers have at some point in their journey into online banking found the process frustrating enough to give up, as estimated by Signicat. The challenge is to take a traditional account opening process and transform it into a simple one.

Mobile banking apps are designed to make digitalbanking more convenient for customers, yet 21.7 This was just the first of many questions PYMNTS examined in the Consumer-Centric Authentication Playbook: The Path To Banking App Adoption Edition , in collaboration with Entersekt.

Now, with PSD2 implementation across Europe just a few months away, new research from Accenture points to a major opportunity for UK banks: We’ve found that more than two-thirds (69 percent) of UK consumers say they won’t share their personal financial data with third-party providers.

Competition for customers — especially millennials — from larger banks and FIs has long required credit unions to keep pace with their more innovative counterparts. This often means providing digital solutions and convenient banking options despite smaller technology and innovation budgets, however.

Finding the right balance between physical and digital channels and approaches to banking is crucial for providers wanting to guarantee the highest possible levels of satisfaction for their customers – particularly in the millennial age group. Combining the physical and the digital.

Surveyed consumers noted trying mobile payments and ultimately giving up on them after experiencing a few failures at the point of sale, and decided they preferred their always-functional cards, particularly in-store. The largest banks in the world are investing tens of millions in enhancing their digitalbanking experiences,” Pierce said.

A digital-loving millennial, John, searches our website to find the type of account he wants and chooses to open it online,” Vas Nunes said. “As When members first join, and as they complete various transactions with us or open a new product, we have the capabilities to survey them based on their experience,” Vas Nunes said. “We

But how far are they willing to go to do their banking on small mobile devices? A consensus says that the future banking customer relationships—particularly for millennial consumers—will orbit to one degree or another around mobile technology. s entry into the payments business with Apple Pay.

In the latest survey of just about 10,000 gig economy workers, only 47 percent of those gig workers have a regular full-time job. The survey, done in conjunction with Unifund , uncovers that in general, among the four categories (No Worries, On the Edge, Second Chances and Shut Outs), many Americans live paycheck to paycheck.

Ask four different industry experts how satisfied bank customers are with their delivery options and you’ll likely get four completely different answers. Power 2018 survey revelation was that 71% of millennials use a branch an average of 11 times a year. Seventy-nine percent is too much, and banks can’t afford it.

DIGITALBANKING TRACKER. The DigitalBanking Tracker looks at how old ways of banking are evolving with the advent of faster technology that allows customers to get real-time updates on their accounts, share money with ease among contacts and even open accounts with a selfie.

Bankers are obsessed with discovering the “secrets” of getting consumers to change banks, while market researchers feed that obsession with survey data that purports to reveal those secrets. Sadly, bankers are barking up the wrong tree, and most surveys do little to help those bankers understand consumers’ real behaviors and attitudes.

Bankers are obsessed with discovering the “secrets” of getting consumers to change banks, while market researchers feed that obsession with survey data that purports to reveal those secrets. Sadly, bankers are barking up the wrong tree, and most surveys do little to help those bankers understand consumers’ real behaviors and attitudes.

We organize all of the trending information in your field so you don't have to. Join 23,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content